You can use your 401(k) in a few different ways to fund a business venture, whether you’re buying a company, contributing capital to an existing business, or starting one on your own. In most cases, you’ll access those funds through one of three paths: a Rollover for Business Startups (ROBS), a 401(k) loan, or a 401(k) withdrawal.

Each option works differently, with distinct considerations related to taxes and potential penalties, how quickly you can access funds, total costs and fees, and eligibility rules. I’ll walk through each approach so you can compare them side by side and choose the best fit for your situation.

- Rollover for Business Startups (ROBS): Good for investing retirement funds into a business without incurring taxes or penalties

- 401(k) loan: Good for short-term access to funds and business owners who can repay the loan from their current employment

- 401(k) withdrawal: Best for last-resort funding due to financial hardship and for business owners willing to accept taxes and penalties

Quick comparison of ROBS vs. 401(k) loan vs. 401(k) withdrawal

Each way of accessing your 401(k) comes with its own rules and implications, and the right option depends on what you’re trying to accomplish. To give you a quick overview of which one might be best for you, I’ve created the following comparison table.

| ROBS | 401(k) Loan | 401(k) Withdrawal | |

|---|---|---|---|

| Funding speed | 2-4 weeks | 1-3 weeks | 1-2 weeks |

| Ease of qualification | Complex; requires setup of a C Corporation entity | Easy (no credit checks required) | Proof of financial hardship may be required if under the age of 59.5 |

| Repayment requirement | None required | Yes | None required |

| Tax implications | No direct tax implications | None | Income tax & potential early withdrawal penalties |

| Impact on retirement | Risk of losing funds if the business fails | Low; reduced growth in retirement growth | High; reduction in available retirement balance |

| Cost | Highest; one-time and monthly recurring maintenance fees | Low; documentation, application, or administration fees | High if deemed an early withdrawal; subject to taxes and penalties |

| Risk of legal issues | High if not done correctly | Low | Low |

| Control over funds | Must be used for business purposes | Varies based on plan terms | Typically unrestricted |

| Impact of job loss | None | May require full repayment within 30 to 60 days | None |

Using a Rollover for Business Startups (ROBS)

How a ROBS works

A ROBS allows you to access funds from your retirement accounts without penalty or tax implications. That said, there are various tax rules and regulations that business owners must adhere to.

With a ROBS, you start by moving money from your personal retirement account into your company’s retirement plan. That plan then uses the funds to buy stock in the business, which is how the business receives the cash. It’s similar to how a company raises money when an individual buys shares in a publicly traded company, since the purchase provides capital that the business can use.

Pros & cons

| PROS | CONS |

|---|---|

| Provides tax- and penalty-free access to retirement funds | Complex transaction that can be difficult to understand |

| Easier qualification requirements than traditional business loans | Typically takes several weeks before funds can be accessed |

| No monthly payments required as it is not a loan | Ongoing maintenance is required to remain compliant |

| Funds can be used for any business purpose | Most ROBS providers charge one-time and recurring fees to maintain the plan |

Who should consider a ROBS

If you’re considering a ROBS, start by confirming that you meet the eligibility requirements and have the resources to set it up and maintain it. It can also help to speak with an experienced ROBS provider. Many offer free consultations and can explain how the process works, what compliance involves, and whether this approach makes sense for your specific situation.

If you think a ROBS might work for you, consider the following criteria:

- Your business is, or will be, structured as a C Corporation (C-corp): One of the core requirements of a ROBS is that your business must be a C-corp. This is to allow the company to have shareholders and the subsequent purchase of stock, which will allow you access to the funds.

- You have a large retirement account balance: With most ROBS providers, you’ll need a minimum balance of $50,000 to be eligible. This is largely done to ensure you are not charged excessive fees in relation to the amount being rolled over.

- You don’t want monthly loan payments: Since a ROBS is not a loan, you won’t have to make monthly payments. This can help from a cash flow perspective and also save you on interest charges.

- You are comfortable risking your retirement account balance: If your business fails, you also risk losing the retirement funds used in the rollover.

- You’re unable to qualify for a business loan: Most business loans have requirements for things like credit score, time in business, and revenue. A ROBS has no such criteria, which is why we also identified it as one of the best ways to fund a startup.

Summary of typical rates, terms & qualifications

| Typical rates & terms | |

|---|---|

| Interest rate | None |

| Repayment term | None |

| Initial setup fee | $0 to $8,000 |

| Ongoing maintenance fee | $0 to $150 monthly |

| Funding speed | 2 to 4 weeks |

| Typical qualifications | |

| Minimum balance to qualify | $50,000, but may be flexible |

| Required credit score | None |

| Required time in business | None |

| RRequired business revenue | None |

How to get a ROBS

As a ROBS can be a complex transaction to maneuver, I recommend working with an experienced ROBS provider. In addition to Guidant Financial, you can also consider our other recommendations for the best ROBS companies.

That said, a ROBS transaction can be simplified into the following six steps.

- Step 1: Establish a C-corp.

- Step 2: Create a retirement plan within the C-corp.

- Step 3: Choose a custodian for the retirement plan (check out our picks for the best 401(k) companies).

- Step 4: Rollover funds from personal retirement accounts to the C-corp’s retirement plan.

- Step 5: Have the C-corp’s retirement plan purchase stock in the company.

- Step 6: Utilize available funds for business purposes.

If you’re looking for additional details for each stage, you can reference our ROBS guide.

Using a 401(k) loan

How a 401(k) loan works

A 401(k) loan allows you to borrow against the balance in your 401(k) retirement account. IRS rules typically limit the amount you can borrow to either 50% of your vested balance or $50,000, whichever is less.

Repayments are typically made quarterly and are expected to be paid in full within five years from loan origination. Although 401(k) loans carry an interest rate, that interest is repaid to your retirement account.

One important detail is that these loans are tied to your employer’s plan. If you leave your job, you may have to repay the remaining balance much sooner. In many cases, you’ll have until the due date of your next federal tax return to pay it off.

Pros & cons

| PROS | CONS |

|---|---|

| Less complicated than a ROBS | Could face large tax and early withdrawal penalties if money isn’t repaid |

| Interest repaid is increased contributions to your retirement account | Hurts cash flow because you have loan payments to account for |

| Business isn’t restricted to a C-corp; can be organized in any manner | Only an option with 401(k); cannot take out a loan against an individual retirement account (IRA) |

Who should consider a 401(k) loan

For business owners looking to utilize a 401(k) loan, there are a few instances in which it may be most applicable. This may include scenarios where:

- You have a sufficiently large balance in your 401(k): Since 401(k) loans are limited to the lesser of 50% of your vested balance or $50,000, you’ll want to ensure that it will be enough to satisfy your funding needs.

- You don’t anticipate separating from your employer in the short term: Since you’d have to repay the loan on an accelerated timeline if you separated from your employer, I recommend this as an option only if you don’t foresee any short-term changes in employment.

- You have the ability to repay the loan quickly if needed: Since you’d have a shorter period to pay off the loan if you separated from your employer, it’s a good idea to also have other means to complete a full payoff just as a backup plan.

- You don’t qualify for a business loan: A 401(k) loan rarely has requirements for things like credit scores or income, which makes it a good option if you’re unable to get a business loan.

Summary of typical rates, terms & qualifications

| Typical rates & terms | |

|---|---|

| Interest rate | Prime plus 1% to 2% |

| Loanamount | 50% of vested 401(k) balance or $50,000, whichever is less |

| Repayment term | 5 years |

| Fundingspeed | 1 to 3 weeks |

| Typical qualifications | |

| Required credit score | None |

| Required time in business | None |

| Required business revenue | None |

How to get a 401(k) loan

Getting a 401(k) loan is typically facilitated by your plan’s administrator, so there are nuances in applicable financing steps. In general, however, you’ll need to go through the following:

- Step 1: Contact your plan’s administrator with your loan request.

- Step 2: Review terms and complete the required paperwork with the details of your funding request.

- Step 3: Verify receipt of funds.

- Step 4: Verify regular payments through payroll deductions or other methods as allowed by your plan administrator.

Using a 401(k) withdrawal

How a 401(k) withdrawal works

By using a 401(k) withdrawal, you can access the vested portion of your 401(k) account balance. However, it’s important to keep in mind that this option is typically associated with hefty penalties, fees, and taxes.

401(k) accounts are designed for retirement, so the IRS assesses an additional income tax of 10% on withdrawals made prior to the age of 59.5. Since the funds you withdraw may also be taxed as regular income, your plan administrator could also be required to withhold 20% for federal taxes.

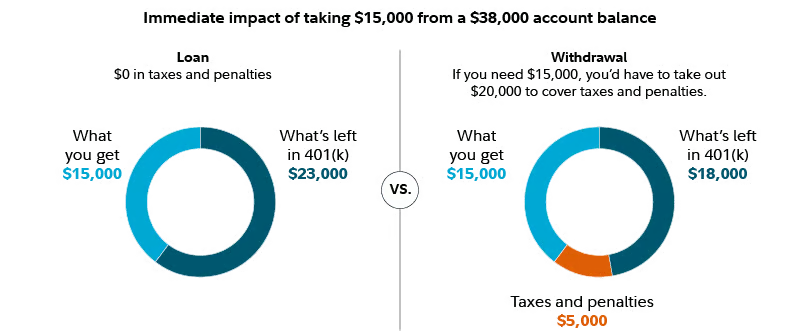

To illustrate the impact that penalties and taxes could have on a 401(k) loan versus an early withdrawal, Fidelity provides an example of how an individual would need to take out nearly $23,000 just to net $15,000 in funds. See the graphic below.

Although the precise amounts can vary depending on your unique circumstances, the key takeaway is that the amount of taxes and penalties can quickly lower the amount of the final check you receive.

Pros & cons

| PROS | CONS |

|---|---|

| Can potentially get a larger sum of money without having to repay a loan | Can face substantial tax liabilities and penalties for early withdrawal |

| No restrictions on how your business is organized | Could place you in a higher tax bracket, causing a larger tax burden |

| Funds could be used for both personal and business expenses | May be risking your future ability to retire if the business fails and retirement funds are lost |

Who should consider a 401(k) withdrawal

In most cases, a 401(k) withdrawal is best treated as a last resort, especially if you’re under age 59.5 and would face taxes and early withdrawal penalties. That said, it may be worth considering if any of the following apply to you:

- You have an urgent need for funds and cannot get financing elsewhere: If you need funds quickly to cover an emergency but cannot get approved for a loan, a 401(k) withdrawal can be an option, as it does not have any credit or income requirements.

- You have reached retirement age: If you’ve already reached the age of retirement, you can avoid the penalties associated with an early withdrawal. However, be aware that the funds you get may still be taxed as ordinary income.

- You qualify for an exception to be exempt from penalties: The IRS has a list of exceptions to the 10% additional tax that will exempt you from paying an early withdrawal penalty. However, no exemptions are listed for utilizing funds for starting up a business, covering regular business expenses, or acquiring another company.

Summary of typical rates, terms & qualifications

| Typical rates & Tterms | |

|---|---|

| Interest rate | None |

| Funding amount | Your current vested 401(k) balance |

| Penalties and fees | 10% penalty may apply prior to age 59.5, in addition to federal and state income tax |

| Repayment term | None |

| Funding speed | 1 to 2 weeks |

| Typical qualifications | |

| Required credit score | None |

| Required time in business | None |

| Required business revenue | None |

How to complete a 401(k) withdrawal

Depending on your employer and/or the retirement plan’s administrator, the steps involved with a 401(k) withdrawal may differ. However, generally, the process is as follows:

- Step 1: Contact your employer or the plan’s administrator with your request.

- Step 2: Review any disclosures you’re provided and complete your plan’s paperwork for a withdrawal request.

- Step 3: Verify receipt of funds.

Risks to consider with 401(k) business funding

Using a 401(k) to finance your business comes with a few risks for you to keep in mind before you pursue this option. This can include:

- Losing your retirement savings: If you mismanage your business finances, you could potentially lose your retirement savings in the event you can’t recoup your financial losses. This is a big risk from a personal finance perspective, as you could impact your future financial stability by investing your retirement funds into your business.

- Penalties and fees: Depending on the financing type and administrator, there may be hefty penalties or fees associated with financing your business with a 401(k). Be sure to read the fine print before entering into any agreements.

- Compliance with IRS regulations: There are certain rules and regulations to be mindful of to ensure you’re in compliance with the IRS. It’s worth consulting a professional who may be able to help you navigate the financing process.

- Employment-related risk: If you use a 401(k) loan and leave your employer, you may be required to repay the loan quickly or face taxes and penalties.

- Ongoing administrative burden: Options like ROBS require ongoing plan administration, reporting, and documentation. Failing to keep up with these responsibilities can create compliance issues and added costs.

Alternatives to 401(k) business funding

If you don’t qualify to use your 401(k), or if the available balance isn’t enough to cover your business plans, you may be better served by another financing option. If you’re leaning toward a traditional business loan, our guide on how to get a small business loan can help you understand the process, improve your approval chances, and move to funding faster.

That said, here are a few alternatives to consider:

Roth IRA

This is another type of retirement account that you can draw funds from for virtually any purpose. The great thing about a Roth IRA, however, is that you are allowed to withdraw your contributions tax- and penalty-free regardless of whether you’re of retirement age or not. And, because it’s not a loan, there aren’t any eligibility requirements you’d need to meet. You could almost look at this like a bit of a savings account, as long as you don’t withdraw your actual earnings.

This is because in a Roth IRA, you’ve already paid taxes on the money you’ve contributed. Now the only tricky thing might be to determine how much you can safely withdraw. Your IRA administrator, however, should have documentation outlining your account’s historical gains and contributions to help you determine the IRA balance that consists of contributions and the balance that consists of earnings.

Personal loan

In some cases, you can get up to $100,000 or more in funding on a personal loan. Qualification requirements typically focus more on your personal credit and finances rather than those of your business. Check out our picks of the best personal loans for business funding.

Home equity loan (HELOAN) or home equity line of credit (HELOC)

These are good options if you have good personal credit, finances, and sufficient equity in your home. Funds can be used for nearly any business purpose, and you can check out our separate guides on getting a HELOAN to finance your business and using a HELOC to fund your business to learn more about how to get this type of financing.

Friends and family

A big benefit of asking friends and family for funding is that you can bypass many of the typical requirements associated with getting a loan from a bank. With that being said, there are still tax regulations to follow, and it can run the risk of straining relationships if the business venture does not succeed. To learn more, read our guide on raising money from friends and family to fund your business.

Angel investors

Angel investors are suitable for early-stage businesses seeking capital without taking on debt. These investors offer seed money in exchange for equity in your company, which can make it a great option for businesses with limited credit history and financial resources. To learn more, read our guide on how to raise angel funding for your business.

Frequently asked questions (FAQs)

Is it a good idea to use a 401(k) for business financing?

This depends, and there’s always a risk. By using your 401(k) for business financing, you could give your company a better chance of growing. However, you may also run the risk of losing your funds altogether or experiencing a setback in your retirement plan if the investment in the business does not go according to plan.

How can I use my 401(k) for business financing?

Three popular options include: taking a loan against your account, withdrawing funds, or using a ROBS to withdraw funds as a way to bypass any potential taxes or early withdrawal penalties. Each, however, has its own set of pros and cons, and some may not be suitable for your needs and circumstances.

What is the maximum amount of money I can get from a 401(k) loan?

In general, you’ll be limited to 50% of your vested balance, or $50,000, whichever is less. If that won’t be a sufficient amount of funding for your business needs, you can always combine it with an alternative method of funding or financing, such as withdrawing from other retirement accounts that may not be subject to taxes or penalties (such as a Roth IRA), seeking funding from friends or family, or getting a personal loan for business purposes.

Are there penalties for using a 401k to buy a business?

If you’re not careful, you could be subject to hefty fines and penalties. For example, a ROBS requires you to navigate multiple areas of tax rules and regulations in order to avoid the usual taxes and penalties associated with touching your retirement funds. Other methods, such as taking a 401(k) withdrawal, could come with income tax responsibilities and early withdrawal penalties if done before you have reached the age of retirement.

Bottom line

If you plan to use a 401(k) to start or buy a business, it’s important to understand each option and the risks that come with it. You’ll also want to weigh the potential impact on your retirement savings and compare these approaches with other financing options before moving forward.

If you’re considering 401(k) business financing, we recommend speaking with a company like Guidant Financial. It is a specialist in 401(k) business financing and offers different types of funding options such as SBA loans, franchise financing, unsecured loans, and equipment leasing. You can set up a free consultation session to discuss your needs and see if it can offer a suitable form of funding for you.