IRS Form 1125-A is used by corporations, partnerships, and multimember limited liability companies (LLCs)―filers of Forms 1120, 1120-C, 1120-F, 1120-S, or 1065―to calculate their cost of goods sold (COGS) for the year. It applies to businesses that sell products while businesses that sell services generally don’t need it—unless they also sell parts and supplies.

Example of Completing Form 1125-A

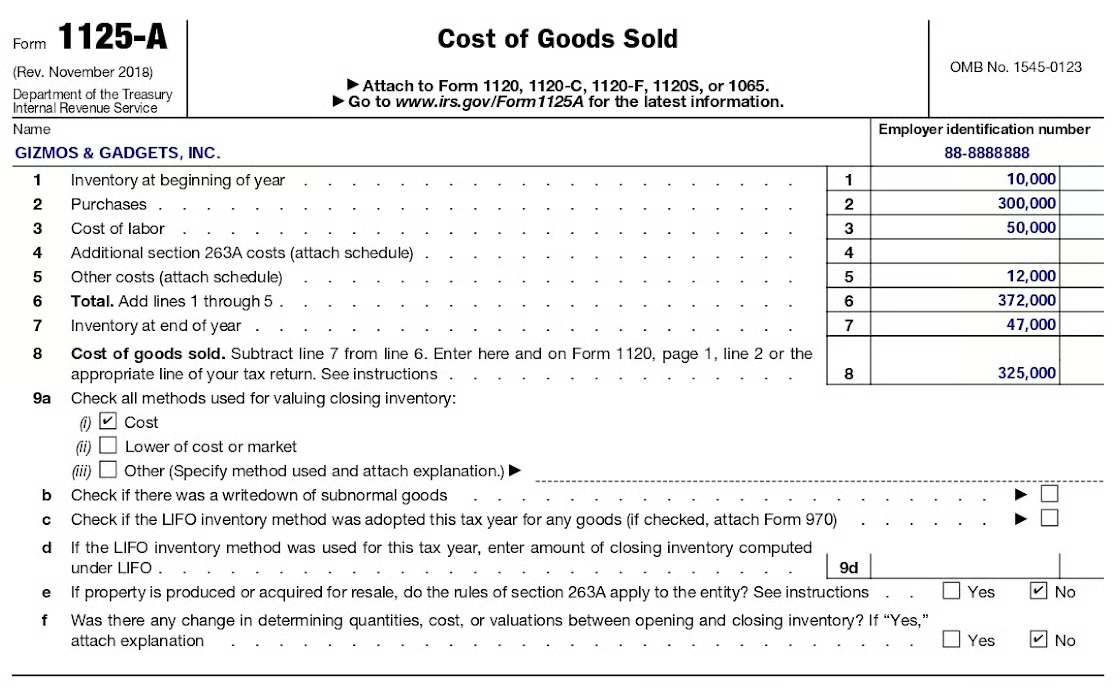

Gizmos & Gadgets (G&G) used the following activity to complete Form 1125-A for 2024:

- Gross receipts – 2023: $500,000

- Gross receipts – 2022: $450,000

- Gross receipts – 2021: $400,000

- Average gross receipts for 3 prior years: $450,000

- Beginning of year inventory: $10,000

- Purchases: $300,000

- Cost of labor: $50,000

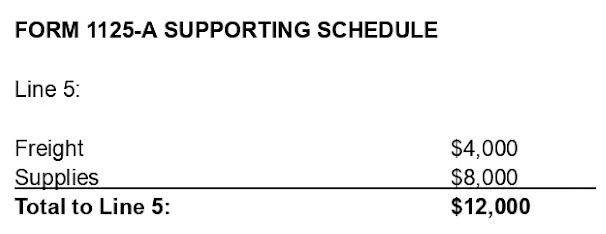

- Freight: 4,000

- Supplies: 8,000

- End of year inventory: $47,000

With average gross receipts of $450,000, G&G qualifies as a small taxpayer and has some flexibility in how it calculates and reports inventory for taxes. G&G decides to continue its practice from prior years of valuing inventory for tax purposes the same as for its books, which is one of the methods allowed for small taxpayers.

- Line 1: The book value of the inventory that G&G held at the beginning of the year is reported here.

- Line 2: The business purchased $300,000 in inventory during the year and reported that total on line 2.

- Line 3: G&G used this line to report the salaries and wages paid for work involved in producing the company’s products for sale.

- Line 4: Section 263A requires that costs be capitalized

- Line 5: This line is for costs not listed elsewhere on the form. These might include supplies, freight, storage, and overhead. A schedule of these costs must be attached.

G&G’s attachment is shown here:

- Line 6: Sum lines 1 through 5.

- Line 7: The book value of the inventory that G&G held at the end of the year was reported here.

| Line 9 Ending Inventory Valuation Options | ||

|---|---|---|

| Line 9a(i)(Cost) | Line 9a(ii)(Lower of Cost or Market) | Line 9a(iii) (Other) |

| Inventory valued at the cost paid to obtain the items calculated using AVCO, LIFO, FIFO, or specific identification. | Inventory valued at the lesser of cost of production or the amount the items could be sold for (market value). | Description of valuation method other than cost or market value (rare). |

- Line 9b: Companies that did not use the AVCO method would check this box if they recorded a reduction in inventory for damaged or unusable inventory. Otherwise, this box would be left blank.

- Line 9c: This box would only be checked if this is the first year that LIFO valuation was used. If it was, then Form 970 would also need to be filed.

- Line 9d: If LIFO was used to value inventory, the ending book value should be entered on this line.

- Line 9e: Generally, Section 263A rules apply to businesses that produce or acquire property for resale. Usually, small taxpayers like G&G are exempt from 263A requirements. When the requirements do not apply, “no” is checked.

- Line 9f: If the business valued ending inventory in a manner different from how beginning inventory was valued, the box on this line should be checked and an explanation should be attached.

How Does Form 1125-A Flow to the Main Tax Form?

The COGS calculated on Form 1125-A, line 8, should carry to the income tax return for the business. For each respective entity, it should be reported on the following lines:

- Partnerships/multimember LLCs: Form 1065, line 2

- S corporations (S-corps): Form 1120-S, line 2

- C corporations (C-corps): Form 1120, line 2

- Cooperative associations: Form 1120-C, line 2

- Foreign corporations: Form 1120-F, Part II, line 2

How to File Form 1125-A?

Form 1125-A is filed with the main income tax form (1120, 1120-C, 1120-F, 1120-S, or 1065) by the due date of the main form.

Frequently Asked Questions (FAQs)

What are purchases on Form 1125-A?

Purchases are additions to inventory, acquired throughout the year. They can consist of purchases of finished goods for resale or raw materials for manufacturing.

What does the IRS consider cost of goods sold?

COGS is calculated by adding beginning inventory to purchases and subtracting ending inventory. Form 1125-A combines basic COGS with form-specific adjustments.

How should business expenses related to COGS be reported on Schedule C?

Expenses related to COGS should be reported in Part III of Schedule C, which will then flow to line 4 in Part I. When you include expenses in COGS, those expenses cannot also be taken as deductions elsewhere on the form.

Bottom Line

Form 1125-A is used to calculate the COGS that are then carried to the taxpayer’s main income tax form. Reference the IRS Form 1125-A instructions for additional details on what should be included.