Consignment allows businesses to sell goods via third-party sellers without requiring the sellers to pay for the goods upfront. Because consignees are only tasked with selling consigned inventory, ownership remains with the consignor until it is sold to final customers. In exchange, the consignee will get a commission from the sales. In this article, we’ll teach you consignment inventory accounting and go over the accounting process for consignors and consignee.

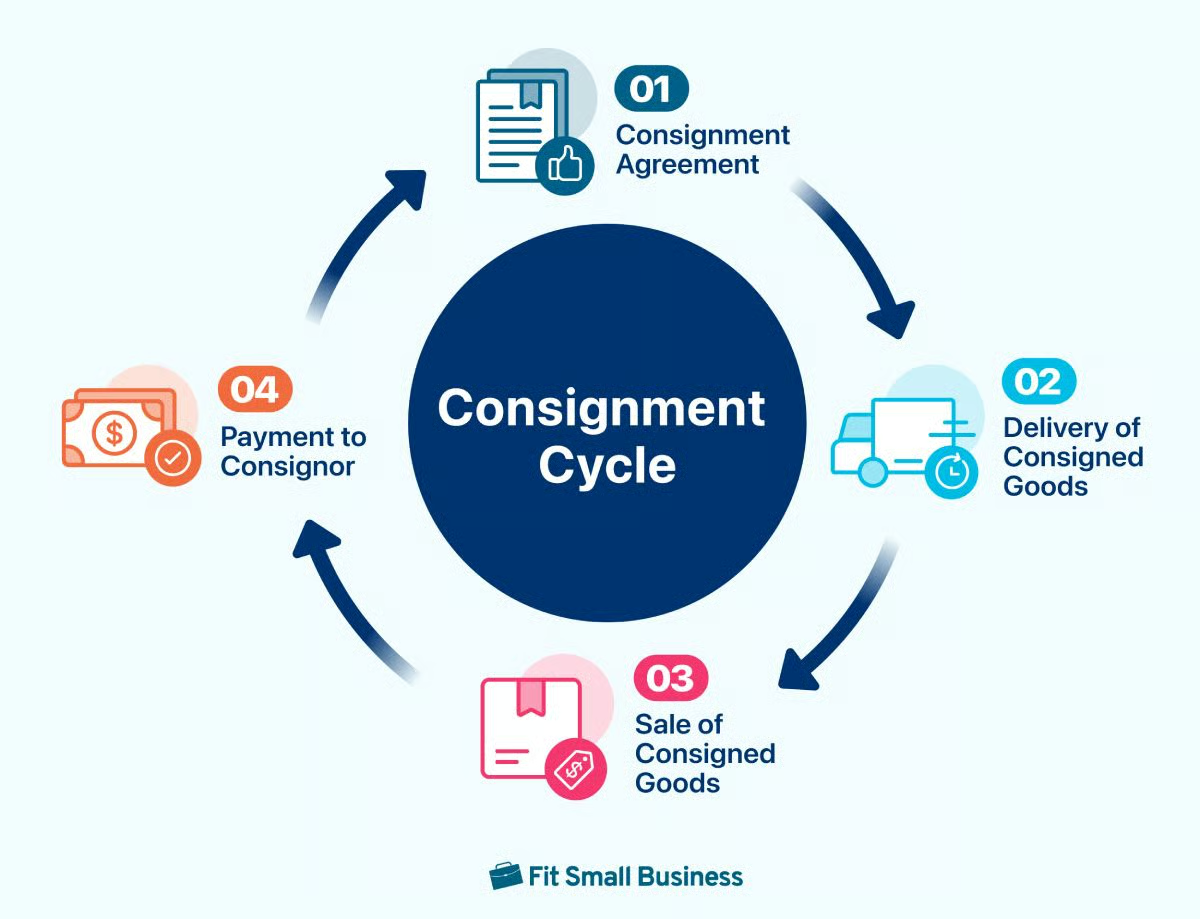

How the Consignment Cycle Works

Understanding how to account for inventory consignment requires understanding what to do at each stage of the consignment process. A consignment arrangement revolves around four steps:

Step 1: Signing of Consignment Agreement

The consignment agreement is a crucial step in the consignment cycle. We recommend that consignors put this in writing to avoid confusion and misunderstandings.

This agreement will serve as a contract between the consignor and consignee, binding each party to perform their roles and responsibilities in the transaction.

The agreement should contain at least the following information:

- Details of the contracting parties, such as name or business name, address, and contact information.

- Consignment period that mentions the commencement and termination of the contract.

- Ownership provision stipulating that the ownership of the consigned goods remains with the consignor until it is sold to final customers.

- Sales provision stipulating how and at what price should the consigned goods be sold.

- Remittance provision stipulating how and when should the consignee remit the proceeds, such as remittances that must be made on the 25th of each month through PayPal or bank transfer.

- Sales tax collection stipulating that the consignee should collect and pay sales taxes directly to the state department.

- Loss provision stipulating who shoulders the loss of consigned goods because of spoilage, breakage, theft, and fortuitous events.

- Commissions and fees provision stipulating the amount of commission the consignee can deduct from the total proceeds of consignment sales.

Step 2: Delivery of Consigned Goods

For consignors

- Ship the goods to the consignee on a timely basis to avoid stockouts

- Pay for the shipping and insurance fees related to the shipment

- Provide the necessary equipment needed to preserve perishable products, such as freezers for ice cream products

For consignees

- Inform the consignor if the goods have already arrived

- Ensure proper safekeeping of the consigned goods and have the right equipment for this purpose. In some cases, consignors provide equipment for free

- Keep proper accounting of consigned goods to prevent them from being mixed up with other goods in your inventory

- (If you paid for the shipment costs) Inform the consignor that you will deduct this from the sales proceeds

Step 3: Sale of Consigned Goods

For consignors

- Ask for a daily sales report from the consignee to update your records

- If the stock is running out, send another batch to avoid stockouts

For consignees

- Sell the consignor’s goods based on the stipulations in the consignment agreement

- Set your own price if it’s allowed in the consignment agreement. Otherwise, stick to the consignor’s suggested retail prices (SRP)

- Prepare a daily sales report for the consignor

- Inform the consignor of spoilages or breakages if there are any

- Ship the goods to final customers. If there are delivery costs, the final customers should pay for it

Step 4: Payment to Consignor

For consignors

- Compute the remittance amount that you expect to receive

- Remind the consignee to remit payments

- If there’s a mismatch between you and the consignee’s computation, find a way to resolve this issue by going over the records

For consignees

- Compute the remittance amount and deduct commission fees

- Send the payment to the consignor via the agreed payment channel

- If there are payment fees, ask the consignor if they can pay for it

Example of Consignment Inventory Accounting

As part of consignment inventory management, both parties should practice proper accounting of consigned goods. For consignors, proper accounting helps them keep track of profits. Whereas for consignees, it helps them segregate consigned goods from other inventory items.

In this section, we’ll show you the different journal entries that consignors and consignees should do to account for consignment transactions.

For illustration, let’s assume that Bakery Inc., the consignor, entered into a consignment arrangement with Walmart, the consignee, to sell its pastry products.

- On January 2, Bakery Inc. shipped $40,000 worth of pastry products and paid $2,500 in shipping.

- To stimulate sales, Walmart spent $700 in advertising costs.

- Walmart sold 75% of the consigned goods for a total sales amount of $45,000 and reported this amount to Bakery Inc.

- On January 31, Bakery Inc. collected cash due from Bakery Inc. less 10% commission and advertising costs. They also pulled out spoiled goods worth $200.

Click each tab to view the journal entries per transaction.

Consignor’s Books (Bakery Inc.)

| Debit | Credit | |

|---|---|---|

| Inventory on Consignment | 40,000 | |

| Finished Goods Inventory | 40,000 | |

| Inventory on Consignment | 2,500 | |

| Cash | 2,500 |

Shipping costs are inventoriable costs in the books of the consignor. These costs should be debited to the Inventory on Consignment account, not freight expense.

Consignee’s Books (Walmart)

| Debit | Credit | |

|---|---|---|

| No Entry |

At this point, the consignee will have no journal entry. However, they may create a memorandum entry stating, “On January 2, Bakery Inc. shipped consigned goods worth $40,000.”

Consignor’s Books (Bakery Inc.)

| Debit | Credit | |

|---|---|---|

| No Entry |

Advertising expenses paid for by the consignee to promote the consignor’s products will be deducted from consignments. For now, no entry must be made in the books of the consignor.

Consignee’s Books (Walmart)

| Debit | Credit | |

|---|---|---|

| Receivable from Bakery Inc. | 700 | |

| Cash | 700 |

Consignees may launch advertising campaigns to boost the consignor’s product sales, depending on the agreement. Bakery Inc. bears the advertising cost, which is why Walmart records a receivable.

Consignor’s Books (Bakery Inc.)

| Debit | Credit | |

|---|---|---|

| Receivable From Walmart | 45,000 | |

| Sales | 45,000 | |

| Cost of Goods Sold (COGS) | 31,875 | |

| Inventory on Consignment | 31,875 |

At this point, Walmart reported sales of $45,000—and Bakery Inc. expects to receive this amount. That’s why we recorded a receivable. Since Walmart’s report stated that 75% of consigned goods have been sold, we can also record the cost of goods sold of $31,875 computed by multiplying $42,500 by 75%.

Consignee’s Books (Walmart)

| Debit | Credit | |

|---|---|---|

| Cash | 45,000 | |

| Payable to Bakery Inc. | 45,000 |

Walmart records a payable because consignment sales are not Walmart’s revenues.

Consignor’s Books (Bakery Inc.)

| Debit | Credit | |

|---|---|---|

| Cash | 39,800 | |

| Commissions Expense | 4,500 | |

| Advertising Expense | 700 | |

| Receivable From Walmart | 45,000 | |

| COGS | 200 | |

| Inventory on Consignment | 200 |

Bakery Inc. receives $39,800 as the net proceeds of consignment sales. Walmart deducted $4,500 (45,000 × 10%) commission fees and $700 advertising fees from the sales proceeds. Bakery Inc. then records these as expenses. The $200 cost of spoiled goods pulled out from Walmart can be recorded as an additional cost of goods sold in this case.

Consignee’s Books (Walmart)

| Debit | Credit | |

|---|---|---|

| Payable to Bakery Inc. | 45,000 | |

| Commissions Revenue | 4,500 | |

| Receivable from Bakery Inc. | 700 | |

| Cash | 39,800 |

In Walmart’s books, the 10% commission is credited to Commissions Revenue. If you go back to Transaction 2, we recorded a receivable to track Walmart’s payments for advertising. We should credit Receivable From Bakery Inc. to deduct advertising costs from total proceeds. Overall, Walmart should only pay $39,800 after deducting commissions and advertising costs.

Related Resources:

- What Is Bookkeeping and What Does a Bookkeeper Do?

- Cost of Goods Sold: What It Is & How To Calculate It

Frequently Asked Questions (FAQs)’

Is proper accounting needed for both the consignor and consignee?

Yes, because both parties must keep track of consignment transactions. For the consignee, proper accounting ensures that consigned goods aren’t mixed with other goods. For the consignor, it helps them account for the cost of goods sold and revenue.

Who records inventory on consignment?

The consignor records the inventory on consignment because they still own the consigned goods until sold to final customers. The consignee does not show consigned inventory on their balance sheet.

What happens to unsold goods on consignment?

The consignee may continue to sell these goods even if new stocks have arrived. However, for perishable goods, the consignor may pull out old stock and replace it with new stock.

Bottom Line

Consignment is a good business model if you want to expand your retail business by being a consignee. For consignors, consignment is an opportunity to introduce your products to a different market. We hope this guide taught you how consignment inventory works and the different journal entries involved in the consignment process.