Depreciation in accounting and bookkeeping is the process of allocating the cost of a fixed asset over the useful life of the asset. The cost of the asset should be deducted over the same period that the asset is used to generate income instead of deducting a large expense when it’s purchased. This provides a better match of expenses and the income those expenses generate. Depreciation expense is listed on your income statement and is subtracted from revenue when calculating profit.

Depreciation Expense, Accumulated Depreciation & Net Fixed Assets

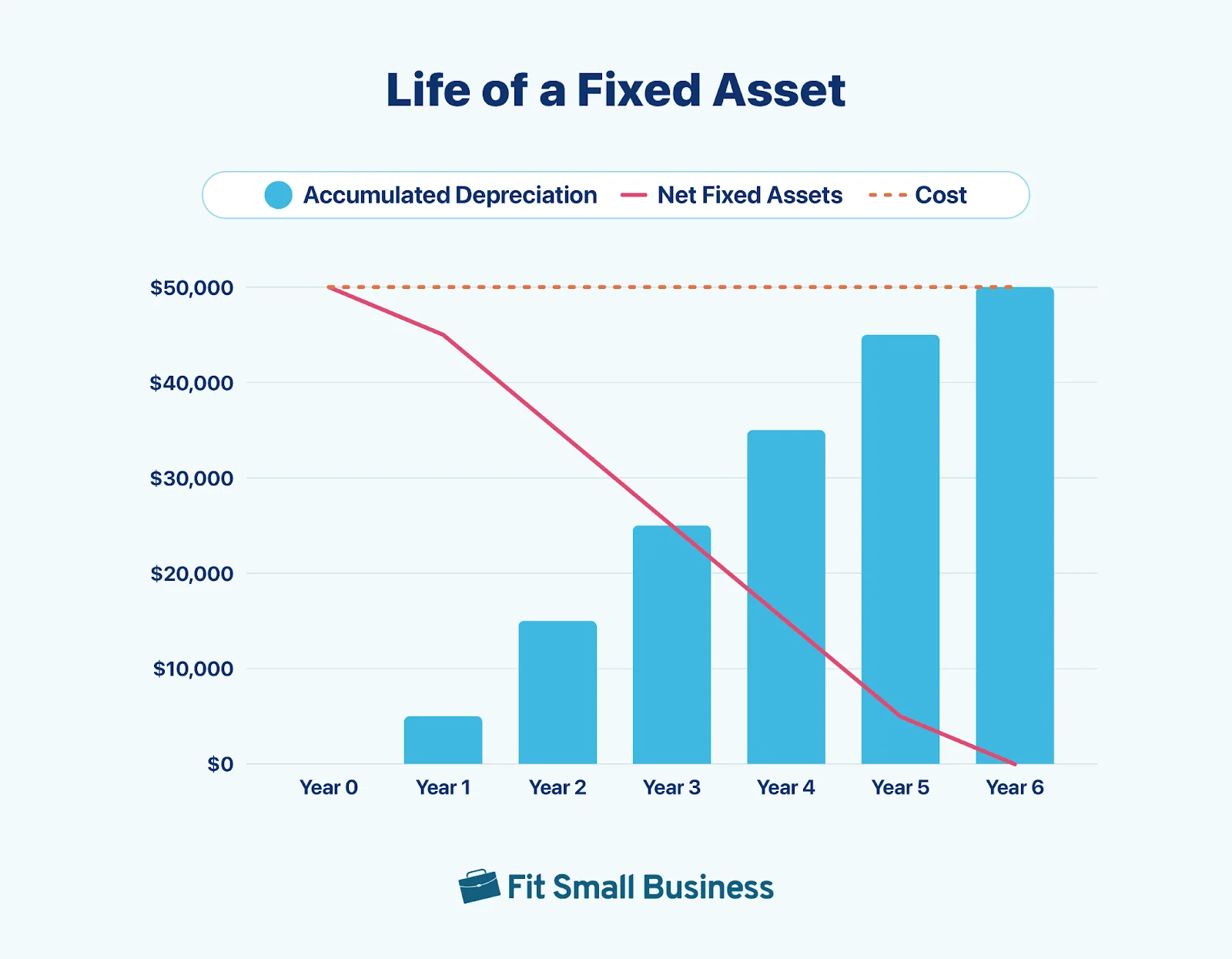

Depreciation expense is the amount that a company’s fixed assets are depreciated for a single period, and it’s shown on the income statement. Accumulated depreciation is the total amount of depreciation that has been deducted over the life of an asset. It reduces the value of net fixed assets on the balance sheet.

The basic journal entry for depreciation is to debit the Depreciation Expense account and credit the Accumulated Depreciation account. Over time, the accumulated depreciation balance will continue to increase year after year as more depreciation is added to it until it equals the original cost of the asset. In contrast, depreciation expense is reset to zero at the end of each year.

Say you have $10,000 of depreciation expense in the current month. The journal entry would be:

| Debit | Credit | |

|---|---|---|

| Depreciation Expense | 10,000 | |

| Accumulated Depreciation | 10,000 |

Net Fixed Assets

Net fixed assets equals the cost of fixed assets minus accumulated depreciation. So, as accumulated depreciation increases over time, the value of net fixed assets decreases over time.

The chart below represents the cost, accumulated depreciation, and depreciation expense of a $50,000 fixed asset depreciated $10,000 per year for five years. The first and last years deduct only $5,000 as it’s assumed the asset was placed in service mid-year.

Types of Depreciation for Book Purposes (GAAP) With Examples

The four main methods of depreciation for the generally accepted accounting principles (GAAP) are straight line, double declining balance, units of production, and sum of the years’ digits.

Straight Line

Straight line depreciation is the simplest method of calculating depreciation expense. In it, the expense amount is the same every year over the useful life of the asset.

To calculate your deduction, first determine the cost basis, salvage value, and estimated useful life of your property. Subtract the salvage value, if any, from the cost basis. The balance is the total depreciation you can take over the useful life of the property.

- Cost: The total cost of the item, including taxes, shipping, and more

- Salvage value: How much you’ll sell the item for (if anything) once you’re done using it

- Estimated useful life: The estimated amount of time that you’ll use the item, typically calculated by years; for additional insights, check out our article on how to determine the useful life of an asset

Example: You purchased a brand new computer for $1,200, with an estimated salvage value of $200. The estimated useful life of the computer is five years. According to the formula:

($1,200 − $200) ÷ 5 = $200 per year

Double Declining Balance

The double declining balance (DDB) depreciation method is a form of accelerated depreciation

Example: You own a screen printing business and purchase a machine for $1,200 to produce custom-printed merchandise. The machine is expected to last five years and has a salvage value of $200.

(1 ÷ 5) = 20%

The straight line depreciation rate is 20%, but you want double that rate, so multiply it by two.

Depreciation rate: 20% × 2 = 40%

Once you have your depreciation rate, multiply it by the adjusted book value of the asset at the beginning of the period. The beginning adjusted book value is the cost of the asset less accumulated depreciation (A/D) from prior years.

| Beginning Book Value | Depreciation Expense(BBV × 40%) | |

|---|---|---|

| Year 1 | $1,200.00 | $480.00 |

| Year 2 | $720.00 | $288.00 |

| Year 3 | $432.00 | $172.80 |

| Year 4 | $259.20 | $59.20 |

| Year 5 | $200.00 | $0.00 |

| Total | $1,000.00 |

Units of Production

Although you can’t use the units of production depreciation method to calculate your tax return, it’s one of the four methods of depreciation allowed for GAAP. It allows businesses to allocate the cost of an asset based on its output, such as the number of hours it’s used, the number of units it produces, or another relevant measure of production.

It is beneficial to manufacturers whose use of machinery varies from year to year because it matches the cost of the machinery to the revenue that it creates and better reflects its wear and tear. It can be calculated in two steps:

- Determine the units of production rate by subtracting the salvage value from the cost basis of the asset and dividing that by the estimated number of units that you expect it to produce over its useful life.

- Multiply that amount by the actual units produced, and that amount will be your depreciation expense.

- Estimated units: You’ll need to estimate the number of units the machine will be able to produce over its entire life. If you forecast too few, you’ll assign too high of a cost to units produced early in a machine’s life and no cost to units produced at the end of the life.

- Units produced: This is the number of units that are produced during the year for which depreciation is being calculated.

Example: You purchase a computer for your manufacturing business at a total cost of $1,200. It has a salvage value of $200, and it’s estimated to produce 5,000 units over its estimated useful life. There were 1,250 actual units produced during the first year, which will be multiplied by the depreciation rate per unit.

Depreciation rate per unit: ($1,200 – $200) ÷ 5,000 = 0.20

Depreciation expense: 1,250 × 0.20 = $250 for Year 1

Sum of the Years’ Digits

Sum of the years’ digits is also an accelerated depreciation method, but it doesn’t depreciate an asset quite as quickly as DDB. It takes an asset’s expected life and adds together the digits for each year. Each digit is then divided by this sum to determine the percentage that the asset should be depreciated each year. This method results in greater depreciation in the earlier years of an asset’s useful life and less in the later years.

This depreciation method is often used for assets that could quickly become obsolete. However, it’s considered the most difficult depreciation method to calculate.

- Remaining life: The estimated amount of time remaining for the asset, typically calculated by years.

- Sum of the years’ digits: Add the digits for each year of an asset’s expected life. For example, if an asset was expected to last five years, the sum of the years’ digits would be determined by adding 5 + 4 + 3 + 2 + 1 for a total of 15.

Example: You purchase a computer for $1,200, and you estimate that its estimated useful life is five years. First, you’ll determine the sum of the years’ digits by adding up the digits in the five years of the computer’s useful life. In this case, it would be 1+ 2 + 3 + 4 + 5, or 15. Divide the remaining life of the asset by the sum of the years’ digits and multiply that by the difference between the cost of the asset and its salvage value.

Cost less salvage value: $1,200 – $200 = $1,000

Year 1 depreciation rate: 5/15

Year 1 depreciation expense: $1,000 × 5/15 = $333 per year

The table below shows the depreciation expense for all five years of the asset’s life.

| Cost Less Salvage Value | Depreciation Rate | Depreciation Expense | |

|---|---|---|---|

| Year 1 | $1,000 | 5/15 | $333 |

| Year 2 | $1,000 | 4/15 | $267 |

| Year 3 | $1,000 | 3/15 | $200 |

| Year 4 | $1,000 | 2/15 | $133 |

| Year 5 | $1,000 | 1/15 | $67 |

| Total | $1,000 |

Types of Depreciation for Tax Purposes

Unlike book depreciation—which matches expenses with revenues—the purpose of tax depreciation is to provide an incentive for companies to purchase fixed assets by providing a large tax deduction early in the asset’s life. There are different types of depreciation used for tax purposes, and the most popular is the MACRS depreciation method. Using Section 179, expense and bonus depreciation are two other methods that can be employed.

MACRS Depreciation

The primary depreciation method used for tax purposes is MACRS. The IRS publishes tables that you can use to calculate your annual tax depreciation, and the underlying depreciation method used to calculate the tables differs based on the life of the assets.

Section 179 Expense

The Section 179 expense allows business owners to deduct up to $1,220,000 of the cost of qualifying new or used property and equipment purchases automatically for the 2024 tax year. One of the advantages of this deduction is that you’ll immediately receive tax savings from the purchase of an asset rather than gradually saving taxes through depreciation in future years.

Section 179 is elected by completing Part 1 of IRS Form 4562. This form summarizes your depreciation expense and is included with your business return.

Bonus Depreciation

Bonus depreciation allows a business to write off 60% of the cost of qualifying property for 2024; the remaining 40% of the cost must be depreciated. It is often confused with the Section 179 deduction because both allow a company to write off at least a portion of the cost of qualified property immediately.

While these two depreciation methods serve a similar purpose, they aren’t the same. For example, a business can’t claim Section 179 unless it has a taxable profit, whereas bonus depreciation isn’t limited by the company’s taxable income. Bonus depreciation can be a valuable tax break for businesses that purchase equipment, furniture, and other fixed assets.

Key Differences Between Book & Tax Depreciation

Book depreciation refers to the depreciation expense shown on the company’s income statement, while tax depreciation refers to the depreciation expense as listed on a company’s tax return. Here’s a summary of key differences between how the two are calculated:

- Tax depreciation never uses a salvage value.

- The useful life of assets for tax depreciation is set by law.

- Units of production and the sum of the years’ digits aren’t allowed for tax depreciation.

- For tax purposes, most tools and equipment are considered purchased in the middle of the year, regardless of when they’re purchased. Real property is considered to be purchased in the middle of the month in which it’s actually purchased.

Frequently Asked Questions (FAQs)

Is depreciation good or bad?

In accounting, depreciation is neither good nor bad. It’s just an allocation of the cost of fixed assets over their useful life. It decreases net income, which some financial statement users might consider bad.

Is it worth claiming depreciation?

Absolutely. You should always claim your allowable depreciation for tax purposes. There is no benefit to not claiming the tax deduction. When you sell an asset, the gain or loss is calculated on the asset cost less allowable depreciation—regardless of whether you actually deducted the allowable depreciation.

Does depreciation measure wear and tear on a machine?

No—despite many opinions shared on the internet—depreciation in accounting is not a measure of wear and tear. It is simply an allocation of cost over the useful life of the asset. While it might be somewhat correlated with wear and tear, wear and tear is not a factor in determining depreciation expense.

The term “depreciation” can also refer to the decline in value of an asset, which is related to wear and tear. However, this is not the meaning of depreciation in accounting nor what the Depreciation Expense on the income statement measures.

Bottom Line

Depreciation is the allocation of purchase costs over an asset’s useful life. It is an important part of accounting and helps match the expense of the asset with the revenue generated by the asset.