Special event insurance is primarily a liability insurance policy for a business, vendor, or individual hosting an event. The policy provides coverage for injuries and damaged property, with additional options like weather cancellation. Unlike other policies, special event insurance is a policy with one payment, with average premium costs starting at $100 or $500 for events with 100 or 3,000 attendees, respectively.

Key Takeaways

- Special event insurance coverage is a special policy that provides liability coverage for a short period.

- Special event insurance is necessary for businesses hosting or organizing events that are off-site or significantly different from the company’s daily operations, like holiday parties and employee retreats.

- Usually, this policy has additional coverages for property or other losses specific to the event, like jewelry coverage for a wedding.

- Policies range from $100 to $400 for an event with at least 100 and no more than 250 attendees.

Event Insurance Costs

Event insurance is a one-time payment, and unlike most insurance policies, many policies do not come with a deductible. But if they have a deductible, it’s usually for the third-party property damage portion and starts at $500.

Number of Attendees | Liability Coverage Limit | Average Premium Costs |

|---|---|---|

100 | $1 million per occurrence/$2 million aggregate | $100 - $400 |

500 | $1 million per occurrence/$2 million aggregate | $150 - $450 |

1,000 | $1 million per occurrence/$2 million aggregate | $175 - $500 |

3,000 - 5,000 | $1 million per occurrence/$2 million aggregate | $500 - $800 |

Factors That Impact Event Insurance Costs

When shopping for event liability insurance, be prepared to answer questions about the event—such as location, date, type of event, and what activities will be present. For example, will there be live animals or a dunk tank? Questions like these will influence whether the insurance company will cover the event and the premium amount.

And while a few insurers will offer coverage up to 24 hours before the start of the event, many require advance notice. Keep your event timeline in mind when shopping for insurance.

Other factors influence special event insurance costs and availability.

- Limits: The above quotes are all for the same $1 million liability limit. Increasing the limit will increase the premium you pay. But for an important event, it’s worth it to have the added protection.

- Alcohol service: Are you selling alcohol, or will a vendor sell it? While some event liability packages include liquor liability, some will require that you purchase liquor liability insurance as an added coverage.

- Expected turnout: The more people at your event, the greater the likelihood that they will be injured, and thus, the event insurance costs will increase.

- Type of event: The cost to cover a small corporate holiday party for your business will differ from a three-day music festival.

- Length of event: The time of the event, including set-up and tear-down, will likely impact the cost of insuring the event.

- Structures: Are there temporary structures like large tents, stages, or a bounce house for your event? If so, understand that temporary structures increase the risk of injury and property damage and will impact your premium rate.

- Deductible: Not all special event insurance policies include an insurance deductible. But if you have one that does, adjusting it can help with the cost. For example, if you raise the deductible, the premium should decrease. This approach comes with a risk since if you file a claim, you will owe the deductible.

Special Event Insurance Coverage

Like a business owner’s policy (BOP) that combines first-party losses with third-party liability exposures, event insurance usually has two core components built into the policy.

- Event liability coverage protects your business if someone is injured at your event. For example, a guest slips on some water and breaks their ankle while at a business expo for mops. Upset at the faulty mophead, the salesperson kicks a hole in the wall of the rented venue. Event liability helps cover the broken ankle and the damaged wall.

- Event cancellation coverage helps protect any nonrefundable deposits or loss of profits should you have to cancel an event. Let’s say a hurricane shuts down your outdoor event or a blizzard closes the roads to your indoor event, and you have to cancel. Event cancellation coverage protects you from losses.

This is a high-level overview, and the specific coverages available will change depending on the type of event. For example, a wedding event insurance policy often has additional options for unforeseen losses involving photography, videography, attire, and even jewelry. Many insurance companies offer additional coverages, such as hired auto, contractual liability, or accident medical expenses.

As is the case when shopping for insurance, if you are honest with the insurance company about what type of event you are hosting, it will be honest about whether it will write a policy for it.

Pro Tip: When planning your event, factor in when the coverage terminates. Providers may have a specific cut-off time for the event insurance. For example, Travelers’ wedding insurance ends at 2 a.m. after the event.

What Special Event Insurance Doesn’t Cover

This type of insurance isn’t for every event. The range of what type of event is and is not covered varies by insurer. Some have a much greater capacity for high-risk events, while others will limit it to events like weddings, graduations, and retirement parties. Still, in general, the following are usually not covered:

- Activist rallies and marches

- Organized protests

- Cancellation due to communicable diseases

Additionally, high-risk events like gun shows and tractor pulls, while not impossible to find coverage, may prove challenging to do so or may cost a lot more than event coverage for a wedding.

Did You Know? Most insurance providers now have an epidemic/pandemic exclusion for the cancellation portion of their coverage. Check the terms of your policy carefully as they relate to communicable diseases.

The Case for Special Event Insurance: Covering Losses for Canceled Events

Unfortunately, because of the threat of a potential terrorist attack, Taylor Swift recently canceled several concerts in Vienna, Austria. Because she cancels tours so infrequently, Taylor is considered a low risk when it comes to insurability for special event insurance. The reported cancellation of these three shows will likely cost the insurance companies thousands of dollars.

While most small business owners don’t own an event company hosting a Taylor Swift concert, the story illustrates how it works. The concert was canceled unexpectedly, and because of that, customers lost out on money.

Different businesses associated with the venue have either lost business income or lost money they invested in preparing for the event. For any of those situations, special event insurance can help cover losses from unexpected cancellations.

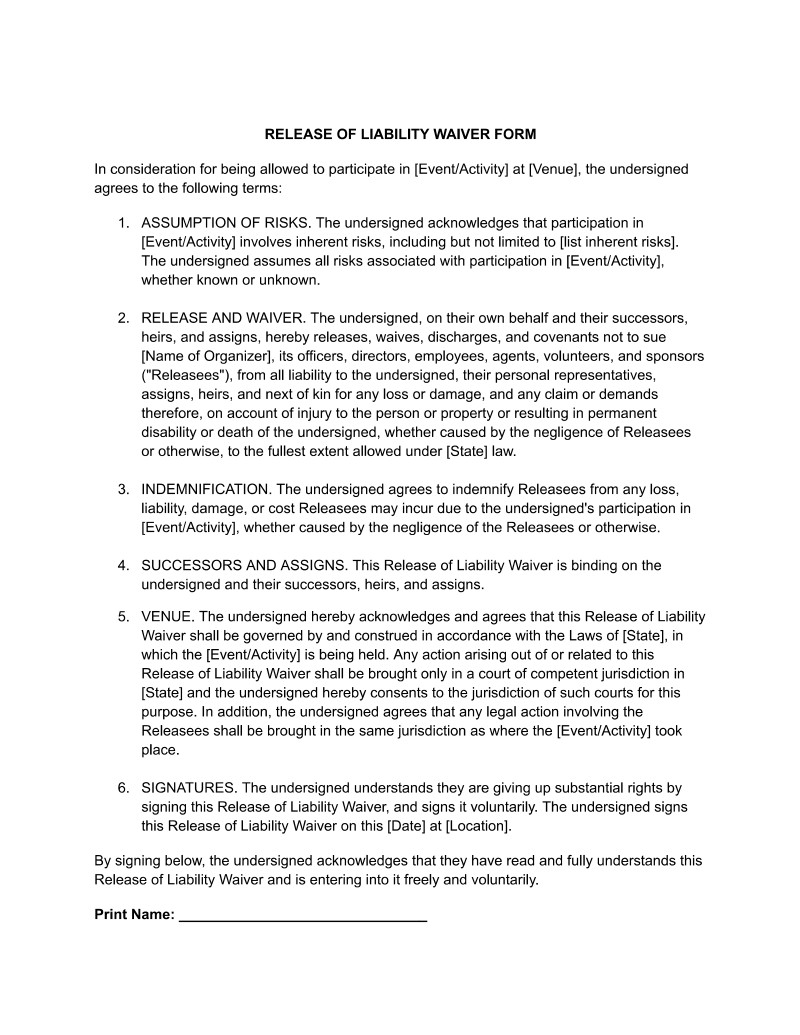

Liability Waiver for Events

Some insurers may ask that you use a waiver or will consider lowering your special event insurance costs if you can demonstrate actionable steps to mitigate or transfer liability.

A liability waiver, sometimes called a release of liability or a general waiver, is a document that a business has patrons sign to acknowledge risks and release the business from claims arising from injury or loss. It cannot violate state law and is common in recreational, fitness, and high-risk businesses.

Download a free Business Liability Waiver Template for your business

Thank you for downloading!

Special Event Insurance for Businesses

Businesses typically need special event insurance if they are hosting and organizing the event. Generally, you will need to purchase this coverage if your event is off-site or significantly different from your company’s daily operations, like holiday parties and retreats.

- Holiday parties: If you’re hosting a holiday party with entertainment, caterers, and alcohol, consider event insurance that includes liquor liability.

- Company picnics: Everyone loves the annual company picnic with the bounce house and the family games, but that sack race could lead to a lawsuit if someone gets hurt.

- Fundraisers: Nonprofits often host a catered meal at an off-site location. With the cost of deposits and the potential for liability, nonprofits should consider special event insurance.

- Employee retreats: Many companies will have a retreat for team building. However, many of the exercises at these events, such as the “trust fall,” are a liability nightmare.

Event Insurance for Vendors

If your small business will be a vendor at a special event, you’ll want to discuss what insurance you may need with the host. Generally, you will need liability insurance to protect your assets if a client or the venue owner accuses you of causing bodily injury or property damage. If, as the vendor, you are serving alcohol, most special event policies taken out by the host will require the vendor serving alcohol to have a liquor liability policy.

Some venues require proof of liability insurance to book them. The certificate, or COI, will show them you have the required coverage and, if necessary, list the host as an additional insured. When a host venue requests to be added as an additional insured, it adds a layer of liability protection to their business by making your policy the primary coverage if something happens.

As you shop for special event insurance policies, consider companies that provide an instant COI to prevent any delays in booking or planning.

Special Event Insurance for Individuals

Special event insurance isn’t just for businesses. Individuals may want to purchase a policy, too, especially if they have a lot of money invested in the event. Events an individual may want to purchase special event insurance for the following:

- Bar mitzvahs and bat mitzvahs

- Quinceañeras

- Family reunions

- Retirement parties

- Anniversary parties

- Weddings

Wedding event insurance is probably the most common form of special event insurance a private individual will purchase. As with special event insurance, its primary coverage is liability and event cancellation. Many insurance companies offer additional coverage for wedding gowns, tuxedos, jewelry, and accessories. Just remember, insurers won’t cover cancellations if someone gets cold feet and changes their mind.

How to Purchase Special Event Insurance

Many insurers will not offer special event insurance. Even large brokers that work with over a dozen providers don’t sell it. You’ll most likely need to turn to a specialty insurer to find special event insurance.

To do that, locate an independent agent or carrier in your area for help with location and some insurers that will cover your event. Or review our roundup of the best special event insurance companies.

Frequently Asked Questions (FAQs)

Most insurers will offer cancellation insurance coverage, but whether you get money back depends on the nature of the event and the reason for cancellation. Not every event that leads to a cancellation will be covered. For example, communicable diseases are almost universally excluded from cancellation coverage.

Most venues require a minimum amount of liability coverage to participate in an event as a vendor. Venues request proof of insurance or a certificate of liability to ensure you have the proper coverage. Your proof is a simple one-page document summarizing your coverage.

Many carriers allow you to go online and adjust your limits. If you can’t do this through your online account, reach out to your agent or call the carrier directly to make changes.

Bottom Line

If you are a business or private individual planning to host a large event, you will want to look into event insurance. Whether it’s for your special day or an important milestone in your company, getting coverage can protect you if anything goes wrong.