Form 941 is a quarterly tax form that tracks Federal Insurance Contributions Act (FICA) (Social Security and Medicare) payments made by employers throughout the year. Employer FICA tax payments (6.2% for Social Security and 1.45% for Medicare) are typically due monthly or semiweekly, and Form 941 is due quarterly.

Since filling out Form 941 can be time-consuming and confusing, let’s go through each section and cover what you need to do. Once complete, filing your tax return electronically is the easiest route, but if you prefer to mail it in, check out our mailing address by state table further down in the article.

Key Takeaways:

- Most employers need to file Form 941, except seasonal employers who only have to file for quarters in which they pay wages

- Make sure you prepare for filing this form by keeping accurate records and having them ready when you’re completing the form

- There is an updated form for 2024 which eliminated many lines, making for a smoother filing process

- 2024 Form 941 Updates

- 1. General Information & Form 941 Reporting Period

- 2. Form 941 Part 1, Lines 1 Through 15

- 3. Form 941 Part 2, Line 16

- 4. Form 941 Part 3, Lines 17 & 18

- 5. Form 941 Part 4

- 6. Form 941 Part 5

- Form 941 Basics: How, Who, When & Where

- Form 941 Late Filings

- Frequently Asked Questions About Form 941

- Bottom Line

2024 Form 941 Updates

There have been some changes to the form for 2024, so make sure you’re using the updated version. Here’s a breakdown of the updates:

- The Social Security wage base is now $168,600

- Lines 11a through 11g have been removed, and now line 11 requests information from Form 8974, if applicable

- Lines 13a through 13i have been removed, and now line 13 requests the sum of deposits for the present quarter

- Lines 19 through 28 have been removed

1. General Information & Form 941 Reporting Period

In the top section of the form, you will provide general information about your business, such as business name, tax ID, and mailing address. You will also indicate the quarter for which you are filing the return.

2. Form 941 Part 1, Lines 1 Through 15

- Line 1: Enter the total number of employees who received wages, tips, or other compensation in the quarterly pay period.

- Line 2: Enter the total wages, tips, and other compensation paid to employees.

- Line 3: Enter the total federal income tax withheld from employee wages, tips, and other compensation.

- Line 4: Check this box if there are no wages, tips, or other compensation subject to Social Security or Medicare taxes. If checked, jump to line 6.

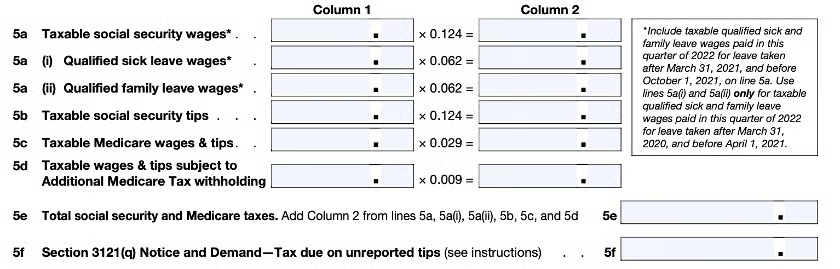

- Line 5a: Enter the total taxable Social Security wages in Column 1. Multiply that by 0.124 and enter the total in Column 2.

- Line 5b: Enter the total taxable Social Security tips in Column 1. Multiply that by 0.124 and enter the total in Column 2.

- Line 5c: Enter the total taxable Medicare wages and tips in Column 1. Multiply that by 0.029 and enter the total in Column 2.

- Line 5d: Enter the total taxable wages and tips subject to additional Medicare tax withholding in Column 1. Multiply that by 0.009 and enter the total in Column 2.

- Line 5e: Enter the sum of Column 2 in lines 5a through 5d.

- Line 5f: Enter tax due on unreported tips. You may have received a Section 3121(q) Notice and Demand from the IRS. If you did not receive this notice, leave this line blank.

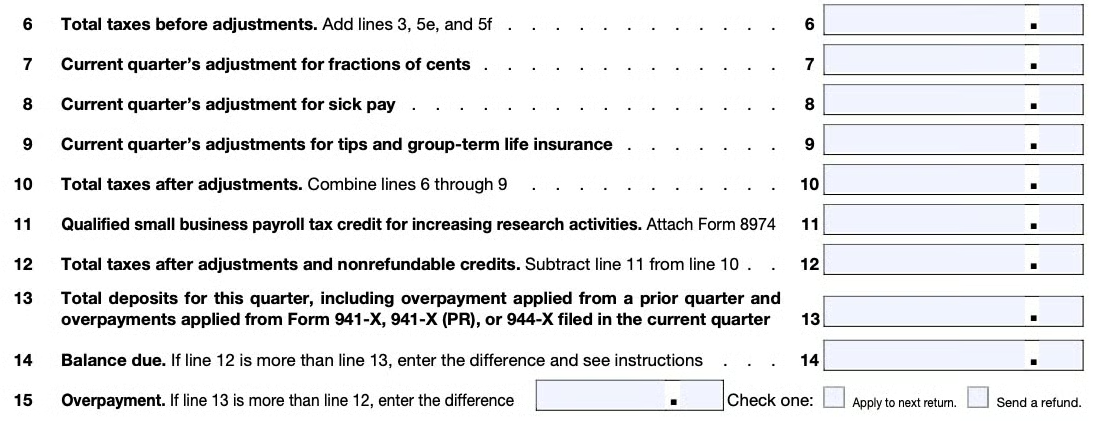

- Line 6: Enter the sum of lines 3, 5e, and 5f (if applicable).

- Line 7: Use this line to adjust fractions of cents from lines 5a through 5d. In those calculations, you may end up with fractions of cents. This can be either positive or negative, so use a negative sign (not parentheses) to indicate a decrease.

- Line 8: Calculate any paid sick leave and enter the total as a negative.

- Line 9: Enter a negative for any uncollected employee share of Social Security and Medicare taxes on tips and for the uncollected employee share of Social Security and Medicare taxes on group-term life insurance premiums paid for former employees. Leave this line blank if you don’t have either.

- Line 10: Enter the total from lines 6 through 9.

- Line 11: If this credit applies to you, enter the amount of credit from Form 8974 and attach the form. Leave this line blank if the credit does not apply to you.

- Line 12: Enter the total amount from subtracting line 11 from line 10.

- Line 13: Enter your total deposits, including overpayments.

- Line 14: If line 12 is more than line 13, enter the difference. Leave this line blank if line 12 is less than line 13.

- Line 15: If line 13 is more than line 12, enter the difference. Do not complete this line if you entered an amount on line 14.

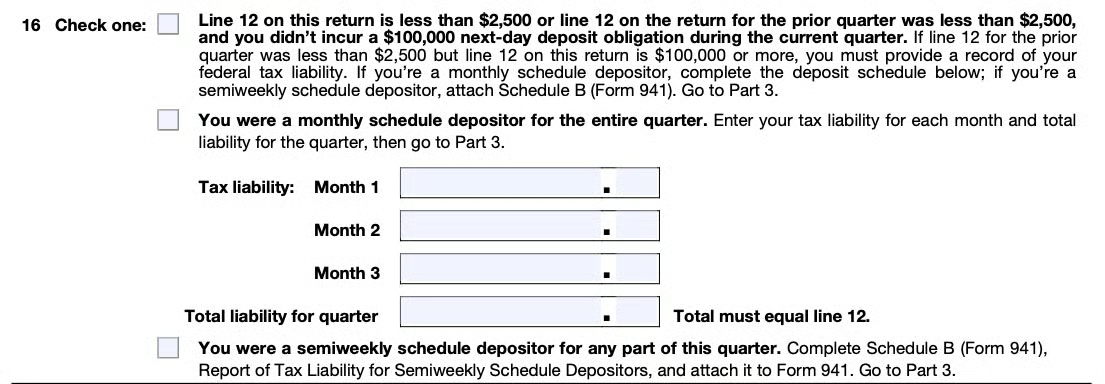

3. Form 941 Part 2, Line 16

In this section, you’ll only check one box.

- Check the first box:

- If line 12 above or on your previous quarterly return is less than $2,500 AND

- You did not incur a $100,000 next-deposit obligation during the quarter for which you are completing this form

- Check the second box:

- If you’re a monthly depositor

- Also, complete your tax liability for each month, ensuring the total amount matches line 12 above

- Check box three:

- If you’re a semiweekly depositor

- Also, complete Schedule B

4. Form 941 Part 3, Lines 17 & 18

- Line 17: If your business has closed or stopped paying wages during this quarter, check the box and enter the date you paid final wages. Leave this line blank if you’re still operating.

- Line 18: If you hire seasonal workers and don’t file a return every quarter, check this box.

5. Form 941 Part 4

According to the Form 941 instructions, you can give permission for the IRS to speak to someone about this form on your behalf. For example, you could put your CPA as a third-party designee. Be sure to include their complete name and telephone number. If you don’t want to designate anyone, you can select no.

6. Form 941 Part 5

In this section, you will sign and date Form 941 indicating that you agree with the information that has been included on this form and that, to your knowledge, it is accurate.

Form 941 Basics: How, Who, When & Where

As an employer, you are required to withhold taxes from your employees’ paychecks. Generally, these taxes include income taxes, Social Security, and Medicare taxes. The IRS requires that you report these taxes quarterly on Form 941. The employer’s share of FICA taxes is reported on Form 941 along with the employee’s share.

How to Prepare to File Form 941

To prepare to file your Form 941, you’ll need to gather information:

- Your pertinent business information, such as the legal business name, the business address, your employer identification number, and a trade name, if you use one

- The total number of employees you have for the reporting period

- The total wages and tips you paid for the reporting period

- The total taxable Social Security and Medicare wages for the reporting period

- The total amount of federal income taxes, Social Security, and Medicare tax withheld for the reporting period

- Employment tax deposits already made for the reporting period

You must use Form 941 to report the following:

- Wages you paid to your employees

- Tips your employees reported to you

- Federal income tax you withheld from employees’ paychecks

- Both employee and employer share of Social Security and Medicare taxes

Who Needs to File Form 941

Any business that pays wages to an employee has to file Form 941 each quarter. In most cases, you’ll be able to skip filing the form if you have seasonal employees and don’t pay wages during a quarter, or if you employ household or agricultural workers. Agricultural employees do need to file a different form, Form 943.

When To File Form 941

The due date to file Form 941 is the same for all employers, regardless of whether you are a monthly or semiweekly depositor of FICA taxes. Form 941 is due on the last day of the month that follows the end of the quarter. If the due date falls on a weekend or holiday, the due date is the next business day. You will submit Form 941 four times per year.

Below you will find a summary table of the due dates for Form 941:

| Quarter | Due Date |

|---|---|

| 1st Quarter(January 1–March 31) | April 30 |

| 2nd Quarter(April 1–June 30) | July 31 |

| 3rd Quarter(July 1–September 30) | October 31 |

| 4th Quarter(October 1–December 31) | January 31 |

Where To Mail Form 941

The best way to file tax forms is to use e-file. This service, offered by the IRS, allows you to file your tax returns electronically for free. Filing your tax return electronically will ensure that it is received on time.

If you prefer to mail in your tax forms instead, the state you live in will determine where your tax return is mailed. Refer to the table below for the address to mail your Form 941 return. Remember that information may change, and it’s always best to verify the mailing address before sending anything.

Form 941 Mailing Address by State

| State | Without a Payment | With a Payment |

|---|---|---|

| CT, DE, DC, GA, IL, IN, KY, ME, MD, MA, MI, NH, NJ, NY, NC, OH, PA, RI, SC, TN, VT, VA, WV, WI | Department of the TreasuryInternal Revenue ServiceKansas City, MO64999-0005 | Internal Revenue ServiceP.O. Box 806532Cincinnati, OH45280-6532 |

| AL, AK, AZ, AR, CA, CO, FL, HI, ID, IA, KS, LA, MN, MS, MO, MT, NE, NV, NM, ND, OK, OR, SD, TX, UT, WA, WY | Department of the TreasuryInternal Revenue ServiceOgden, UT84201-0005 | Internal Revenue ServiceP.O. Box 932100Louisville, KY40293-2100 |

| No legal residence or principal place of business in any state | Internal Revenue ServiceP.O. Box 409101Ogden, UT84409 | Internal Revenue ServiceP.O. Box 932100Louisville, KY40293-2100 |

| Special filing address for exempt organizations; governmental entities; and Indian tribal government entities, regardless of location | Department of the TreasuryInternal Revenue ServiceOgden, UT84201-0005 | Internal Revenue ServiceP.O. Box 932100Louisville, KY40293-2100 |

Form 941 Late Filings

Failure to file Form 941 and/or make your tax payments by the due date will result in penalties and interest. In general, penalties are typically a one-time payment, but interest will continue to accrue until your tax payment is made.

If you don’t file Form 941 on time, you could be subject to the following penalties and interest.

Each month that the form has not been filed, a failure-to-file (FTF) penalty of 5% of the unpaid tax due with that return will be assessed. The maximum penalty is generally 25% of the tax due.

If you have a balance due that should have been paid with your return (e.g., outstanding employer FICA payments that you need to make), there is a failure-to-pay (FTP) penalty of 0.5% per month of the amount of tax. This penalty is assessed for each month that the payment is late. The maximum amount of the penalty is also 25% of the tax due.

If both penalties apply in any month, the FTF penalty is reduced by the amount of the FTP penalty. The penalties won’t be charged if you have a reasonable cause for failing to file or pay. If you receive a penalty notice, you can provide a written explanation of why you believe reasonable cause exists.

In addition to any penalties, interest accrues from the due date of the tax on any unpaid balance. If income, Social Security, or Medicare taxes that must be withheld aren’t withheld or aren’t paid, you may be personally liable for the trust fund recovery penalty.

Keep in mind that even if you use a third-party payer, such as Gusto, that doesn’t relieve you of the responsibility to ensure tax returns are filed and all taxes are paid or deposited correctly and on time. However, most payroll services will reimburse you for any interest and penalties that you may incur if they are indeed at fault for filing and paying your taxes late.

Frequently Asked Questions About Form 941

Can I file Form 941 electronically?

Yes, and it’s recommended. You can file electronically through the IRS e-file system. This gives you faster processing times, immediate confirmation of receipt, and less worry if you’re close to the deadline.

What should I do if I find an error in a previously filed Form 941?

If you find an error, file Form 941-X. This form is used to make corrections to previously filed Form 941s. It’s crucial that you follow the instructions carefully to ensure corrections are processed accurately.

How do seasonal businesses handle Form 941?

Seasonal businesses that do not pay wages during certain quarters of the year can avoid filing the form if they don’t pay any wages during a particular quarter. They must still file Form 941 for any quarter they pay any wages.

Bottom Line

As you can see, there is a lot that goes into reporting Social Security, Medicare, and federal income taxes for both you as an employer and your employees. By following these instructions to file and pay your payroll taxes you can avoid penalties and the headache of IRS notices.

If you’d rather not manually fill out Form 941, consider using a payroll software like Gusto. Gusto will automatically pay FICA taxes and complete all payroll form filings on your behalf, so you don’t have to worry about doing it yourself. Check them and 1 month payroll free. Offer will be applied to your Gusto invoice while all applicable terms and conditions are met or fulfilled.