Form 4797 is used to report sales of business property commonly referred to as section 1231 property. Section 1231 property includes assets used in your business, such as buildings, machinery, and equipment, but excludes assets held as investments or inventory.

Determining the gain or loss on section 1231 property is straightforward. However, determining whether that gain or loss is characterized as ordinary or capital is very complicated. The purpose of Form 4797 is to make this difficult determination, so you must pay strict attention to the line item instructions.

Basic Example of Completed Form 4797

To illustrate how to complete Form 4797, let’s consider the following property transactions

| Description | Purchased | Sold | Sales Price | Cost | Depreciation | Gain / (Loss) |

|---|---|---|---|---|---|---|

| Land | 1/1/2020 | 7/4/2023 | 75,000 | 20,000 | 0 | 55,000 |

| Building | 1/1/2020 | 7/4/2023 | 305,000 | 275,000 | 30,000 | 60,000 |

| Equipment A | 8/5/2021 | 1/22/2023 | 10,000 | 23,000 | 6,000 | (7,000) |

| Equipment B | 4/5/2023 | 11/11/2023 | 10,000 | 15,000 | 3,000 | (2,000) |

| Equipment C | 4/1/2019 | 6/30/2023 | 12,000 | 50,000 | 50,000 | 12,000 |

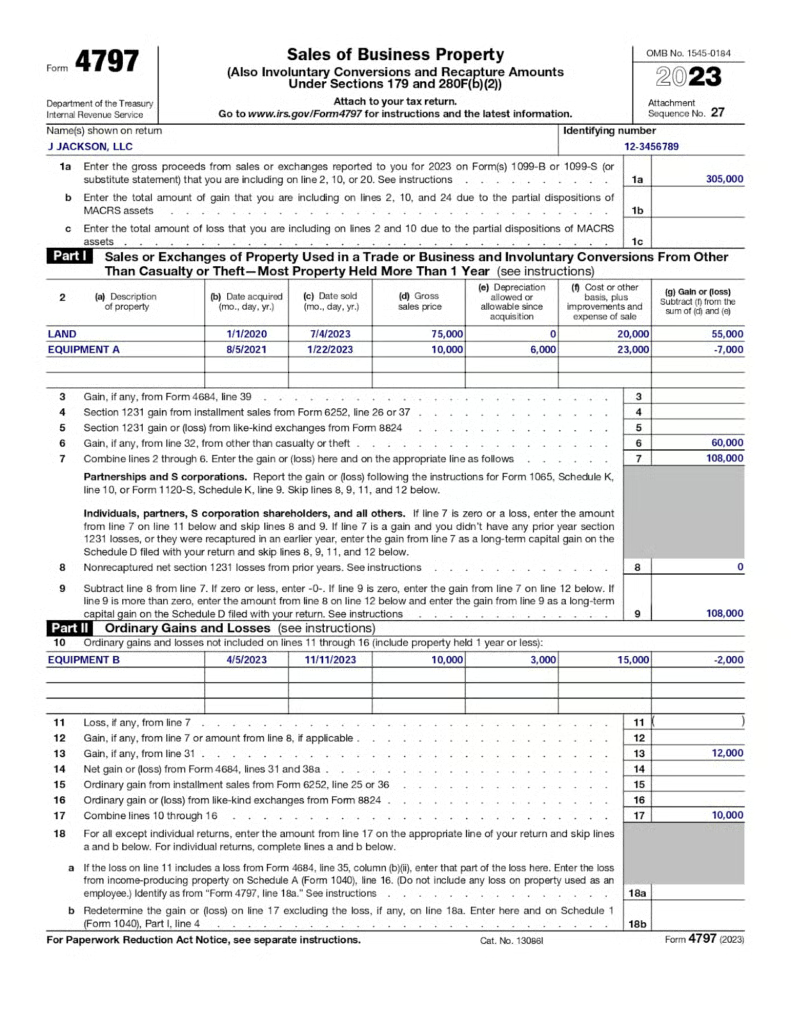

Below is a sample Form 4797 completed with the five property transactions. Next, we’ll discuss how we determined where to report each transaction and how we completed each part.

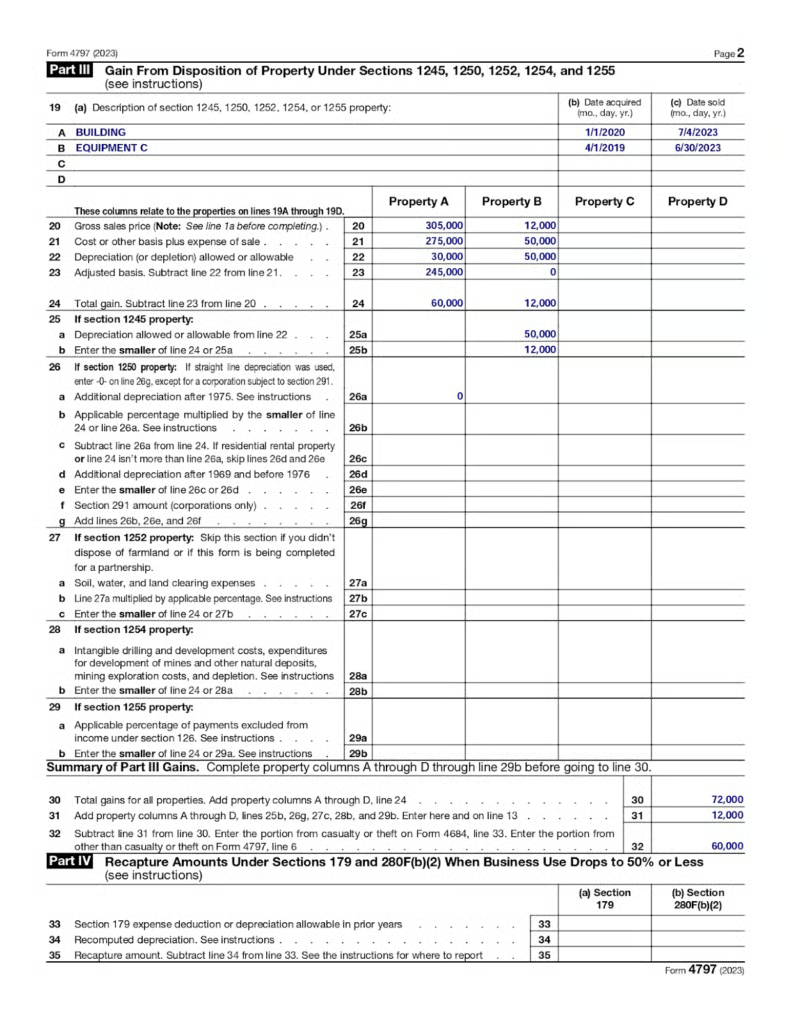

Form 4797 Part III

Completion of Form 4797 should start with Part III. The results from Part III will flow to either Part I or Part II—or possibly both. Only sales of depreciable 1231 property resulting in a gain should be reported in Part III. Looking at our sample transactions, this will include the building and equipment C.

The important thing to understand is which lines to complete based on the type of property. Complete lines 19 through 24 for all transactions.

You must complete only one of lines 25 through 29 based on the type of property that was sold as follows:

- Line 25: Section 1245 property

- Line 26: Section 1250 property

- Line 27: Section 1252 property

- Line 28: Section 1254 property

- Line 29: Section 1255 property

All of these property types are subsets of section 1231 property in general. The tax rules for separating their gains into 1231 gain and ordinary income differ, which is why they must be calculated on different lines of the form.

Click through the headers below for quick definitions of each property type.

§1245 Property

Section 1245 property is the most common subset of 1231 property and consists of depreciable machinery, equipment, furniture, and similar non-real property used for business.

In our example, Equipment A, B, and C are all 1245 property, but only Equipment B is reported in Part II because it is the only equipment held for more than a year and sold at a gain. For Equipment C, the separation of gain into its two components is done on line 25.

§1250 Property

Section 1250 property is depreciable real estate, both commercial and residential. Section 1250 property excludes land since land is not depreciable. It also excludes land that is held as an investment since that is not a 1231 asset.

In our example, the building is section 1250 property—and the gain is separated into its component parts on line 26.

§1252 Property

Section 1252 property is farmland held for less than 10 years. The gain is separated on line 27.

§1254 Property

Certain drilling, mining, and exploration costs are considered section 1254 property, which is rare. Qualifying costs are defined in sections 263, 616, and 617 of the IRS Code.

§1255 Property

Section 1255 property is rare and generally consists of land improvements partially sponsored through government cost-sharing programs. The gain on the sale of these land improvements may partially be taxed as ordinary income, as calculated on line 29.

- Lines 30 through 32 at the bottom of Part III summarize the total gains on all property and the portion of the gains that will be treated as Section 1231 gains and ordinary income.

- Line 31 is the portion of the gains to be treated as ordinary income and flows to Part II of the form.

- Line 32 is the portion taxed as Section 1231 gain and flows to Part I of the form.

Form 4797 Part I

Part I is used to report the sale of property where the total gain or loss will always be treated as Section 1231 gain or loss. This includes two main types of property:

- Nondepreciable 1231 property, which is most commonly land.

- Depreciable 1231 property sold at a loss.

From our example, the sale of the land for a gain and the sale of Equipment A at a loss are both reported in Part I. Part I line 6 reports the $60,000 1231 gain calculated in Part III and reported on line 32.

Form 4797 Part II

Part II reports only business assets that are sold prior to owning for one year. For our example, Equipment B is reported in Part II because it was not owned for a year. It would be reported in Part II whether it generated a gain or a loss.

The $12,000 of ordinary income calculated in Part III and reported on line 31 is included in Part II line 13.

Form 4797 Part IV

Section IV flows to or from the other sections of Form 4797. Its purpose is to recapture excess depreciation when an asset goes from above 50% business use to below 50% business use:

- Assets with business use of 50% or less do not qualify for accelerated depreciation methods like Section 179 or MACRS depreciation.

- If assets are initially used for greater than 50% business but then subsequently fall to below 50% business use, then the accelerated depreciation claimed must be included in ordinary income.

- When assets drop to 50% business use or less, the depreciation recapture must be calculated in Part IV.

Which Parts of Form 4797 Should You Complete?

As illustrated above, it’s vital that you report all asset sales in the appropriate part of the form. The chart below summarizes the appropriate sections that should be completed, based on the property type and length of ownership of the property sold.

| Property Type | Form 4797 Input Section by Holding Period | |||

|---|---|---|---|---|

| More Than 12 Months | 12 Months or Less | |||

| Gain | Loss | Gain | Loss | |

| Depreciable Furniture, Machinery, Equipment & Similar Property (1245 Property) | Part III Line 25

| Part I | Part II | Part II |

| Depreciable Buildings (1250 Property) | Part III Line 26 | Part I | Part II | Part II |

| Land Used for Business | Part I | Part I | Part II | Part II |

| Farmland Owned Less Than 10 Years (1252 Property) | Part III Line 27 | Part I | Part II | Part II |

| Farmland Owned More Than 10 Years | Part I | Part I | Part II | Part II |

| Drilling, Mining, Exploration Costs (1254 Property) | Part III Line 28 | Part I | Part II | Part III |

| Cost-sharing Property (1255 Property) | Part III Line 29 | Part I | Part II | Part II |

Filing Form 4797

Who Should File?

Form 4797 should be filed by taxpayers who sold business property during the tax year on the form. Applicable taxpayers include individuals and entities filing the following forms:

- 1065: Partnership and multimember limited liability company (LLC)

- 1120: C-corporation (C-corp)

- 1120S: S-corporation (S-corp)

- 1040: Individuals

How To File

Form 4797 is included with the main income tax form for the taxpayer and has the same due date as the main form.

Frequently Asked Questions (FAQs)

What is Form 4797 used for when selling a business?

The sale of a business can be structured as a stock sale or an asset sale. When the transfer of ownership is done by way of an asset sale, Form 4797 would be used to report the sale of those assets.

What is the difference between Form 4797 and Form 8949?

Form 4797 is used to report the sale of property used in a trade or business. Meanwhile, Form 8949 lists the individual transactions summarized on Schedule D. Sale of investment property is reported on Schedule D.

What is the difference between Schedule D and Form 4797?

Schedule D is used to report the sale of investment property while Form 4797 is used to report the sale of business property.

Bottom Line

Form 4797 is used to report the sale of property used in a trade or business. Business property may have different classifications, and the sale of business property may result in gains that must be reported separately in different parts of Form 4797.