The prime rate can affect the interest rate you get on a loan, although lenders may use varying methods. It can fluctuate over time, so being aware of the prime rate can give you an idea of the range of interest rates you might be able to get.

As a general rule of thumb, the prime rate is typically 3% higher than the federal funds rate, which is the interest rate that banks charge other institutions to borrow money. In other words, just like individuals and business owners are charged interest when they take out a loan, banks are charged interest at the federal funds rate.

How the Prime Rate Can Affect You

The interest rate on a loan is usually determined by taking the prime rate and adding it to a margin. For example, a bank charging its best customers a 0.25% margin on a prime rate of 8.50% would result in a final interest rate of 8.75%.

If the prime rate were to rise to 9.00% six months later, the best interest rate available to new borrowers would be 9.25%, even if the borrowers are just as well qualified as those from earlier in the year.

Interest Rates & Loan Pricing

Many lenders determine the margin and rate you get based on your qualifications as a borrower. The specific criteria can vary based on the type of financing being offered, and you can check out our guide on small business loan requirements for more details.

To illustrate how the prime rate can impact the interest rate you get, below is a simple example of a lender that determines pricing based on your credit score.

| Credit Score | Example Current Prime Rate | Margin used by Bank | Bank’s Method of Determining Your Rate | Rate Issued to Borrower |

|---|---|---|---|---|

| 760 to 850 | 8.50% | 0.00% | Prime + 0.00% | 8.50% + 0.00% = 8.50% |

| 720 to 759 | 8.50% | 0.50% | Prime + 0.50% | 8.50% + 0.50% = 9.00% |

| 680 to 719 | 8.50% | 1.00% | Prime + 1.00% | 8.50% + 1.00% = 9.50% |

| 620 to 679 | 8.50% | 1.50% | Prime + 1.50% | 8.50% + 1.50% = 10.00% |

| 619 and under | 8.50% | 2.00% | Prime + 2.00% | 8.50% + 2.00% = 10.50% |

Variable Rate Loans

Many variable rate loans are tied to the prime rate. As a result, it’s important to know the circumstances in which the rate can change if you have a loan with a variable interest rate. We recommend paying attention to the following terms:

- The specific index it’s tied to (such as the prime rate)

- How much the rate may change (up or down)

- When the rate may change

- How often the rate can fluctuate

- Options for locking a portion of the balance at a fixed rate

Why the Prime Rate Might Change

The Federal Reserve determines the federal funds rate based on the overall health of the economy. When the rate is reduced, it makes it more affordable to borrow money and encourages more spending. With a higher rate, borrowing money becomes more expensive.

Scenario 1: Encourage Saving

The Federal Reserve can increase rates if it believes inflation is running too high, or otherwise wants to reduce the flow of money between individuals and businesses. Loan rates will be higher, but rates on savings accounts will also be greater. In other words, increases in the federal funds rate and prime rate make it more expensive to borrow money and give people more incentives to save.

Scenario 2: Encourage Spending

Reductions in the Federal Funds rate generally occur when the Federal Reserve wants to encourage individuals and businesses to spend more money and increase hiring levels. Rates on loans will decrease, making it cheaper to borrow money. Similarly, rates on savings accounts will also go down, encouraging people to spend or invest funds elsewhere.

How Often the Prime Rate Changes

There is no set schedule for when the prime rate changes. However, it could potentially change around eight times a year. That is the number of times the Federal Reserve typically meets to determine whether adjustments are necessary to the federal funds rate, although additional meetings can be called depending on the state of the economy.

Changes in the federal funds rate often lead to changes in the prime rate. While banks have the ability to choose which figure they use here, most use the WSJ prime rate. This rate is determined by surveying 30 of the largest banks and changes when at least 23 make a change.

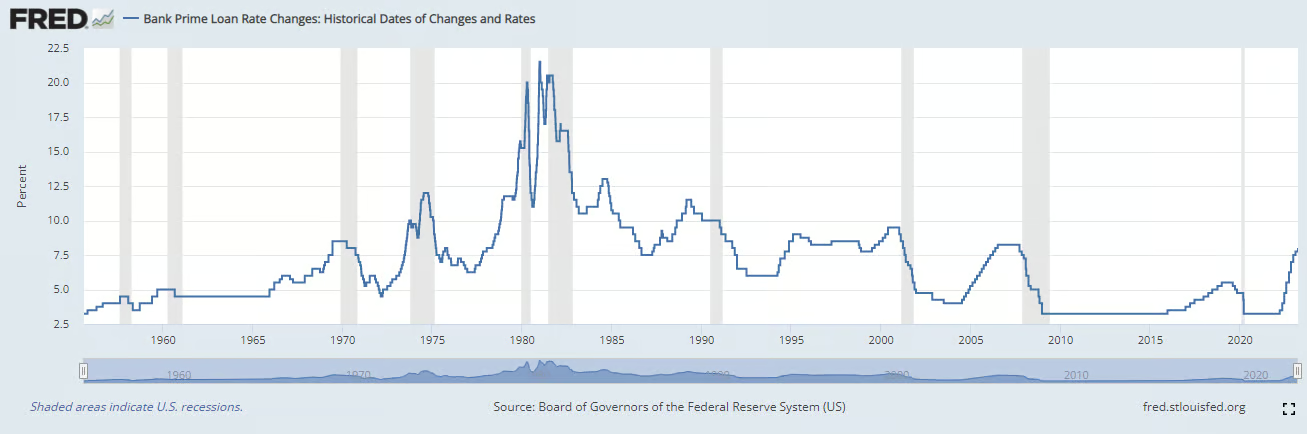

Historical Prime Rates

The prime rate will continue to change over time depending on the overall state of the economy. It reached a high of 21.5% in December 1980 and a low of 3.25% as recently as March 2020, which was largely in response to the COVID-19 pandemic.

We’ve listed the prime rate changes since March 2020, along with a historical chart dating back to the 1950s.

| Date of Change | New Prime Rate |

|---|---|

| July 27, 2023 | 8.50% |

| May 4, 2023 | 8.25% |

| March 23, 2023 | 8.00% |

| Feb. 2, 2023 | 7.75% |

| Dec. 15, 2022 | 7.50% |

| Nov. 3, 2022 | 7.00% |

| Sept. 22, 2022 | 6.25% |

| July 28, 2022 | 5.50% |

| June 16, 2022 | 4.75% |

| May 5, 2022 | 4.00% |

| March 17, 2022 | 3.50% |

| March 16, 2020 | 3.25% |

Prime Rate Alternatives

The prime rate is not the only figure that banks can use as a benchmark in determining how they set their interest rates for lending or banking accounts. Alternative figures can be used depending on a bank’s goals, policies, or location. This can be especially true for banks that have a larger international presence, as opposed to one primarily based in the United States.

Below are some examples of alternatives that banks may use:

- Secured overnight financing rate (SOFR)

- American Interbank Offered Rate (AMERIBOR)

- Bloomberg Short-Term Bank Yield Index (BSBY)

Frequently Asked Questions (FAQs)

Does a change in the prime rate mean interest rates will instantly change?

No. Lenders may not immediately adjust rates on their loan programs. This can commonly be due to its own policies that dictate a change in rates only during certain times throughout the year.

Do all lenders adjust rates based on the prime rate?

No. Alternative indexes, such as SOFR and AMERIBOR, may be used instead of the prime rate to determine what interest rates are offered for certain loan programs.

What is the difference between the federal funds rate and the prime rate?

The federal funds rate is determined by the Federal Reserve and reflects the rate that banks charge when borrowing money from one another. Meanwhile, the prime rate is typically 3% higher than the federal funds rate and is the rate that banks charge their customers.

Bottom Line

Being aware of the prime rate is important because it often impacts the interest rate you get on a wide variety of loans. It’s typically the rate offered by banks to its most creditworthy customers. However, while it may be one of the more common benchmarks banks use to determine rates, lenders can choose other options.