Designed by well-known criminologist Donald R. Cressey, the fraud triangle explains the reasons behind fraud and is a guide for small business owners and managers to assess the areas where fraud might exist. In the accounting process, we look at fraud as a causative factor for material misstatements in accounting records and financial statements. We also look into how we can prevent fraud.

1. Pressure (or incentive): the what

Pressure is the financial or emotional motive to commit fraud. And with the right incentive or situation that creates a personal demand for more money, some employees may be tempted to commit fraud.

Motivations that create pressure to commit fraud include:

- Survival needs, e.g., sustaining a life-saving medicine or keeping up with inflation

- Unexpected circumstances, e.g., paying for a sudden medical bill or a life partner losing their job

- Personal incentives, e.g., supporting a gambling addiction or wanting to keep up with peers’ lifestyles

- Disgruntlement or resentment, e.g., feeling constantly pressured to exceed goals to gain bonuses or being overlooked for a promotion

2. Opportunity: the how

Opportunity is the ability to commit fraud without getting caught or the circumstance that allows fraud to occur. In the fraud triangle in accounting, it is the only condition you, as a business owner or manager, have complete control over.

Common opportunities that enable fraud include:

- Nonexistent or weak small business internal controls, e.g., employees can override internal controls or take advantage of its weaknesses

- Lack of owner participation, e.g., the owner does not actively participate in daily operations, such as approving large expenses and signing checks

- Lack of physical controls or supervision, e.g., employees have access to the inventory storages, allowing them to steal goods, especially if there are no security personnel or security cameras in place

3. Rationalization (or attitude): the why

Rationalization is the personal justification of dishonest actions. Even when employees feel pressured and have the opportunity to commit fraud, most will not unless they can justify their actions.

Common justifications used to rationalize fraud include:

- “Everyone does it,” or the “tone at the top,” e.g., the owner bragging about hiding income from the IRS may affect employees’ behavior

- “No one would know or see,” e.g., someone handling incompatible duties (like recording payments in the accounting records and accepting cash from customers)

- “The company deserves it,” e.g., someone who has a below-market salary or is passed on for a promotion rationalizing that the crime is a way of getting back at the employer

Sample scenarios using the fraud triangle

Fraud can happen at any level of the business. I prepared two examples.

1. At the employee level

- Pressure (the what): Consider an employee struggling to keep food on the table due to debt — there’s an incentive to steal.

- Opportunity (the how): Say that the same individual lacks supervision and knows there are weak accounting controls. They have access to checks, so they steal them.

- Rationalization (the why): Imagine the employee thinking, “No one’s ever checked, so nobody will find out,” or “I deserve this money for all my hard work anyway.”

2. At the executive level

- Pressure (the what): Picture a greedy executive wanting more money to sustain their lavish lifestyle. However, the executive’s debt is piling up, and their income can no longer sustain it.

- Opportunity (the how): Say that person has the power to undo internal controls, hide spending in financial statements, and falsify documents.

- Rationalization (the why): Imagine them thinking, “No one will dare challenge me given my superiority,” or “Nobody will ask questions because I always deliver beyond what’s expected.”

Fraud at the executive level is harder to detect and uncover. First, executives have the authority to manipulate financial processes and override internal controls without immediate scrutiny. Second, lower-level employees often hesitate to report suspicious activity due to fear of retaliation, job loss, or direct threats from those in power. This combination of influence and fear creates an environment where fraud can persist undetected for extended periods.

Kinds of business fraud

There are two types of business fraud applicable to every business: fraudulent financial reporting and misappropriation of assets. These can exist regardless of the business size and anywhere in the bookkeeping process.

1. Fraudulent financial reporting

Also known as financial statement fraud, this involves the intentional manipulation of financial statement information through misstatements and omissions of information.

Click through the tabs for some of the precursors of fraudulent financial reporting.

Pressure

- Negative economic, industry, and operating-related conditions affecting business performance, stability, and profitability:

- High degree of competition and market saturation

- Rapid changes in technology and industry practices

- Increase in interest rates, inflation rates, and commodity prices

- Decline in consumer demands due to high prices

- Significant operating losses that might lead to bankruptcy

- Recurring negative cash flows from operations

- Inability to generate enough cash flows from operations due to poor credit collection

- New legislation or tax laws

- Excessive pressure from owners or top management to meet performance goals and objectives:

- Overly optimistic profit and growth estimates

- Owner’s extreme reliance on financial forecasts made by external investment and financial analysts without considering the business’s operating capabilities

- Achieving required financial metrics and solvency levels, such as the 1.5:1 current ratio, due to loan agreements and debt covenants

- Perceived effects of poor financial performance in relation to obtaining contracts from clients like government contract bidding requirements

- Existence of significant financial interests threatened by poor business performance:

- Stock options, partnership admissions, bonuses, performance raises, promotions, and fringe benefits that are contingent on the happening of business goals, such as stock price, level of sales, profit margin, and ROI

- Debts owed to business partners

Opportunity

- Inadequate or nonexistent internal control system:

- Absence of accounting controls to prevent, detect, and correct misstatements in the accounting system

- Lack of proper separation of duties

- Ineffective accounting systems, such as using unprotected spreadsheets that can be easily altered or deleted

- Use of manual accounting systems, even if similar businesses in the same industry have shifted to accounting software as a minimum standard

- Lack of owner participation:

- Passive participation of the owner in major business transactions, such as acquiring fixed assets or selling real property

- Lack of owner oversight in minor business transactions like signing checks, reviewing expenses, or checking the quality of products

- Extreme reliance of owner on subordinates like managers, vice presidents, and supervisors

- Unclear leadership and organizational structure:

- Overlapping job responsibilities due to inadequate workforce

- High employee turnover due to poor or negative HR management

- Absence of approval workflows

Rationalization

- Disregard of HR:

- Hesitation of the owner to hire more people

- Outsourcing job positions that should not be outsourced

- Unethical behavior and misconduct:

- Hiring employees with a known history of business fraud and violation of business laws

- Excessive pressure from management to constantly achieve profit goals

- Excessive participation and involvement of nonaccounting personnel in determining accounting policies

- Overestimation or underestimation of significant accounting estimates to influence income and tax obligations

- Participation of the owner in unethical behaviors and misconduct

- Charging personal expenses to business accounts

2. Misappropriation of assets

Asset misappropriation involves theft and unauthorized use of company assets. Lower-level employees can do it in small or immaterial amounts, while top management can misappropriate assets in large amounts by concealing them.

Click through the tabs for examples of asset misappropriation.

Pressure

- Personal financial obligations of management and employees creating pressures to steal cash or other assets:

- Unpaid mortgages that may lead to home foreclosure

- Excessive credit card debts

- Poor money management and impulse expenses

- Extravagant living or living beyond means, leading to excessive loans

- Negative relationship between owner and employees:

- Firing employees subjectively

- Decrease in compensation levels and benefits or indifferent benefits and rewards after being promoted to a higher position

- Inconsistent promotions and rewards without an objective basis

- Favoritism

- Authoritarian owner or manager

- Unreasonable workloads that force employees to work overtime without pay

- Lack of reward systems to encourage employees to exceed requirements

- Performance reviews that are geared toward employee mistakes and flaws

- Absence of career advancement opportunities and lack of employer support with regard to pursuing continuing education and professional development

- Very stringent job promotion guidelines and qualifications

Opportunity

- Inadequate or nonexistent controls over custody and access to assets:

- Inadequate separation of duties

- Lack of management or owner intervention in minor frauds like using office printers for personal printouts, stealing office supplies, and bringing home office equipment like keyboards or monitors without approval

- Liberal or no-questions-asked approval on expense reimbursements

- Absence of physical controls like security cameras, fencing, biometrics scanning, and other access restrictions to business premises, and more

- Absence of expense and mileage expense policies

- Abuse of petty cash fund

- Lack of timely reconciliations of accounts like bank reconciliations

- Lack of documentation of transactions involving asset purchase, usage, and disposal

- Lack of independent and unannounced checks of employee work to assess consistency

- Lack of job rotation and mandatory vacations for key management officials

- Inadequate controls over electronic and automated systems:

- Absence of passwords in business computers and workstations

- Use of single passwords for all electronic banking apps

- Easily accessible passwords like writing login credentials in sticky notes and pasting them beside the computer monitor or keeping passwords in notepads

- Use of single accounts rather than separate user accounts

Rationalization

- Lack of monitoring:

- Absence of monitoring procedures to ensure proper documentation and accounting of asset-related transactions

- Announced performance monitoring or audits causing employees to work hard only during the monitoring period

- Business owner tolerance:

- Owner or manager’s tolerance of petty theft, such as stealing loose coins, taking office supplies for personal use, or abusing office pantry supplies by bringing them home

- Significant lifestyle changes like an employee earning $50,000 a year was able to buy luxurious properties

- Owner’s disregard for establishing a good internal control system

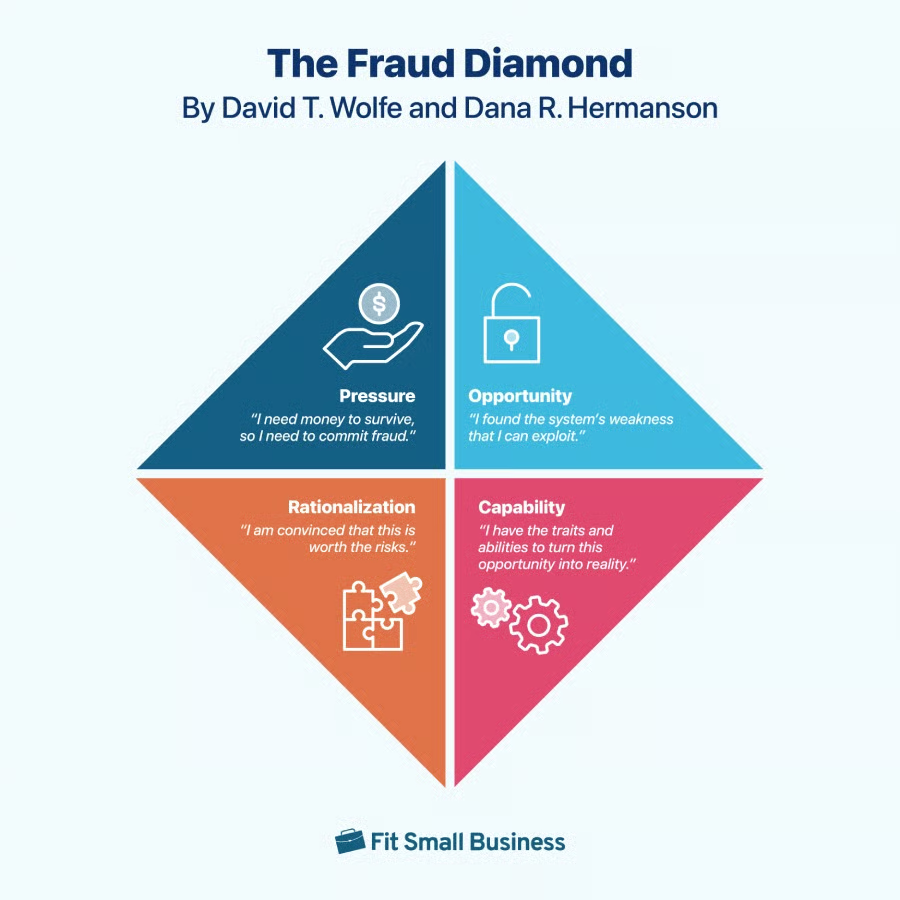

The new fraud triangle theory: The fraud diamond

The fraud diamond is a newer theory by David T. Wolfe and Dana R. Hermanson that incorporates capability as one of the key conditions to commit fraud, emphasizing the fraudster’s personal characteristics. While pressure, opportunity, and rationalization exist, the fraudster should also possess certain traits and abilities.

- Traits include greed, dishonesty, persuasion, and excessive pride.

- Abilities include knowledge of controls and the company’s vulnerabilities.

So capability, in this case, means that the fraudster would be intelligent and creative enough not only to recognize an opportunity to execute a fraudulent scheme but also to manipulate the system, deal with the stress of the crime, and stay undetected.

Six factors constitute capability, per Wolfe and Hermanson.

- Position: The person holds a role or responsibilities within the company that enables them to create an opportunity for fraud, such as the ability to control a deal’s timing.

- Intelligence: The person is smart enough to understand the company’s weaknesses and creative enough to use their position or access to their advantage.

- Ego: The person has a big ego and is very confident; common personality types include self-centered and narcissistic.

- Coercion: The person can convince others to conceal or even participate in the fraud. They may threaten those who don’t comply or insist that colleagues look the other way.

- Deceit: The person can lie convincingly, consistently, and effectively. This is critical so that their fabrications remain undetected.

- Stress: The person manages their stress very well, as committing and concealing fraud is stressful.

Frequently asked questions (FAQs)

What is the fraud triangle in simple terms?

In simple terms, the fraud triangle states that employees commit fraud when three conditions co-exist: pressure, opportunity, and rationalization.

What is the new fraud triangle theory?

The fraud triangle theory is a model for identifying fraud risks. It states that three factors — pressure, opportunity, and rationalization — lead to fraud.

What are the four points of fraud?

The four points of fraud in the fraud diamond are pressure, opportunity, rationalization, and capability.

Bottom line

Establishing strong internal controls can mitigate fraud risks — but only to a certain level. Business owners and leaders should create a healthy working relationship with, as well as an environment for, employees to prevent them from resorting to fraudulent acts. Keeping workers happy and providing growth opportunities will help them align personal goals with business goals.