A fixed asset roll forward report is a schedule that reconciles beginning and ending balances of fixed assets and accumulated depreciation over a period by capturing all movements. It presents the opening balances for asset cost, accumulated depreciation, and net book values, followed by period activity, such as acquisitions and retirements.

My template below shows the most basic and ready-to-use sample of a fixed asset roll forward report.

What a fixed asset roll forward report includes

A fixed asset roll forward details the annual activity in fixed assets and accumulated depreciation — including improvements and disposals — leading to the ending balance.

Here’s the basic structure of a roll forward of the fixed asset account:

| Opening balance of fixed assets | |

|---|---|

| + | Additions during the year at cost |

| − | Disposals during the year at cost |

| − | Current period depreciation |

| = | Ending balance of fixed assets |

When fixed assets are disposed of, the cost of the disposed asset, not the selling price, must be used because the rollforward report tracks asset balances, not sales proceeds. The selling price is only relevant in calculating any gain or loss on the sale, but it doesn’t affect the reconciliation of fixed asset cost and accumulated depreciation within the rollforward report.

Here’s the outline of the roll forward of the accumulated depreciation account:

| Opening accumulated depreciation | |

|---|---|

| + | Current period depreciation expense |

| − | Accumulated depreciation of disposed asset |

| = | Ending accumulated depreciation |

When disposing of a fixed asset, remove the accumulated depreciation related to that asset from the books and compute depreciation expense only up to the disposal date so that the net book value is accurate at the time of disposal. The same principle applies to additions of fixed assets. Also, depreciation should begin from the date the asset is placed in service to ensure the expense reflects the actual period of use within the reporting cycle.

I recommend reading the following resources to help you learn more about fixed asset accounting and depreciation.

- What Is Fixed Asset Accounting?

- Disposal of Fixed Assets

- Depreciation: How It Works

- What Is PP&E in Accounting?

- What Are Assets in Accounting?

Purposes of a fixed asset roll forward

A fixed asset roll forward serves many purposes in financial management, reporting, and analysis. Here are a few:

- Reconciliation and accuracy: Shows how opening balances move to closing balances by itemizing activity, ensuring PP&E and accumulated depreciation are reported correctly.

- Audit trail and support: Gives auditors a ready-made record to verify completeness, existence, and valuation of assets and depreciation. The movement analysis reduces auditor follow-up and rework, making the audit process smoother.

- Period balances: Presents beginning balances, period activity, and ending balances that reconcile directly to the general ledger and financial statements.

- Tax readiness: Captures acquisitions and disposals required to prepare tax depreciation and maintain accurate asset schedules.

- Management decisions: Helps management plan capital spending, review asset utilization, and time replacements by showing trends in additions and retirements.

Common formats for roll forward reporting

A fixed asset roll forward schedule can be presented in different ways depending on the purpose, audience, and level of detail required. The approaches below highlight the most common formats used in practice.

| Format | What it is |

|---|---|

| By movement buckets | A bucketed movement schedule lays out columns for opening balance, additions, disposals, transfers, revaluations or impairments, depreciation (including special, extraordinary, and reversals), and closing balance for both cost and accumulated depreciation. This is the most audit-friendly format. |

| Expanded buckets by transaction type | Depreciation is further split between regular and special or bonus, while write-ups, write-downs, and revaluations are shown separately. This mirrors ERP transaction codes and makes one-to-one tie-outs straightforward. |

| By level of detail | A summarized roll forward shows totals by asset class or entity with only a few line items, often used monthly or when activity is low for management reporting. |

| Detailed asset-level roll forward | This lists line-by-line movements for each asset, typically used for quarter or annual close and audits. ERP systems often export these schedules into Excel for detailed review. |

Also read: ERP vs Accounting Software: Which Is Best for Your Business?

How to do a fixed asset roll forward report

A fixed asset roll forward is a valuable tool for ensuring accuracy, analyzing asset management, and supporting financial reporting. Use the template I supplied above to create your own fixed asset roll forward, and follow these steps.

Step 1: Gather all necessary reports.

When preparing to fill out the template, you’ll need to gather the following reports:

- Prior year ending balance sheet or trial balance

- Current year ending balance sheet or trial balance

- Current year income statement or trial balance

- Current year depreciation schedule

If possible, access your accounting software to gather other information that might be excluded from the reports above.

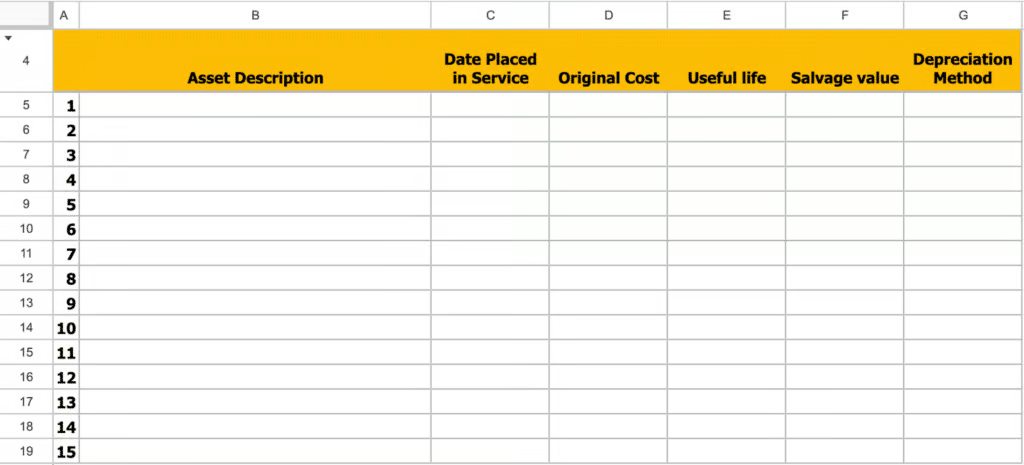

Step 2: Fill in basic fixed asset information.

To complete this section, reference your fixed asset register, purchase invoices, vendor contracts, and general ledger for cost details. Also, check your accounting policies or tax depreciation schedules for useful life, salvage value, and method.

Here’s how to fill out the fixed asset template, along with where to source the information:

- Asset Description: Enter the name of the asset, such as “Office Laptop” or “Delivery Truck.” You can find this in your fixed asset register or purchase invoices.

- Date Placed in Service: Record the date the asset was first used in operations. This date is typically on the purchase documents, vendor invoices, or fixed asset register. It is important because it determines when depreciation begins.

- Original Cost: Input the acquisition cost of the asset, including purchase price and any additional costs necessary to make it usable (e.g., shipping, installation). This is available from vendor invoices, purchase orders, or the general ledger.

- Useful Life: Enter the estimated number of years the asset is expected to be productive. This information is usually set by company accounting policy, management estimates, or tax guidelines.

- Salvage Value: Record the estimated residual value of the asset at the end of its useful life. This is often determined by management or based on industry practices.

- Depreciation Method: Specify the method applied to the asset, such as straight-line or double-declining balance. This comes from your accounting policy or depreciation schedules.

Related resources:

- How To Calculate Useful Life of an Asset for Tax & GAAP

- How To Make a Depreciation Worksheet in Excel + Free Template

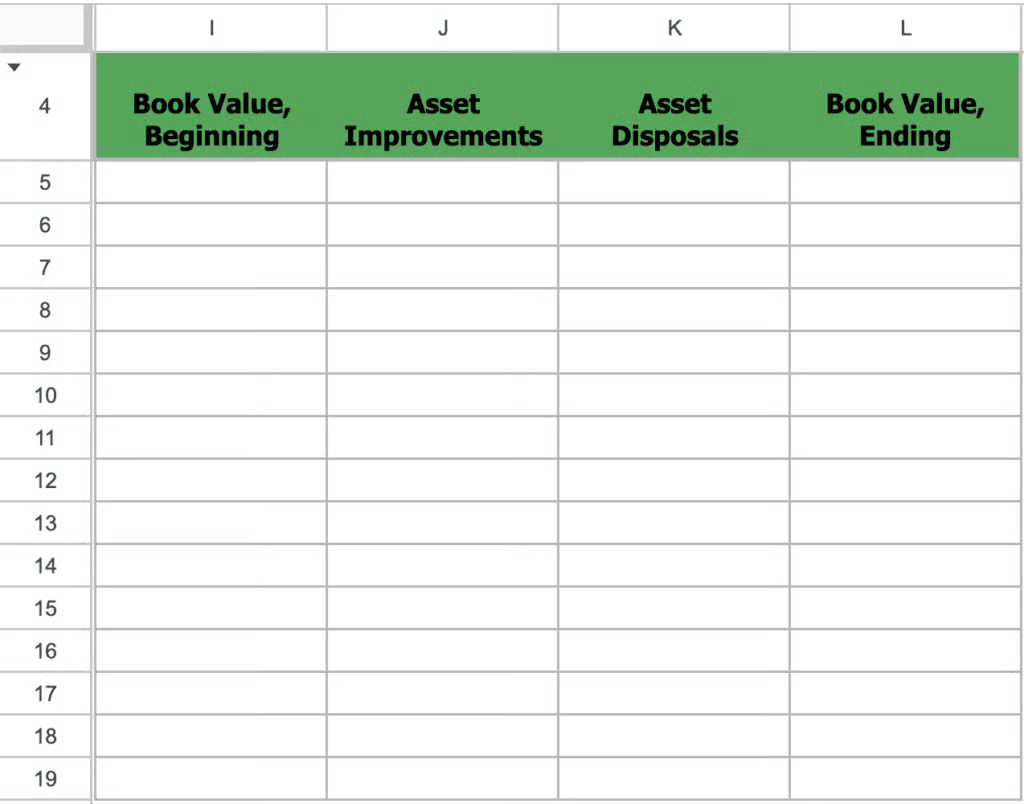

Step 3: Add asset improvements and disposals.

This section tracks changes in the book value of assets by pulling information from several key sources.

The beginning balance comes from the prior period’s ending balances, typically available in the fixed asset register or the general ledger.

Asset improvements are captured from capital expenditure records, vendor invoices, or project completion reports that document upgrades or major repairs, while asset disposals are identified from disposal forms, sale agreements, or accounting entries that record the retirement or sale of an asset.

Once those details are gathered, the ending balance is calculated by reconciling the beginning value with improvements and disposals. It should tie directly to both the fixed asset subledger and the balance sheet.

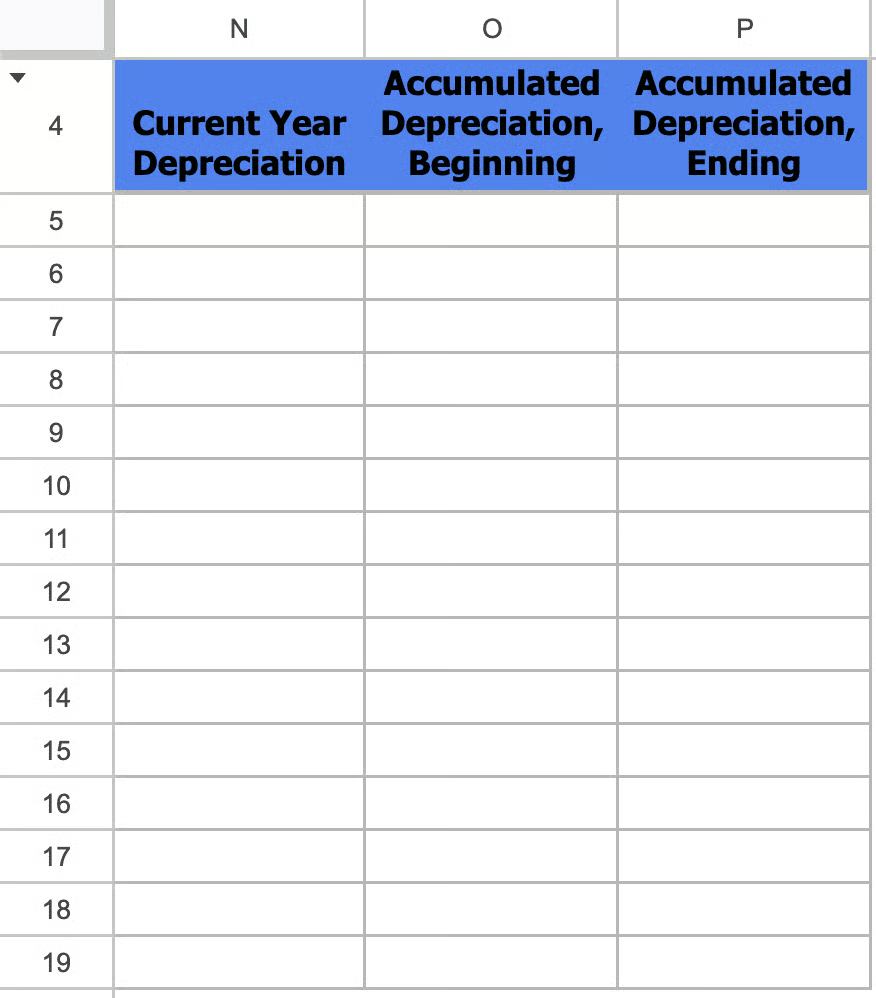

Step 4: Complete the depreciation information.

This part of the schedule tracks depreciation and shows how the accumulated depreciation balance changes during the period.

The current year depreciation represents the expense recorded for the period. It can be obtained directly from the depreciation expense report or fixed asset depreciation schedule generated by your accounting system.

Beginning accumulated depreciation is carried forward from the prior period’s ending balance, which you can find in the fixed asset register, the depreciation schedule, or the trial balance under accumulated depreciation.

Then, the ending accumulated depreciation is calculated by adding the beginning balance and the current year depreciation, less any accumulated depreciation removed for disposed assets.

This final balance should reconcile with the accumulated depreciation account in the general ledger and appear correctly in the balance sheet.

Common errors in creating a report and tips to resolve them

These issues often arise from timing, classification, capture, or calculation errors, causing the subledger not to tie to the general ledger or balance sheet.

- Inaccurate beginning balances: Prior-period ending balances don’t align with opening balances because adjustments weren’t carried forward. This is resolved by reconciling prior-year adjustments and confirming that opening balances match the general ledger.

- Missing or duplicate transactions: Additions, disposals, transfers, or revaluations are sometimes omitted or recorded twice. Cross-checking the roll forward against invoices, disposal records, and the fixed asset register usually clears up these differences.

- Timing and cutoff errors: Transactions fall in the wrong reporting period, leaving movements outside the roll forward window. Reviewing posting dates and adjusting cutoff entries brings them back into the right period.

- Misclassifications: Purchases are incorrectly expensed or posted to inventory, or construction in progress remains untransferred. Scan expense and inventory accounts and reclassify them to fixed assets to correct the totals and depreciation.

- Incorrect useful lives or methods: Depreciation is misstated when the wrong settings are applied. Verifying useful lives and methods by asset class and updating the system ensures expense is calculated correctly.

- Missing reversals on disposals: Accumulated depreciation isn’t removed when an asset is disposed of, overstating balances. Include the reversal with the disposal entry to clear the error.

- Partial disposals not handled: Only part of an asset is retired, but the related cost and depreciation aren’t removed proportionally. Applying proportional write-offs fixes the remaining residual balances.

- Spreadsheet or formula errors: Manual roll forwards can introduce broken links or wrong formulas. To reduce the risk of errors, test formulas and use version control.

Frequently asked questions (FAQs)

What does "roll forward" mean?

In accounting, “roll forward” is a term used to describe the process of updating the balances of accounts or financial statements from one period to the next. It involves taking the ending balance of a previous period and adjusting it for all relevant transactions that have occurred in the current period to arrive at a new ending balance. This concept is essential to ensure that financial records are accurate.

How often should a fixed asset roll forward be prepared?

The frequency of preparing a fixed asset roll forward depends on the company’s needs. However, it’s commonly prepared annually, quarterly, or monthly.

What are some common challenges in preparing a fixed asset roll forward?

The biggest challenge in preparing a fixed asset roll forward is commonly dealing with dispositions. It’s important to remove the original cost and life-to-date accumulated depreciation for disposed-of assets. The sales proceeds and gain or loss on the disposal of assets have no effect on the asset roll forward.

What is the journal entry for a fixed asset purchase?

To record a journal entry for a fixed asset purchase, you’ll debit the fixed asset account and then credit the cash account or the notes payable account if the purchase is financed. To learn more, read our guide on fixed asset accounting.