Tired of fraudsters stealing your credit card information and using it to make purchases on your account? Enter virtual credit cards, one way to combat this type of fraud!

So what is a virtual credit card? A virtual credit card is like a substitute for your regular credit card, but it’s still linked to your regular, permanent credit card account. For individual consumers, virtual cards are often used as an additional layer of security as they allow you to conduct transactions without having to give out your regular credit card number.

As a business owner, virtual credit cards can be helpful in managing costs by assigning limits to employee cards, as well as help with accounting for the purposes of tracking and categorizing expenses. Continue reading this guide to learn more details about the pros and cons of virtual credit cards, how they work, and how you can implement them for your personal and business use.

How different types of virtual credit cards work

At a high level, virtual credit cards act as a substitute for your regular credit card. The virtual card is linked to your regular account, so when you make a purchase with it, it will record and post to your regular account. However, they can be structured to work in a number of different ways, such as only being good for a single purchase, a period of time, limiting transactions to certain dollar amounts, or a specific store.

Single-use

A virtual credit card can be generated so that it’s only good for a single transaction. Once used, the virtual card will no longer be valid. This can be useful for consumers who do not want to risk having their account number stolen.

Time-based

Virtual cards can be set up in such a way that they’re only good for a certain period of time. Business owners could use this for company cards to allow employees a window of time to make business-related purchases. This can be especially useful if employees are traveling and are expected to incur travel-related expenses such as meals, airfare, and lodging.

Limited-spend

Credit limits can be set on virtual credit cards such that purchases exceeding a specified dollar amount will not be approved. This is commonly used by businesses that issue employee cards for expenses related to company events for things like meals and lodging, but still want to retain some level of control over the total budget.

Store-specific

Virtual cards can be structured to only be valid at certain vendors or companies. This can be useful if your company frequently makes purchases at a specific store, but also wants to reduce the likelihood of the card being used for fraudulent transactions at other vendors.

Benefits of virtual credit cards

Virtual credit cards carry a number of benefits that consumers and business owners alike may find useful. It can increase the level of security by making it more difficult for fraudulent transactions to occur, and it can also allow business owners to more easily manage employee cards and track expenses.

Security

Virtual cards allow you to make purchases without sharing your regular, permanent credit card account number. This gives you a greater level of protection against fraud because even if your number is compromised or stolen, it will either be impossible or difficult for the fraudsters to use the card, especially if it was set for single-use only.

Personally, I’m also an advocate of using credit cards over other forms of payment, such as debit cards, as it’s less of a hassle to try and recover funds from fraudulent transactions. Many credit cards also have rewards programs to help offset your business expenses, and we talk about this and other benefits in our comparison of

.

Expense management

Virtual card numbers can allow business owners to have more control over company expenses and stay within budget. This is made possible through features like being able to set spending limits on individual cards, set restrictions that allow cards only to be used at certain vendors, and easily issue new virtual cards and deactivate unused cards all at the same time.

If you’re a business owner looking for these features to more easily manage employee cards, I recommend working with a company like Ramp. Ramp makes it easy to manage a fleet of virtual cards, including the ability to create accounts, remove cards, and set spending restrictions.

Convenience

Virtual card numbers don’t require a physical card to make a purchase. This can come in handy if you’ve forgotten or temporarily misplaced your credit card, as you might be able to use the mobile app on your phone to generate a virtual number to make a time-sensitive purchase.

Downsides of virtual credit cards

There aren’t many downsides to using virtual credit cards. With that being said, they’re really only useful for online purchases, and some stores or vendors may prohibit the use of virtual cards. Additionally, since a virtual card uses a different number than your regular physical, permanent account number, it could cause issues if a merchant needs to match up the number with your physical card in order to verify your identity.

For example, if you purchase tickets to be picked up at will call for a concert, you may be required to show your photo identification along with the same credit card that was used to purchase the tickets. Without a matching credit card, you might not be allowed to pick up the tickets. Similar scenarios could occur if you’re booking a hotel or want to return an item that you purchased in-store, where a matching credit card is required to process the transaction.

How to get a virtual credit card

In order to get a virtual credit card, your card issuer must support and offer this feature. Major credit card issuers offer this, but it also may not be available on certain cards. The exact steps needed to generate a virtual card will vary depending on the issuer, but it should commonly be available as an option in your credit card dashboard.

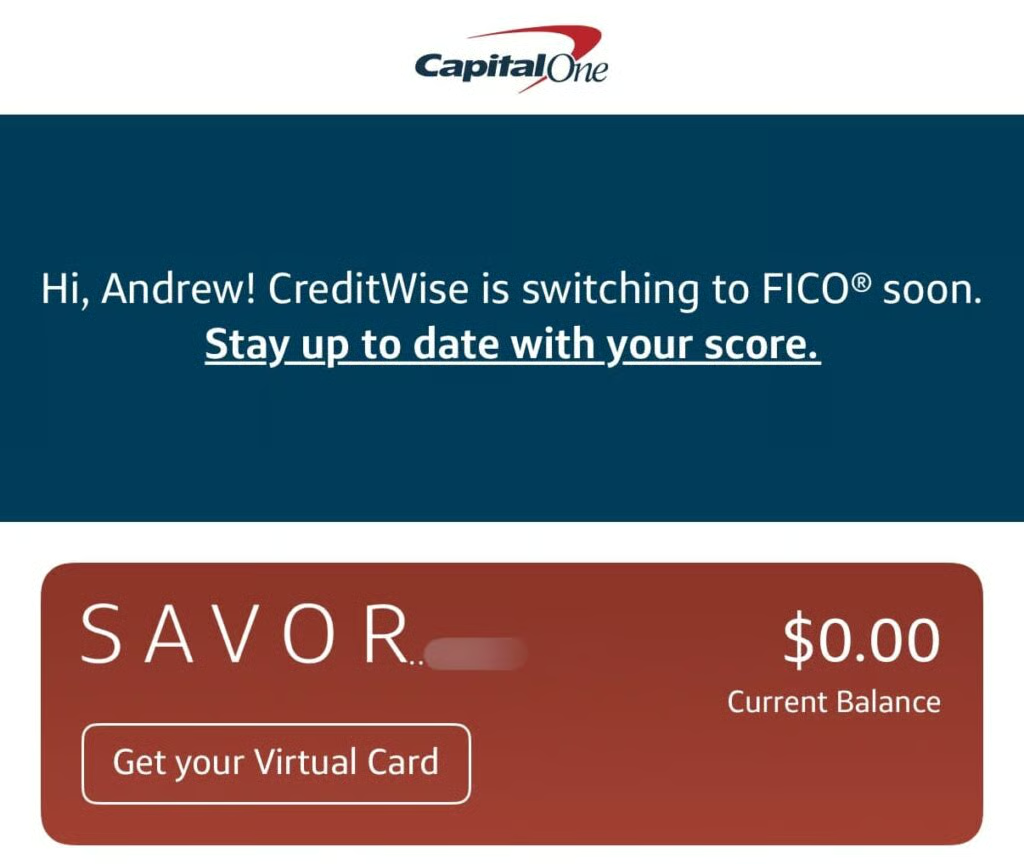

Capital One, for instance, offers virtual card numbers — you can browse our picks of the best Capital One cards to find one suited for your spending habits. A virtual card can be generated through your Capital One online or mobile account; simply tap the button that says “Get Your Virtual Card” below your card balance.

From the Capital One mobile app, you can quickly and easily generate a virtual credit card number at the click of a button. (Source: Andrew Wan, Fit Small Business)

If you don’t currently have a card that supports this feature or are having trouble getting approved for one that does, the tips listed in our guide on

how to get a business credit card

can help you improve your odds of landing an approval.

Frequently asked questions (FAQs)

Can I set spending limits on a virtual credit card?

Yes. This is actually one of the key benefits of a virtual credit card, as business owners can partner with companies like Ramp in order to have greater visibility and control of company expenses when issuing employee credit cards.

Can I use a virtual credit card for recurring subscription payments?

Yes. Virtual credit cards can be used for recurring subscriptions as long as they are set up correctly. Make sure that the virtual card will allow for multiple transactions for a sufficiently high dollar amount, and does not expire after a certain period of time if you plan on keeping the subscription for the long term.

Is it safe to use a virtual credit card?

Yes. In fact, security is a common reason that individual consumers and business owners use virtual credit cards. Virtual cards can be set to be used only for a single transaction, making the account number useless for future purchases even if it is stolen or compromised.

Bottom line

Virtual credit cards can provide an extra layer of security, as well as allow business owners to more easily manage and track expenses for employee cards. Most major credit card companies offer the ability to generate a virtual credit card quickly and easily, and because it’s tied to your regular permanent account number, you’ll still get all of the same benefits and protections.