Approval for a business credit card is never guaranteed, as several reasons can contribute to a denial. The following are seven common reasons why your credit card application may be rejected, namely: credit score issues, verification issues from the issuing bank, business is new or unestablished, too many credit card applications, not enough income, no existing credit history, and mistakes in your credit record.

We discuss each and include actionable steps to improve your chances of getting approved for a credit card.

- 1. Credit Score Issues

- 2. Verification Issues With Your Business Details

- 3. Business Is New or Unestablished

- 4. Too Many Financing Applications

- 5. Not Enough Income

- 6. Insufficient Credit History

- 7. Mistakes in Your Credit Report

- What to Do After Getting Denied for a Business Credit Card

- How to Increase Your Chances of Getting a Business Credit Card

- Frequently Asked Questions (FAQs)

- Bottom Line

1. Credit Score Issues

Your credit score is an important deciding factor when it comes to applying for business credit cards. Most card issuers will perform a personal credit check as part of the application process. Typically, having a bad credit score will result in a rejected credit card application. Most cards require at least good standing (i.e., credit scores ranging from 670 to 739) to qualify.

Several factors could affect your credit score, such as:

- Paying bills late

- Incurring too much debt

- Having account defaults

Apply for a secured business credit card to help build or improve your credit score. To apply for a secured credit card, you only need to provide a security deposit as collateral. For recommendations, check our list of the best secured business credit cards.

2. Verification Issues With Your Business Details

Card issuers may deny your business credit card application if they cannot confirm your business’s legitimacy or the accuracy of the provided data. They may view the business as a risk and reject the application to avoid potential fraud or mismanagement.

Ensure you have all necessary business documents ready before starting your credit card application. Accurately complete the required business information to avoid delays or, worse, denial of your application.

Required Business Information for Credit Card Application

There is certain information that you will need to provide when applying for a business credit card. Oftentimes, issuing banks may have difficulty verifying certain information as you may have incorrectly inputted the following:

- Business name: Sole proprietors can apply with their legal name, while LLCs, corporations, and partnerships must use their registered business name.

- Employer Identification Number (EIN)

- Entity status: You must indicate if you’re a sole proprietor, LLC, corporation, or partnership.

- Business phone number: An active business phone number is required for all entities so that issuing banks can contact you.

- Commercial address: Sole proprietors can use their home address, but LLCs, corporations, and partnerships must use a commercial address, not a P.O. Box or residential address.

Read our guide on how to get a business credit card for more information—we include the common requirements you’ll need before applying.

3. Business Is New or Unestablished

New businesses typically have difficulty getting approved for a business credit because most providers require a certain number of years in business as part of the qualification process. Without a proven track record of revenue and stable cash flow, it’s harder for issuers to gauge the business’s ability to repay debt. In these cases, card issuers may rely more heavily on the personal credit of the business owner—and if that’s not strong, the chances of denial increase.

Build your personal credit by paying all bills on time and keeping credit card balances low. Regularly monitor your credit report for errors and consider opening a secured credit card to strengthen your credit history. Moreover, choose business credit cards that qualify new businesses. Check our roundup of the best credit cards for new businesses for options.

4. Too Many Financing Applications

Card issuers may deny your credit card application if there is a hard credit pull or inquiry in your account. The number and frequency of hard pulls can signal lenders that you’re actively seeking financing in multiple places, which might raise concerns. This makes it harder for credit providers to assess your credit accurately, as recent debts or obligations might not yet appear on your report.

Seek for cards that have qualification requirements matching your eligibility before applying. Research thoroughly and, if possible, get prequalified to avoid multiple hard credit pulls on your account.

5. Not Enough Income

Credit card issuers evaluate your business credit card applications based on the business owner’s personal income and debt-to-income (DTI) ratio to assess creditworthiness. If the business owner doesn’t meet income requirements or has a high DTI, the issuer may deny the application.

Look for business credit card providers that are more lenient when it comes to income requirements. Make sure to determine the eligibility requirements first so you will know which card you can qualify for, considering your income.

6. Insufficient Credit History

Short or nonexistent credit history can lead to a business credit card denial because card issuers use it to assess your financial reliability. Without a credit history, issuers can’t evaluate how well you manage debt or make timely payments.

This lack of information makes you a higher risk, as the issuer has no track record to gauge your ability to repay the credit, leading to potential denial of your application. Essentially, no credit history signals uncertainty to credit card issuers.

Open a business credit account with a provider that reports payments to credit bureaus. Consistently making on-time payments will help establish your business credit history, which can improve your chances of qualifying for a business credit card later on.

7. Mistakes in Your Credit Report

Credit card issuers rely on the information in your credit report to assess your creditworthiness. Errors like an incorrect payment history, accounts that don’t belong to you, or inaccurate balances can negatively affect your credit score. These may make you appear riskier to providers, even if you’re financially responsible. If they see missed payments or high debt (even if they’re incorrect), they may deny your application based on that faulty information.

Check your credit report regularly and file a dispute with the credit bureau (Equifax, Experian, or TransUnion) if you spot any errors.

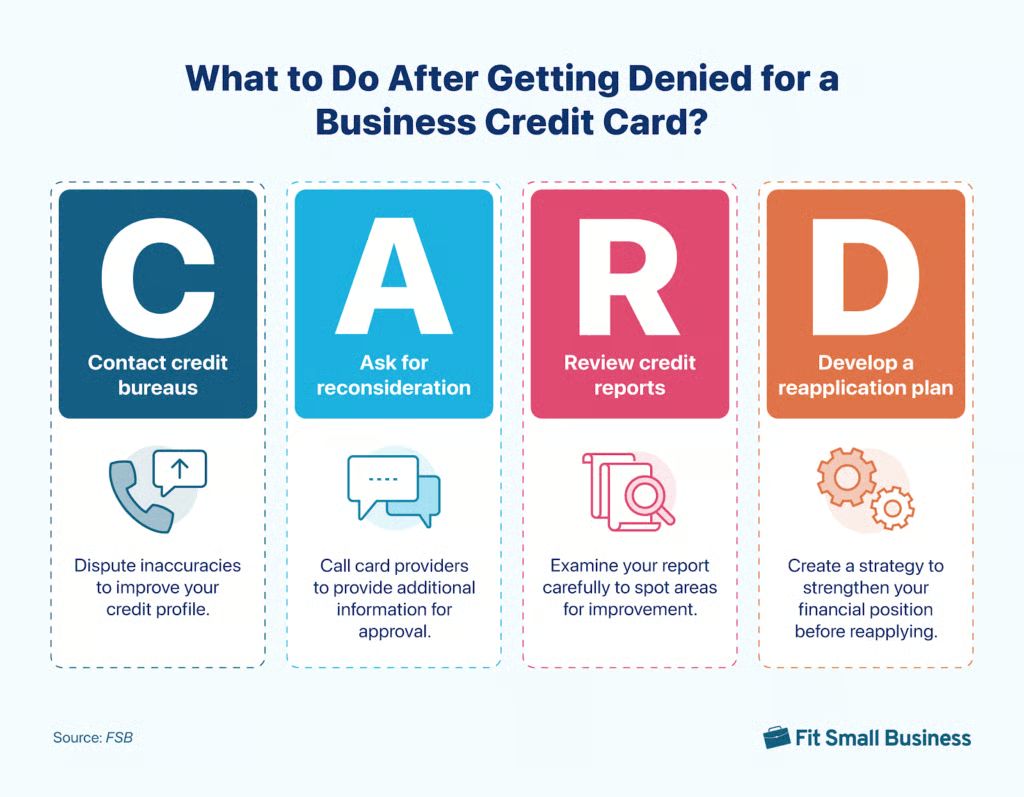

What to Do After Getting Denied for a Business Credit Card

After receiving a denial letter from the card issuer, there are immediate actions you can take to improve your chances of success in the future. To help you remember, we call them our CARD tips, which include the following:

- Contact credit bureaus for a dispute if you find any inaccurate information on your credit report. Once the inaccuracies are confirmed, you can have them corrected or removed, improving your overall credit profile.

- Ask for reconsideration by calling the card provider and providing additional information or clarification. Understand the specific reason for the rejection, whether it’s due to a low credit score or missing details, and address those issues to improve your chances of approval.

- Review credit reports carefully to understand your full credit standing. By examining the details, you can identify areas that need improvement and take steps to enhance your credit profile.

- Develop a plan for reapplication by crafting a clear strategy to strengthen your financial position. Focus on resolving the issues that caused the denial, such as improving your credit score or reducing debt, before submitting a new application.

How to Increase Your Chances of Getting a Business Credit Card

There are several effective ways to increase your chances of getting a business credit card, many of which address the common reasons for initial denial. To make it easy to remember, we’ve named them our STAR tips, which include the following:

- Start building your credit history by borrowing money and making timely payments from a vendor or suppliers that submit reports to credit bureaus.

- Take a credit builder card where the loan amount is held in a savings account while you make monthly payments. Once you’ve completed the loan term, the funds are released to you, and your consistent payment history is reported to the credit bureaus, helping to build or improve your credit.

- Add yourself as an authorized user on someone else’s credit card to benefit from the primary cardholder’s credit score, as long as payments are managed responsibly.

- Reduce existing debts to keep your debt-to-income (DTI) ratio low, demonstrating your ability to manage additional credit, such as a new business credit card.

We have expert-approved business credit card tips that may be of interest to you. Each tip can help you avoid common credit card pitfalls so that you can take advantage of the benefits of your business credit card.

Frequently Asked Questions (FAQs)

What types of business credit cards can improve my approval chances?

Business credit cards that can boost your approval chances if you have limited credit history include:

- Secured business credit cards: Require a security deposit, making them easier to obtain.

- Cards for fair or average credit: Designed for those with less-than-perfect credit scores.

- Business charge cards: Often have more lenient approval criteria, but must be paid in full each month.

Will my credit score be affected if I get denied for a business credit card?

No, it won’t. The denial itself doesn’t hurt your credit score—it’s the hard inquiry associated with the application that causes a few points lower in your score.

Can I reapply after being denied a business credit card?

Yes, you can. However, it’s important to first address the reason you were denied. Whether it’s improving your credit score, correcting application errors, or boosting your revenue, making these changes can increase your chances of success on your next attempt.

Bottom Line

Getting denied for a business credit card may be disheartening, but it’s often an opportunity to understand where improvements need to be made. By taking our actionable tips, you can improve your creditworthiness and increase your chances of approval next time.