A Dun & Bradstreet credit report, often called a D&B credit report, provides a snapshot of how a business handles its debt obligations. Its primary purpose is to provide potential creditors and business partners with insight into how a company will likely manage its payments moving forward and its overall financial health.

A D&B report typically includes data on past payment history, bankruptcies, lawsuits, liens, and other public filings. This data is then used as the basis for various credit scores designed to reflect the company’s risk indicators, such as its likelihood of going bankrupt or being delinquent on payments over a set period of time.

How a D&B credit report works

Dun & Bradstreet pulls information from a mix of public and private sources to build your business credit file. That can include public records from county and state agencies, which may show basics like your contact details and general business information tied to licenses, permits, and other filings. On top of that, lenders, creditors, and vendors can report your payment activity to credit bureaus like D&B, which helps round out the picture of how your business pays its bills.

Once D&B compiles that data, it uses it to generate the scores and ratings that appear on your credit report, giving readers a sense of your company’s overall financial stability. Because your business profile is generally available to others, creditors, partners, and vendors can review it when deciding whether to extend credit or do business with you. D&B also offers multiple report types, and what you’ll see can vary depending on which report you choose.

Types & costs of reports

| Report type | Cost |

|---|---|

| D&B Credit Insights Free | $0 |

| D&B Credit Insights Basic | $49 per month |

| D&B Credit Insights Plus | $149 per month |

| Business Information Report™ Snapshot | Starting at $139 per year |

| Business Information Report™ On Demand | Starting at $189.99 per year |

| D&B Credit Evaluator Plus | Starting at $61.99 per report |

- D&B Credit Insights Free: $0 for alerts that monitor changes in your credit profile while highlighting potential risks or opportunities. This product includes PAYDEX®, delinquency, and failure Score. Also included is a summary of basic company information and legal events.

- D&B Credit Insights Basic: $49 monthly for 24/7 monitoring and access to PAYDEX®, delinquency score, failure score, maximum credit recommendation, and D&B rating. This report includes detailed insights based on the historical trends of your business’s credit score and ratings, along with comprehensive legal events details, including lawsuits, liens, judgments, and UCC filings.

- D&B Credit Insights Plus: $149 per month for all of the features in Basic, plus dark web monitoring for up to five business email addresses and the ability to compare your business scores against up to five other companies and to provide the company with various financial statements so that they may be validated and included with your business credit report.

- Business Information Report™ Snapshot: $139.99 a year to view another US or Canadian company’s detailed business credit report, which is available online for up to 12 months. Included is a company’s PAYDEX® score along with five other D&B scores and ratings. You’ll also be able to view company information and payment history.

- Business Information Report™ On Demand: $189.99 annually for unlimited access to view another company’s business credit file in real-time for up to 12 months. Included are D&B scores that provide insight into potential defaulted payments or the likelihood of financial strain. Alerts for changes to the company’s credit file are also available for up to 12 months.

- D&B Credit Evaluator Plus: $61.99 for a single report, although you can get a volume discount if you purchase five or more at the same time. This product allows you to view credit information for your suppliers, vendors, customers, and other business partners so that you can determine any potential risk. This can help with decisions like determining how much credit to extend, what payment terms should be, and whether there are any potential legal risks due to pending litigation.

Key features of D&B reports

When reading a D&B credit report, there are various elements to consider. Here are some key features to keep in mind:

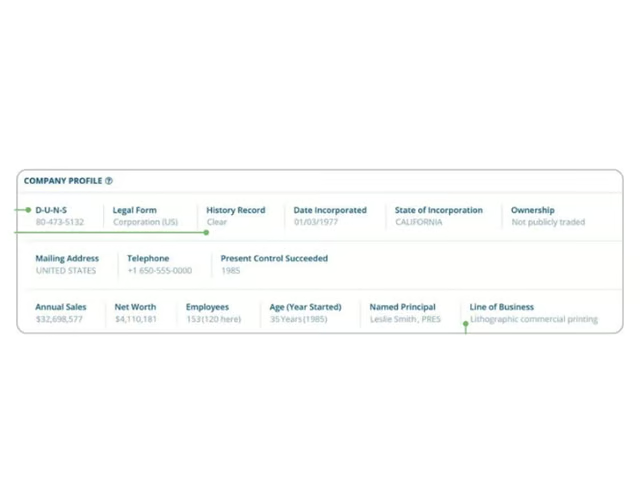

Company profile

The company profile section pulls together core details about your business, including your DUNS Number, contact information, industry classification, and legal structure. Lenders, partners, and vendors may use this section to confirm your information and evaluate your business before deciding to work with you.

Company profile section of a D&B profile. (Source: Dun & Bradstreet)

Categories of company profile section. (Source: Dun & Bradstreet)

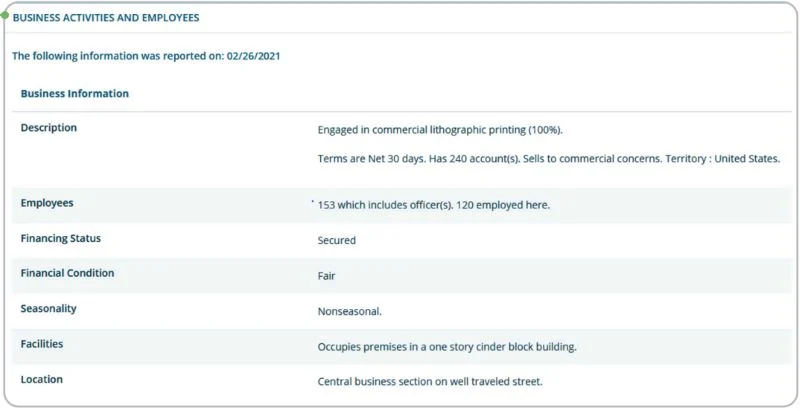

Business activities

This section is attached to the company profile and includes information regarding your business description, number of employees, financial status and condition, payment terms, seasonality, and location and facilities.

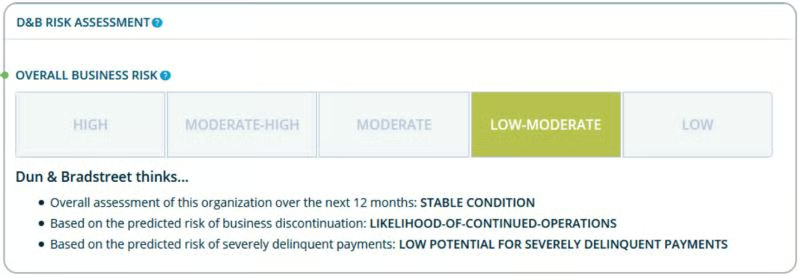

Risk assessment

D&B scores are based on several factors that help indicate a business’s potential risk level and overall creditworthiness. When it comes to broader business risk, D&B typically provides five risk scores, each designed to signal lower to higher risk, along with insight provided by D&B as to the present and future financial strength of your business.

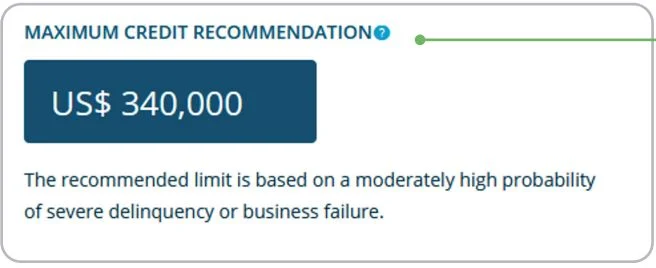

Also included is D&B’s Maximum Credit Recommendation, which is the suggested maximum amount of credit to be extended to your business.

Report scores

There are five ways in which D&B measures your score:

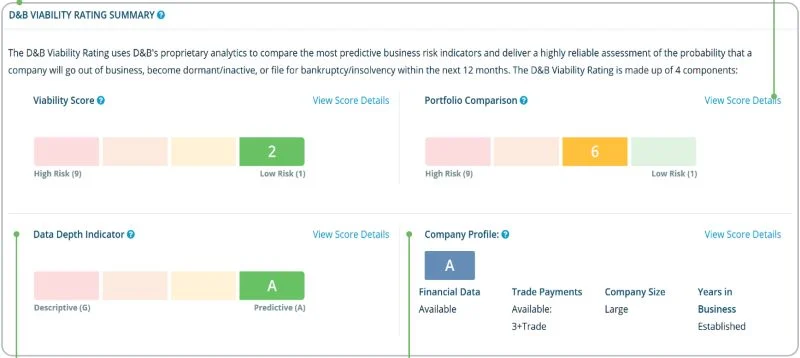

1. Viability Rating

A viability rating is based on the risk that a company will no longer be in business, file for bankruptcy, or become inactive within a 12-month period. The rating is made up of four components, which include the viability score (scores ranging from 1 to 9; 1 being the lowest risk), portfolio comparison (scores also ranging from 1 to 9; 1 being the best in comparison), data depth indicator (scores ranging from A to M), and company profile (scores ranging from A to Z).

2. D&B Delinquency Score

The D&B Delinquency score ranges from 1 to 100 and represents the probability that a company will be delinquent in making payments, generally 90 days or later.

3. D&B Failure Score

The D&B failure score ranges from 1 to 100 (1 being the highest risk) and determines the likelihood that creditors won’t receive payment if a company fails, including filing for bankruptcy or going out of business.

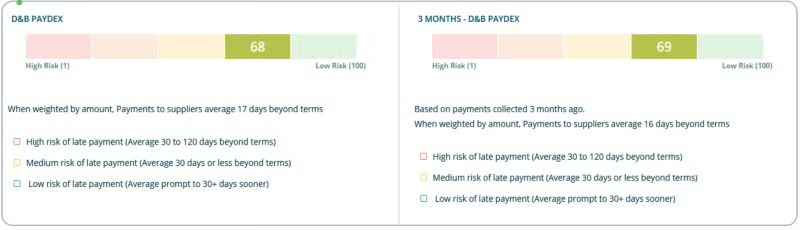

4. PAYDEX® Score

A PAYDEX® score is a dollar-weighted measure of a business’s payment performance over the past two years, based on trade experiences reported by vendors. To generate a PAYDEX® score, a business generally needs at least three reported trade experiences from at least two different vendors. The score uses a 1–100 scale (with 100 as the best) and is commonly reviewed by creditors to assess creditworthiness.

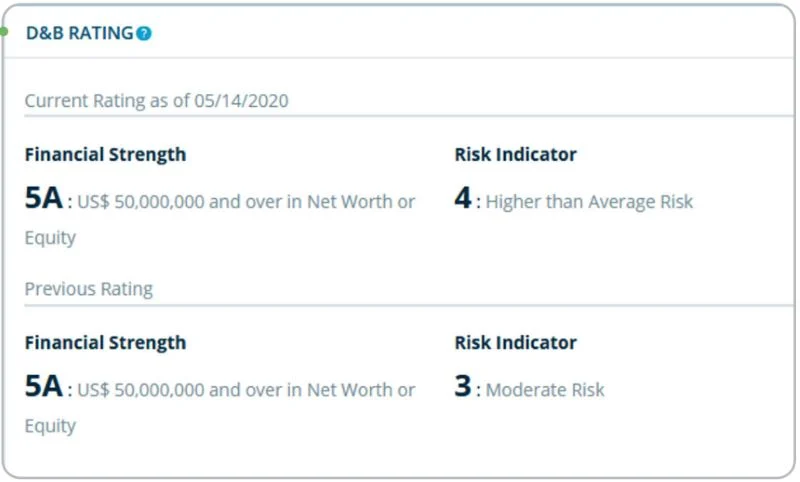

5. D&B Rating

A D&B rating reflects the average of a company’s historical financial performance, factoring in elements such as payment history, time in business, company size, and other financial data. It is presented as an alphanumeric score that signals overall financial strength and serves as an indicator of business risk.

Trade payments

The trade payments section summarizes payment history to other partners. It indicates evidence of payment behavior, such as past-due amounts and total days of past-due payments. Also noted are the types of trade accounts and the total value of each tradeline.

Detailed trade risk insight

This section provides a 13-month, time-series view of a company’s trade payment activity using a large pool of reported commercial trade experiences. It helps you see how consistently the business is paying back unsecured credit commitments and spot recent shifts in payment behavior.

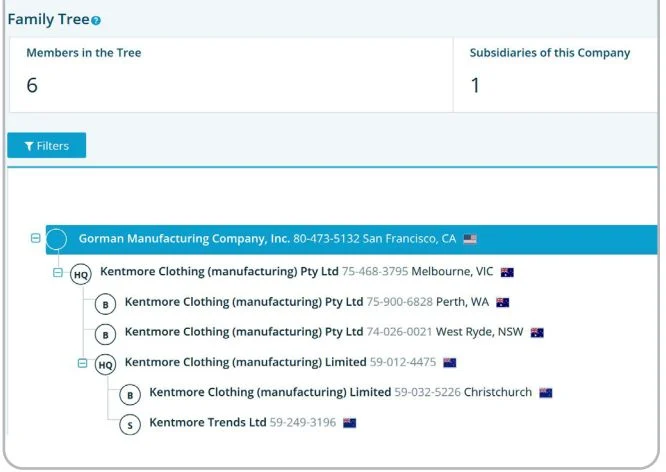

Ownership

This section provides an overview of the ownership chart, which displays relationships between different companies in the D&B database.

This can be used to assess potential risk across a family tree and to provide a global overview of the majority-owned subsidiaries and their relationships.

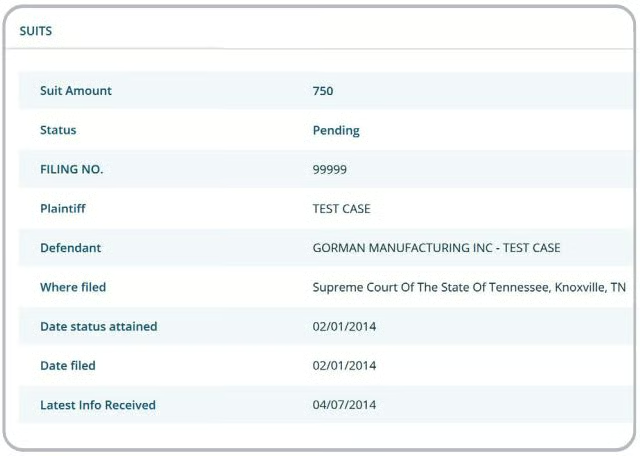

Legal Events

The legal events section reports any legal activity that could impact the financial stability of your business, such as bankruptcy filings, judgments, liens, lawsuits, and UCC filings.

Details regarding any legal events are summarized as demonstrated in the example below:

Special Events

The Special Events section presents the latest developments of a business, such as changes in ownership, operations, and earnings announcements, if applicable.

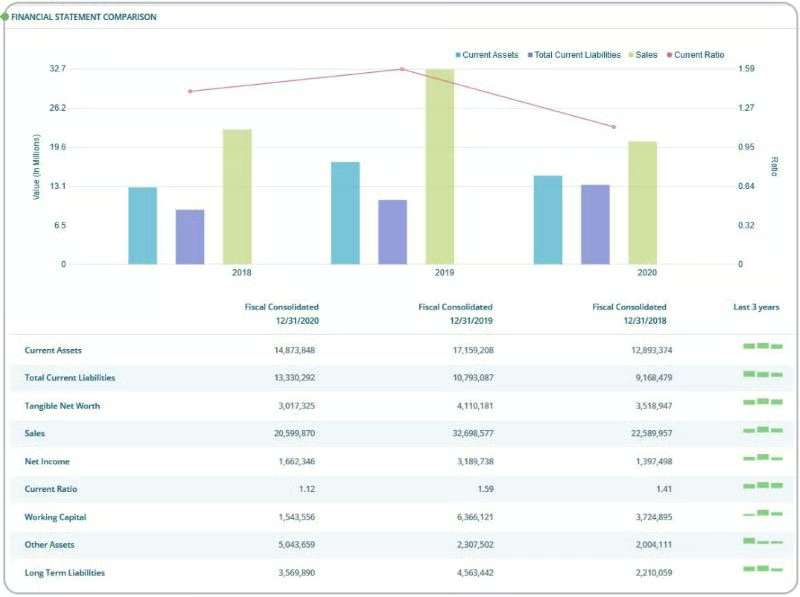

Financials

Depending on the business, a D&B credit report may include access to financial documents such as balance sheets, cash flow statements, profit and loss statements, and other available financial reports.

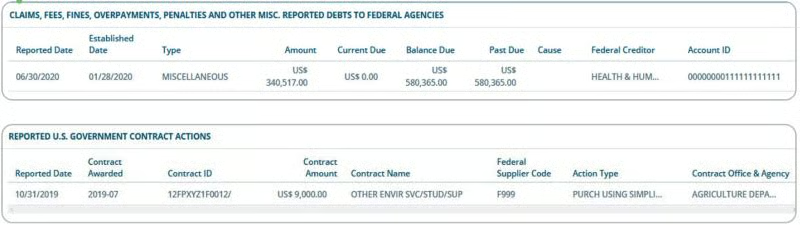

Federal Information

This section supplies information regarding dealings with the US Government (including exclusions) and highlights any activity such as contracts, debts, or assistance.

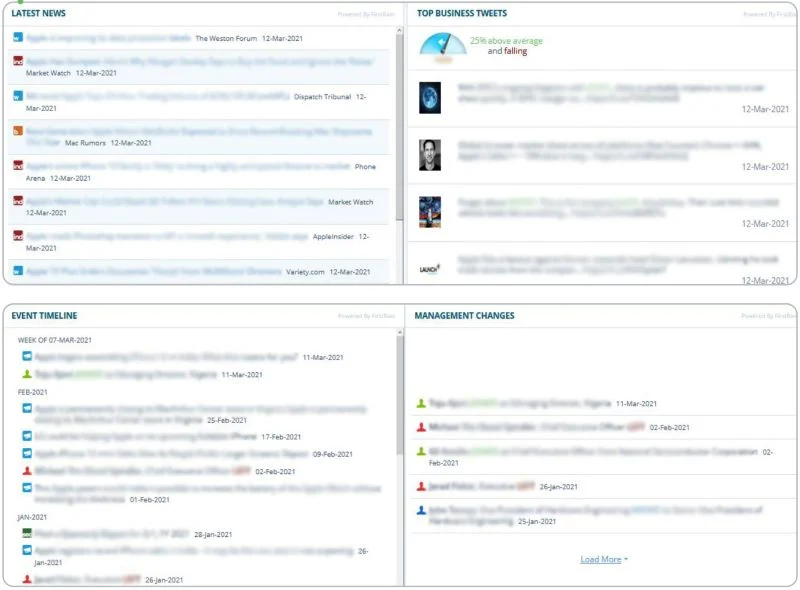

Web & Social

The Web & Social section typically highlights recent news and other online mentions of your business. It can help round out the story for anyone researching your company and provide added context around potential risk factors.

Pros & cons of the Dun & Bradstreet credit report

| PROS | CONS |

|---|---|

| Widely used and recognized by lenders, suppliers, and partners | Can be costly, especially for small businesses |

| Is required from lenders and for government contracts | Requires you to get a DUNS number, which can take up to 30 days |

| Makes it easier to track, establish, and strengthen business credit over time | Keeping your profile accurate and complete takes ongoing time and attention, and paid add-ons can increase the total cost |

Who is a D&B credit report right for?

A business credit report is not only something lenders and potential partners can review. It is also something you can use to show your creditworthiness and put yourself in a stronger position when you need funding or better terms. Essentially, that can mean negotiating more favorable loan terms, longer payment windows, or higher credit limits.

It may be for you if you are a business:

- Looking to build its credit profile: Your company can establish business credit with a D&B credit profile, even if you currently have little to none.

- Seeking financing opportunities: Lenders often utilize a D&B credit report to determine the creditworthiness of a business. Your demonstrated financial history can be a great benefactor toward approval and is generally part of small business loan requirements.

- Working with vendors often: Vendors or other partners can reference your established payment history, which provides you with leverage to negotiate better terms.

How to get a D&B report

D&B credit reports are accessible to all businesses and can be obtained from the D&B website.

- Step 1: Get a DUNS number. This can then be used to apply for or access a report. You can use D&B’s DUNS Number Lookup tool to check if you already have a DUNS number or apply for one if needed. You’ll need this number to search for a company, whether it be your own or the company whose report you’re looking to access.

- Step 2: Select your report type. If you’re looking to obtain a free report, you can get started with D&B’s Credit Insights report, which has options to upgrade your report at various price points. Descriptions of each report, along with their cost, are listed under each product type.

- Step 3: Choose your desired product and add it to the cart. You’ll then proceed to the checkout ,where you can select your payment options and complete the purchase. Once the transaction is complete, your D&B credit report will be available to view online.

Alternatives to a D&B report

While the Dun & Bradstreet credit report is one of the most trusted financial resources, there are other options available that can provide you with similar metrics and insights.

- Equifax reports include a business credit risk score, business payment index score, and business failure score. Similar to D&B, Equifax collects data on financial information, payment history, and public records.

- Experian is the largest credit bureau, and its credit reports include a score of 0 to 100, measured by its Intelliscore Plus model. This factors in collection and payment history, filings for bankruptcy, and financial information. No self-reported data is allowed in contrast to D&B credit reports.

- Transunion is another major credit bureau, offering various solutions to help business owners measure and identify risk. Risk categories covered include credit, insurance, employment, and tenant risk for rental vacancies. The company also has additional risk products to help manage your credit portfolio, acquire customers, prevent fraud, and much more.

- FICO® SBSS℠ score is measured by data from all three credit bureaus (i.e., D&B, Equifax, Experian) and has a score range of 0 to 300. It can utilize both personal and business credit data, in part with other financial information. To qualify, most SBA lenders require a minimum score of 160 to 165.

Frequently asked questions (FAQs)

What is considered a good D&B credit score?

The D&B PAYDEX® score is one of the most commonly reviewed D&B scores, and a rating of 80 or higher is generally viewed as strong. The PAYDEX® scale runs from 0 to 100, but it’s worth noting that this score is usually only one piece of the decision. Lenders often weigh it alongside other factors when approving or denying a loan.

Can I get a D&B credit report for free?

Yes, you can get the D&B Credit Insights report for free. This report can allow you to check your scores and monitor any changes that occur.

How can I correct or modify a D&B report?

If you believe there may be an error on your report, use the D-U-N-S Profile Manager form or contact Dun & Bradstreet directly. Since potential creditors and vendors may evaluate your D&B report in setting terms and conditions, it’s critical that you correct any errors as quickly as possible to avoid any adverse action.

Bottom line

A Dun & Bradstreet credit report pulls together information from your business’s history and turns it into scores that reflect your company’s creditworthiness. Creditors and potential partners use it to understand how your business has handled financial obligations in the past and how reliable it may be going forward. For you, it can be a practical resource when getting a small business loan, keeping tabs on your credit profile, and using your established credibility to negotiate stronger terms.