There are two main components of a bank statement reconciliation. First, ensure that all transactions on your bank statement appear on your check register. Then, see to it that the remaining transactions in your check register are recorded properly, even though they haven’t cleared the bank.

I’ll break those two components into five easy steps, from reconciling the prior period and gathering documents to reconciling balances and creating the reconciliation statement, to illustrate how to do bank reconciliation manually. I’ll also show you how you can do it easily using QuickBooks Online.

- Step 1: Reconcile the prior period and gather documents.

- Step 2: Trace deposits to the register.

- Step 3: Trace withdrawals to the register.

- Step 4: Enter missing transactions into the register.

- Step 5: Reconcile balances and create the reconciliation statement.

- Reconciling bank accounts in QuickBooks Online

- The importance of reconciling a bank statement

- Common bank reconciliation errors and how to fix them

- Frequently asked questions (FAQs)

Step 1: Reconcile the prior period and gather documents.

Begin reconciliation from either the last time the account was reconciled or the account’s opening, if it has never been reconciled.

Gather these documents:

- Bank statement

- Check register

- Previous reconciliation statement

For example, here is a bank statement from a fictitious institution, First Capital Bank.

| CHECKING ACCOUNT STATEMENT PAUL’S PLUMBING355 Lexington Ave., 18th FloorNew York, NY 10017 | ||||

|---|---|---|---|---|---|

| 228 Park Ave S # 20702New York, NY 10003-15021-800-555-5555PO BOX 4000 | Statement Period: June 1, 2022 to June 30, 2022 | ||||

| Date | Description | Ref. | Withdrawals | Deposits | Balance |

| 06-01-2022 | Bank statement beginning bal. | 10,000 | |||

| 06-03-2022 | Local Phone Company - Visa | 9655 | 250 | 9,750 | |

| 06-08-2022 | Check No. 100 | 1,000 | 8,750 | ||

| 06-09-2022 | Check No. 101 | 350 | 8,400 | ||

| 06-15-2022 | Cash Deposit | 2297 | 5,400 | 13,800 | |

| 06-17-2022 | Check No. 103 | 2,100 | 11,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 8,700 | |

| 06-20-2022 | Cash Deposit | 2298 | 1,500 | 10,200 | |

| 06-24-2022 | Check No. 105 | 800 | 9,400 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 9,280 | |

| 06-29-2022 | Kristen Berman - Payment | 3332

| 700 | 9,980 | |

| 06-30-2022 | Bank service charges | 10 | 9,970 | ||

| BANK STATEMENT ENDING BALANCE | 9,970 | ||||

Below is the check register of First Capital Bank’s checking account in the books of Paul’s Plumbing:

| CHECK REGISTER - FIRST CAPITAL BANKAccount No.: 321-0000-9874From June 1, 2022 to June 30, 2022 | |||||

|---|---|---|---|---|---|

| Date | Description | Ref. | Debit | Credit | Balance |

| 06-01-2022 | Beginning balance | 9,000 | |||

| 06-03-2022 | Local Phone Company Payment - Visa | 9655 | 250 | 8,750 | |

| 06-06-2022 | Check # 101 - Business Supply Center | 350 | 8,400 | ||

| 06-08-2022 | Check # 102 - Cecil’s Lockworks | 200 | 8,200 | ||

| 06-10-2022 | Check # 103 - Foster Lighting | 2,100 | 6,100 | ||

| 06-14-2022 | Cash collections deposited | 2297 | 5,400 | 11,500 | |

| 06-16-2022 | Check # 104 - Novello Lights Magazine | 1,800 | 9,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 6,700 | |

| 06-19-2022 | Cash collections deposited | 2298 | 1,500 | 8,200 | |

| 06-21-2022 | Check # 105 - 123 Plumbing Supply | 800 | 7,400 | ||

| 06-24-2022 | Check # 106 - Joe Plumber | 200 | 7,200 | ||

| 06-26-2022 | Check # 107 - Office Supply Store | 500 | 6,700 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 6,580 | |

| 06-30-2022 | Cash collections deposited | 2299 | 5,220 | 11,800 | |

| CHECK REGISTER BALANCE | 11,800 | ||||

At first glance, the June ending bank statement balance ($9,970) and the check register balance ($11,800) do not match. Because book and bank records capture transactions at different times, you need to perform a bank reconciliation to account for unrecorded items in both sets of records.

Before starting the June reconciliation, review the May reconciliation shown below. Notice that check No. 100 for $1,000 was listed as a reconciling item. If it does not clear in June, it will remain a reconciling item in the June reconciliation. This step shows why reviewing the prior month’s reconciliation is essential.

| PAUL’S PLUMBINGBANK RECONCILIATIONFIRST CAPITAL BANK, MAY 31, 2022 | ||

|---|---|---|

| Balance per bank statement as of May 31, 2022 | 10,000 | |

| Add: Deposits in transit | - | |

| Deduct: Outstanding Checks | ||

| (1,000) | (1,000) |

| Balance per Check Register | 9,000 | |

Step 2: Trace deposits to the register.

Deposits must appear in both the bank statement and the check register. Any deposit that appears in only one record becomes a reconciling item. Follow these guidelines to analyze deposits:

- Deposits in the register but not on the bank statement: These are often timing differences if deposited at the end of the month. If not, investigate for possible errors by the bank or in the check register.

- Deposits on the bank statement but not in the register: These are usually omissions from the check register. Verify the bank deposits are valid, then add them to the register.

Let’s use the sample information below:

| CHECKING ACCOUNT STATEMENT PAUL’S PLUMBING355 Lexington Ave., 18th FloorNew York, NY 10017 | ||||

|---|---|---|---|---|---|

| 228 Park Ave S # 20702New York, NY 10003-15021-800-555-5555PO BOX 4000 | Statement Period: June 1, 2022 to June 30, 2022 | ||||

| Date | Description | Ref. | Withdrawals | Deposits | Balance |

| 06-01-2022 | Bank statement beginning bal. | 10,000 | |||

| 06-03-2022 | Local Phone Company - Visa | 9655 | 250 | 9,750 | |

| 06-08-2022 | Check No. 100 | 1,000 | 8,750 | ||

| 06-09-2022 | Check No. 101 | 350 | 8,400 | ||

| 06-15-2022 | Cash Deposit | 2297 | 5,400 | 13,800 | |

| 06-17-2022 | Check No. 103 | 2,100 | 11,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 8,700 | |

| 06-20-2022 | Cash Deposit | 2298 | 1,500 | 10,200 | |

| 06-24-2022 | Check No. 105 | 800 | 9,400 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 9,280 | |

| 06-29-2022 | Deposit by Kristen Berman | 3332

| 700 | 9,980 | |

| 06-30-2022 | Bank service charges | 10 | 9,970 | ||

| BANK STATEMENT ENDING BALANCE | 9,970 | ||||

Pay attention to the items highlighted in green. Start reconciliation by matching bank statement line items with the check register.

For example, on June 15, the bank statement shows a $5,400 cash deposit with reference number 2297. The check register (see table below) records the same deposit on June 14. Apply the same process for the $1,500 cash deposit and the $700 deposit from Kristen Berman.

| CHECK REGISTER - FIRST CAPITAL BANKAccount No.: 321-0000-9874From June 1, 2022 to June 30, 2022 | |||||

|---|---|---|---|---|---|

| Date | Description | Ref. | Debit | Credit | Balance |

| 06-01-2022 | Beginning balance | 9,000 | |||

| 06-03-2022 | Local Phone Company Payment - Visa | 9655 | 250 | 8,750 | |

| 06-06-2022 | Check # 101 - Business Supply Center | 350 | 8,400 | ||

| 06-08-2022 | Check # 102 - Cecil’s Lockworks | 200 | 8,200 | ||

| 06-10-2022 | Check # 103 - Foster Lighting | 2,100 | 6,100 | ||

| 06-14-2022 | Cash collections deposited | 2297 | 5,400 | 11,500 | |

| 06-16-2022 | Check # 104 - Novello Lights Magazine | 1,800 | 9,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 6,700 | |

| 06-19-2022 | Cash collections deposited | 2298 | 1,500 | 8,200 | |

| 06-21-2022 | Check # 105 - 123 Plumbing Supply | 800 | 7,400 | ||

| 06-24-2022 | Check # 106 - Joe Plumber | 200 | 7,200 | ||

| 06-26-2022 | Check # 107 - Office Supply Store | 500 | 6,700 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 6,580 | |

| 06-30-2022 | Cash collections deposited | 2299 | 5,220 | 11,800 | |

| CHECK REGISTER BALANCE | 11,800 | ||||

The $1,500 cash deposit with reference number 2298 appears in the check register. However, two discrepancies must be addressed:

- A $700 deposit from Kristen Berman appears in the bank statement but not in the check register.

- A $5,220 cash deposit with reference number 2299 appears in the check register but not in the bank statement.

Make these adjustments:

- Deposit by Kristen Berman not recorded in the books: Because the deposit appears in the bank statement, no change is needed to the bank balance. After verifying the deposit is correct, add the $700 to the check register.

- Cash deposit by Paul’s Plumbing not reported in the bank statement: Because the $5,220 deposit appears in the check register but not the bank statement, list it as a reconciling item. This type of reconciling item is called a deposit in transit, meaning the bank has not yet recorded it.

Step 3: Trace withdrawals to the register.

Apply the same concept used in Step 2. Match withdrawals between the bank statement and the check register.

- If a withdrawal shows up on the bank statement but not in the check register, it’s either a book or bank error that needs to be investigated.

- If it’s in the check register but not on the bank statement, it becomes a reconciling item.

The checks shown in the bank statement below are vendor checks issued by Paul’s Plumbing. When the vendors deposited them, the bank recorded deductions in the beginning balance.

| CHECKING ACCOUNT STATEMENT PAUL’S PLUMBING355 Lexington Ave., 18th FloorNew York, NY 10017 | ||||

|---|---|---|---|---|---|

| 228 Park Ave S # 20702New York, NY 10003-15021-800-555-5555PO BOX 4000 | Statement Period: June 1, 2022 to June 30, 2022 | ||||

| Date | Description | Ref. | Withdrawals | Deposits | Balance |

| 06-01-2022 | Bank statement beginning bal. | 10,000 | |||

| 06-03-2022 | Local Phone Company - Visa | 9655 | 250 | 9,750 | |

| 06-08-2022 | Check No. 100 | 1,000 | 8,750 | ||

| 06-09-2022 | Check No. 101 | 350 | 8,400 | ||

| 06-15-2022 | Cash Deposit | 2297 | 5,400 | 13,800 | |

| 06-17-2022 | Check No. 103 | 2,100 | 11,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 8,700 | |

| 06-20-2022 | Cash Deposit | 2298 | 1,500 | 10,200 | |

| 06-24-2022 | Check No. 105 | 800 | 9,400 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 9,280 | |

| 06-29-2022 | Kristen Berman - Payment | 3332

| 700 | 9,980 | |

| 06-30-2022 | Bank service charges | 10 | 9,970 | ||

| BANK STATEMENT ENDING BALANCE | 9,970 | ||||

Match checks in the check register and the bank statement

Match the checks in the check register with those listed on the bank statement. Refer to the cells highlighted in green.

The bank statement above shows check numbers 100, 101, 103, and 105. Notice that check numbers 102 and 104 are missing from the sequence. You also need to verify if Paul’s Plumbing issued any checks beyond check number 105 by reviewing the check register.

| CHECK REGISTER - FIRST CAPITAL BANKAccount No.: 321-0000-9874From June 1, 2022 to June 30, 2022 | |||||

|---|---|---|---|---|---|

| Date | Description | Ref. | Debit | Credit | Balance |

| 06-01-2022 | Beginning balance | 9,000 | |||

| 06-03-2022 | Local Phone Company Payment - Visa | 9655 | 250 | 8,750 | |

| 06-06-2022 | Check # 101 - Business Supply Center | 350 | 8,400 | ||

| 06-08-2022 | Check # 102 - Cecil’s Lockworks | 200 | 8,200 | ||

| 06-10-2022 | Check # 103 - Foster Lighting | 2,100 | 6,100 | ||

| 06-14-2022 | Cash collections deposited | 2297 | 5,400 | 11,500 | |

| 06-16-2022 | Check # 104 - Novello Lights Magazine | 1,800 | 9,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 6,700 | |

| 06-19-2022 | Cash collections deposited | 2298 | 1,500 | 8,200 | |

| 06-21-2022 | Check # 105 - 123 Plumbing Supply | 800 | 7,400 | ||

| 06-24-2022 | Check # 106 - Joe Plumber | 200 | 7,200 | ||

| 06-26-2022 | Check # 107 - Office Supply Store | 500 | 6,700 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 6,580 | |

| 06-30-2022 | Cash collections deposited | 2299 | 5,220 | 11,800 | |

| CHECK REGISTER BALANCE | 11,800 | ||||

The check register shows that Paul’s Plumbing issued seven checks to vendors: 101, 102, 103, 104, 105, 106, and 107.

- Only check numbers 101, 103, and 105 appear in both the check register and the bank statement, so mark them as cleared.

- Check numbers 102, 104, 106, and 107 do not appear in the bank statement, meaning they have not cleared yet.

- Check 100 appears in the bank statement but not in the check register. This check was a reconciling item in May. Now that it has cleared, exclude it from the June reconciliation report.

Direct debits and bank service charges

In addition to outstanding checks, the bank statement shows direct debits and service charges. Refer to the cells highlighted in orange.

- Direct debits via Visa: These include payments for Paul’s Plumbing’s telephone bill (Local Phone Company) and electric bill (NYC Electric). Because both transactions appear in the bank statement and check register, mark them as cleared.

- Bank service charges: The bank statement shows a $10 service fee that does not appear in the check register. Because the charge was omitted from the books, add it to the check register.

How to treat these items in reconciliation:

- Outstanding checks are checks that appear in the check register but not the bank statement. Deduct them from the bank statement balance. In this case, they’re check numbers 102, 104, 106, and 107.

- Bank service charges are minimal fees billed by the bank. Deduct these from the check register balance.

Step 4: Enter missing transactions into the register.

When reconciling, remember that adjustments for missing transactions apply only to items in the bank statement that do not appear in the check register. Do not record journal entries for deposits in transit or outstanding checks.

Common book errors found during reconciliation

Correct the following errors in the accounting records before completing the reconciliation:

- Customer payments made directly to the bank

- Collection of customer notes made through the bank

- Interest earned in the bank account

- Bank service charges

- NSF (nonsufficient funds) checks

In the example, only two book adjustments are required:

- Add the $700 deposit from Kristen Berman to the check register.

- Record the $10 bank service charge in the check register.

| CHECK REGISTER - FIRST CAPITAL BANKAccount No.: 321-0000-9874From June 1, 2022 to June 30, 2022 | |||||

|---|---|---|---|---|---|

| Date | Description | Ref. | Debit | Credit | Balance |

| 06-01-2022 | Beginning balance | 9,000 | |||

| 06-03-2022 | Local Phone Company Payment - Visa | 9655 | 250 | 8,750 | |

| 06-06-2022 | Check # 101 - Business Supply Center | 350 | 8,400 | ||

| 06-08-2022 | Check # 102 - Cecil’s Lockworks | 200 | 8,200 | ||

| 06-10-2022 | Check # 103 - Foster Lighting | 2,100 | 6,100 | ||

| 06-14-2022 | Cash collections deposited | 2297 | 5,400 | 11,500 | |

| 06-16-2022 | Check # 104 - Novello Lights Magazine | 1,800 | 9,700 | ||

| 06-18-2022 | ATM Withdrawal | 1112 | 3,000 | 6,700 | |

| 06-19-2022 | Cash collections deposited | 2298 | 1,500 | 8,200 | |

| 06-21-2022 | Check # 105 - 123 Plumbing Supply | 800 | 7,400 | ||

| 06-24-2022 | Check # 106 - Joe Plumber | 200 | 7,200 | ||

| 06-26-2022 | Check # 107 - Office Supply Store | 500 | 6,700 | ||

| 06-28-2022 | NYC Electric - Visa | 8655 | 120 | 6,580 | |

| 06-30-2022 | Cash collections deposited | 2299 | 5,220 | 11,800 | |

| 06-30-2022 | ADJ: Payment from Kristen Berman via bank | 3332 | 700 | 12,500 | |

| 06-30-2022 | ADJ: Bank service charges | 10 | 12,490 | ||

| CHECK REGISTER BALANCE | 12,490 | ||||

Step 5: Reconcile balances and create the reconciliation statement.

A bank reconciliation statement is a schedule that explains the differences between the bank statement balance and the checking account balance.

You’ll have to choose a format.

- Adjusted balances format: Adjust both the bank and book balances until they match. This is the most common method.

- Bank-to-book format: Adjust only the bank statement balance to arrive at the check register balance. While simpler, this format does not demonstrate equality between bank and book balances.

For this example, I’ll use the adjusted balances format.

| PAUL’S PLUMBINGBANK RECONCILIATIONFIRST CAPITAL BANK, JUNE 30, 2022 | |||

|---|---|---|---|

| Balance per bank statement (Step 1) | 9,970 | ||

| Add: Deposits in transit (Step 2) | 5,220 | ||

| Deduct: Outstanding Checks (Step 3) | |||

| Check no. 102 | 200 | ||

| Check no. 104 | 1,800 | ||

| Check no. 106 | 200 | ||

| Check no. 107 | 500 | (2,700) | 2,520 |

| Balance per Check Register | 12,490 | ||

After reconciling the bank accounts, the true cash balance available to spend is $12,490.

Reconciling bank accounts in QuickBooks Online

Bank reconciliation in QuickBooks Online follows a similar process. However, it will be a little bit easier since the tool will automatically pull up your check register. Knowing how to reconcile bank statements in QuickBooks Online will make the reconciliation process easier and stress-free.

As an example, let’s reconcile accounts using the data from First Capital Bank in QuickBooks Online.

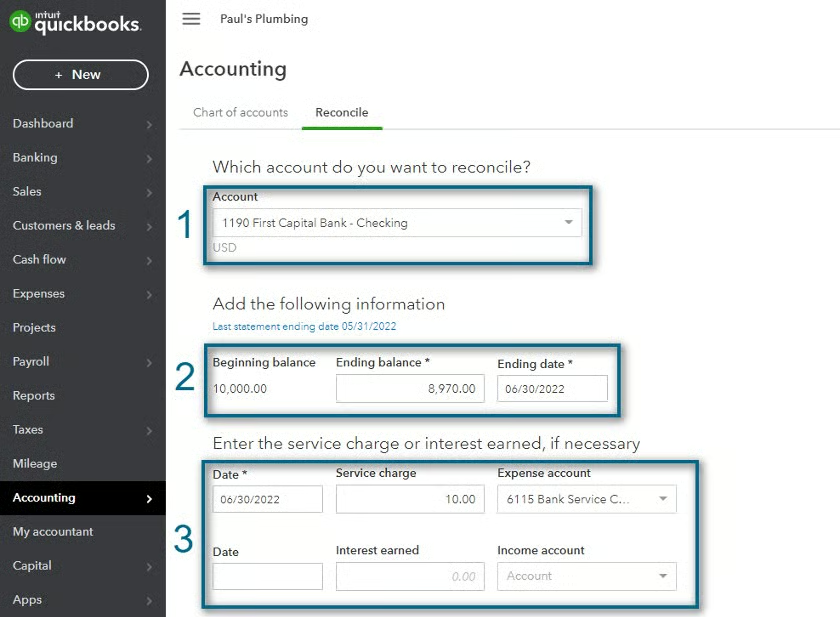

Step 1: Enter bank balance, charges, and interest.

Before you start reconciling in QuickBooks, you need to fill out several fields, as shown in the image below.

- Step 1.1: Choose the account to reconcile. In this example, we use First Capital Bank. For your business, select your checking account.

- Step 1.2: Enter the ending balance from the bank statement. The ending balance in the example above is $9,970.

- Step 1.3: Enter the bank service charges and interest earned. In Paul’s Plumbing’s books, record the $10 fee under the Bank Service Charges account. You may use a different expense account title if appropriate. QuickBooks Online lets you enter bank statement charges at this stage, which eliminates the need to adjust for them later in Step 4.

In this case, no interest was earned, so we skipped that entry. If your bank statement shows interest revenue, record the amount as interest income. Click Start Reconciling when you’re done.

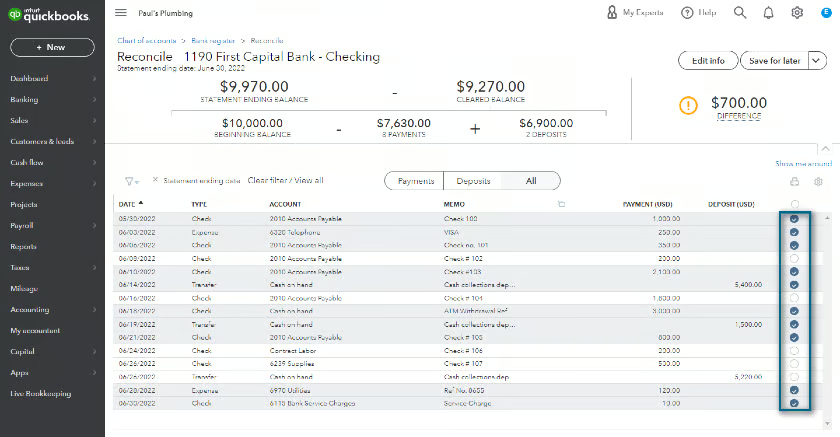

Step 2: Match transactions with the bank statement.

If a transaction appears both in QuickBooks Online and on the bank statement, tick the entry to mark it as cleared. QuickBooks Online will automatically update the cleared balance.

Leave any transaction unticked if it appears only in the QuickBooks Online check register and not on the bank statement. These unticked items remain reconciling items.

Step 3: Record book reconciling items.

In Step 2, you ticked all transactions that appear both on the bank statement and in QuickBooks Online’s check register. However, a $700 difference remains. Reviewing the bank statement shows that Kristen Berman paid $700 directly through the bank. You must record this transaction before completing the reconciliation.

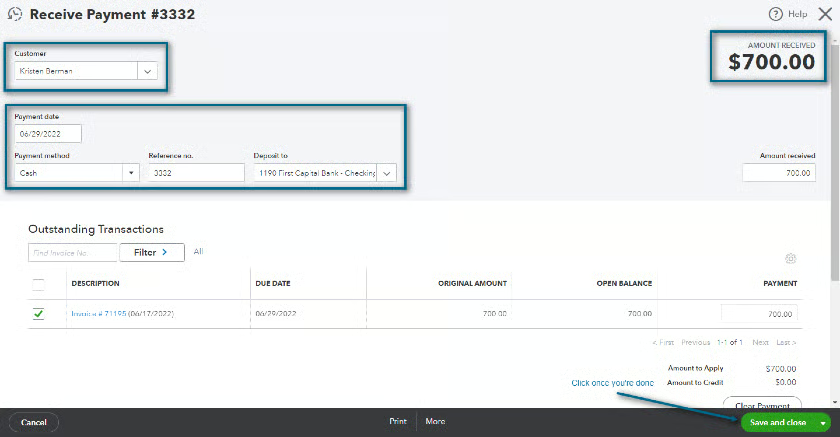

Click Save for later at the top of the reconciliation screen to safely exit without losing progress. After recording the $700 payment from Kristen Berman in the check register, return to the reconciliation screen and tick the payment to clear it.

Fill in the details, and don’t forget to select the appropriate bank account where the customer deposited it. In our example, Kristen deposited it into First Capital Bank, so we should select First Capital Bank – Checking Account. Hit the green Save and close button once you’re done.

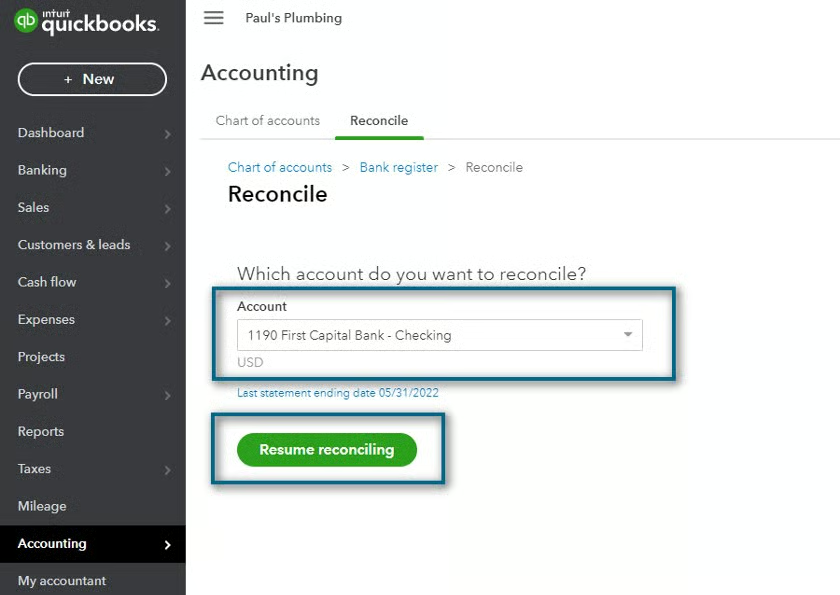

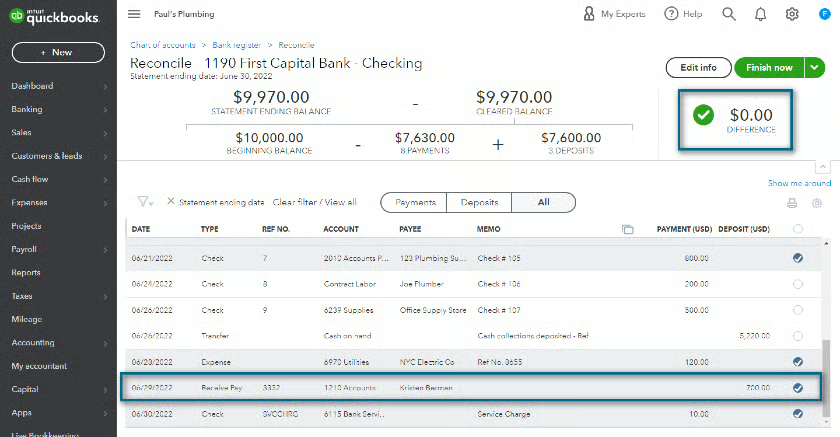

Step 4: Complete reconciliation.

Navigate to Accounting in the left menu bar and click Reconcile to open the reconciliation screen. Select the account you want to reconcile, then click Resume reconciling.

On the reconciliation screen, locate the adjustment you made and tick it. The difference should now be $0, and the cleared balance should match the statement ending balance.

Click the green Finish now button to complete the bank reconciliation. This notification will appear: “You reconciled this account.” Click Done, and you’ll arrive back at the bank register.

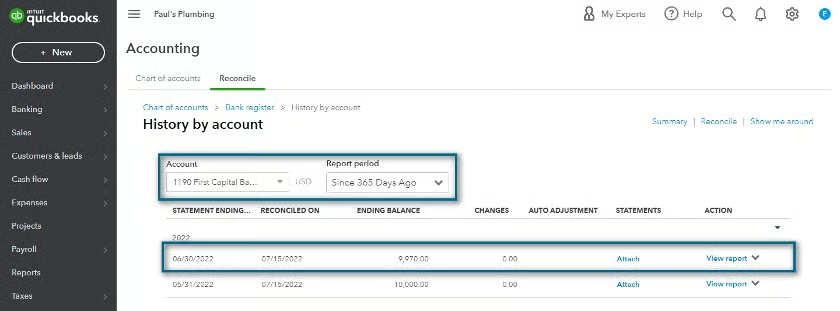

Step 5 (Optional): Generate a bank reconciliation report.

Navigate to Reports in the left side menu. Use the search bar and search for Reconciliation Reports.

QuickBooks Online will bring you to the History by account screen. Ensure you choose the checking account you want to see and set the report period. Click View Report to generate the bank reconciliation statement.

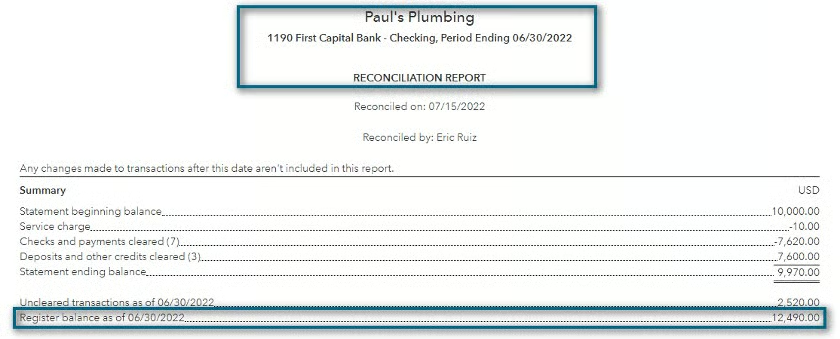

QuickBooks Online reconciled the bank statement items to arrive at the bank statement ending balance. If you add all uncleared transactions to the statement ending balance, you’ll arrive at the register balance or the adjusted cash balance.

The importance of reconciling a bank statement

- Ensures the availability of cash: Timely bank reconciliations help your business know the amount of cash in the bank. It helps reduce the occurrence of bounced checks and failed payments due to insufficient funds.

- Catches fraud and manipulations: If one of your employees withdraws money from your bank account or a supplier forges a check you issued, you will certainly see it in the bank statement. In large businesses, accountants and internal auditors sometimes use the proof of cash, or the two-date bank reconciliation. It not only reconciles the ending balances of the checking account but also the current period receipts and disbursements.

- Detects errors and fees: If you recorded checks in the books by mistake, you can correct them by looking at the amount in the bank statement. More so, you can look at the actual check that comes with the bank statement. The bank statement will also reveal the fees and penalties that were charged to your account.

- Explains differences in bank statements and check registers: A bank reconciliation shows items that 1) should be recorded in the check register; and 2) are yet to be recorded by the bank. By considering these reconciling items, you can verify that the check register and bank account have the same balance.

Common bank reconciliation errors and how to fix them

“To err is human, to forgive, divine,” wrote Alexander Pope. Nowhere is that truer than in accounting. Few things invite mistakes faster than the most tedious task in accounting: bank reconciliations.

Finishing one flawlessly on the first try belongs less to the world of spreadsheets and more to the realm of miracles. If you finish one bank reconciliation without finding errors, mismatches, and irregularities, treat yourself to some ice cream because such is a rare occurrence.

Here are some of the common bank reconciliation errors that sneak in when you’re tired, distracted, or just trying to survive through another cup of coffee.

| Error | How it happened | How to fix it |

|---|---|---|

| Missing or unrecorded items | Bank-originated activity, such as fees, interest, wire charges, and certain ACH adjustments, often appear on statements but are not booked internally. This creates discrepancies between the ledger and bank balances. | Perform regular, frequent reconciliations and automated bank-data imports to surface these items quickly, allowing entries to be posted on time. |

| Duplicate transactions | Duplicate payments or receipts can result from manual entry, an automatic bank feed, re-imports, or processing the same transaction twice. This overstates expenses or cash activity. | Implement controls such as duplicate-detection rules, restricted posting permissions, and a reconciliation checklist to reduce duplicates before they hit the general ledger. |

| Data-entry errors | Transposed digits, incorrect dates, and misclassified accounts commonly derail matching, leading to unexplained differences. | Use standardized descriptions or do a second-person review for manual entries or targeted searches for transposition patterns to help pinpoint and correct these errors. |

| Timing differences | Outstanding checks and deposits in transit are normal timing gaps that cause temporary mismatches between internal records and bank statements until they clear. | Maintain a tracked list of uncleared items and expected settlement dates to prevent unnecessary investigations and clarify true adjusted cash. |

| Unmatched or mismatched transactions | Amount or date discrepancies between ledger entries and the bank statement — often due to typos, partial deposits, or merchant fees — result in items that will not auto-match. | Cross-check against invoices and receipts and use software that flags mismatches, speeds up resolution, and keeps reconciliations accurate. |

| Bank fees and interest not recorded | Service charges, card fees, and interest credits that are not posted in the books distort reconciliation and misstate cash and expense or income accounts. | Implement a month-end procedure to sweep all bank charges and interest into the ledger to close gaps and reduce recurring reconciling items. |

| Unauthorized or fraudulent activity: | Unrecognized vendors, unusual payees, or unexplained withdrawals may appear as anomalies during reconciliation and signal fraud risk. | Watch for new or unrelated vendors, mismatched amounts, and unexplained dates — combined with invoice review — to help surface and stop fraud early. |

| Opening and closing balance mismatches | Differences between statement balances and prior-period reconciled balances can indicate missed adjustments, incorrect openings, or unposted items. | Verify balances and ensure prior-period adjustments are recorded to prevent rolling reconciliation errors. |

Frequently asked questions (FAQs)

What is a bank reconciliation?

A bank reconciliation matches transactions and balances in your internal books to those on your bank statement. It explains differences such as outstanding checks, deposits in transit, fees, or errors. The process results in an adjusted balance that agrees between the books and the bank after timing items are recorded and necessary journal entries are posted.

How often should bank reconciliation be done?

Most businesses reconcile monthly, in line with bank statement cycles. High-volume operations may reconcile weekly or even daily to catch issues promptly and speed the close process. Frequent reconciliations reduce investigation time and help ensure opening balances are accurate for the next period.

What documents are needed?

At a minimum, you need the bank statement or bank feed for the period, plus internal ledgers or accounting system records of cash receipts and disbursements. Supporting documents, such as check registers, deposit slips, and fee schedules, can also help identify timing differences and unrecorded charges.

Who performs bank reconciliation?

Bank reconciliations are typically carried out by an accounting staff member, such as a bank reconciliation specialist or reconciliations officer. A senior accountant or manager then reviews the work to maintain segregation of duties and ensure proper internal control. To reduce the risk of errors or fraud, the person who records cash receipts or disbursements in the ledger should not be the same person who performs the reconciliation. A separate reviewer should approve the completed reconciliation.