Commercial general liability insurance, often called CGL insurance, helps protect businesses from costly third-party claims like bodily injury, property damage, and personal or advertising injury. A standard commercial general liability policy can cover everything from a customer slipping in your office to damage caused by your work.

For many small businesses with around $200,000 in annual revenue, CGL policy insurance typically costs anywhere from $170 to $13,000 per year, with the wide price range reflecting how risky a business’s industry and operations are.

A great way to quickly find affordable general liability is through a broker like Simply Business, which offers CGL to small businesses. In 10 minutes or less, you can get free, no-obligation quotes from multiple providers. After comparing coverage and price, you can purchase a policy online without speaking with anyone.

- How much does commercial general liability insurance cost?

- Commercial general liability insurance costs by profession

- Factors that impact CGL insurance costs

- Commercial general liability insurance coverage

- What commercial general liability insurance doesn’t cover

- Who needs CGL insurance?

- Ways to get commercial general liability insurance

- How to get proof of general liability insurance

- Bundling general liability insurance

- Commercial general liability enhancements

- Frequently asked questions (FAQs)

- Bottom line

How much does commercial general liability insurance cost?

One of the easiest ways to find affordable commercial general liability insurance is by working with an online broker like Simply Business. The platform lets small business owners compare CGL insurance quotes from multiple carriers in about 10 minutes, all at no cost and with no obligation. You can review coverage options, compare prices, and purchase a CGL policy insurance online, often without needing to speak with an agent unless you want extra guidance.

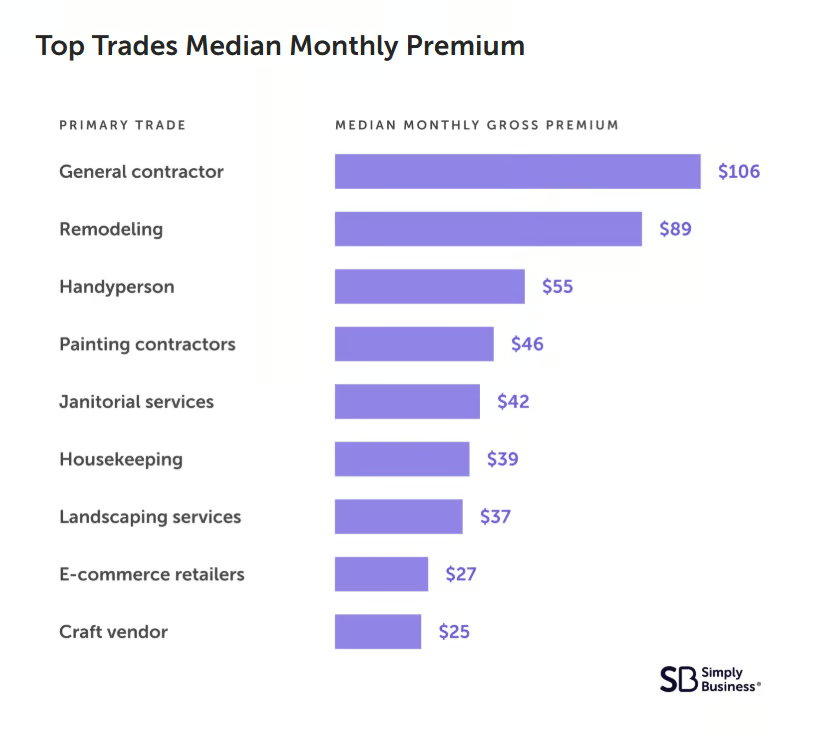

Your actual premium may be higher or lower, but these examples should give you a realistic sense of what general liability insurance typically costs. For instance, the average monthly cost as a general contractor is $106.

Commercial general liability insurance costs by profession

Commercial general liability insurance costs can vary widely depending on what your business does. Some professions carry minimal risk, while others face higher exposure to injuries, property damage, or customer interactions. The table below shows typical CGL insurance costs by profession, giving you a clearer idea of how industry risk influences both monthly and annual pricing for a commercial general liability policy insurance.

| Industry type | Average monthly cost | Average annual cost |

|---|---|---|

| Low-risk services (consultants, IT) | $25–$45 | $300–$550 |

| Retail & small offices | $40–$70 | $480–$840 |

| Food vendors & events | $60–$130 | $720–$1,560 |

| Contractors & trades | $90–$300+ | $1,100–$3,600+ |

Factors that impact CGL insurance costs

The cost of commercial general liability insurance is not one-size-fits-all. Insurers look at a range of business details to assess risk and determine how much your CGL insurance premium will be. Some factors carry more weight than others, but together they shape the final price of a commercial general liability policy insurance.

- Location: Where your business operates plays a role in CGL insurance pricing. Local laws, claim trends, and environmental risks can all affect premiums. For example, businesses in hurricane-prone states like Florida often pay more due to higher potential claim severity.

- Hours of operation: Businesses open longer hours or late at night generally face more exposure. A 24/7 gym or a bar open past midnight typically pays more for CGL policy insurance than a business open standard weekday hours.

- Claims history: If your business has filed general liability claims in the past three to five years, insurers may raise your premium or decline coverage altogether. A clean claims history usually leads to lower commercial general liability insurance costs.

- Revenue: Higher revenue often means more customers, more transactions, and more chances for something to go wrong. As revenue increases, so does risk exposure, which can raise your CGL insurance premium.

- Number of employees: The more employees you have interacting with customers, equipment, or job sites, the greater the chance of a claim. Employee count and training both influence commercial general liability policy insurance pricing.

- Industry type: Industry risk is one of the biggest pricing drivers. For example, a residential cleaning company typically pays less than a cleaning business that services airports, schools, or industrial facilities.

- Inherent risk of your work: Even within the same profession, risk levels can vary. A carpenter installing wood-burning fireplaces will usually pay more for CGL insurance than one installing kitchen cabinets.

- Coverage limits: Higher limits mean higher premiums, although the increase is often smaller than expected. It is worth weighing whether you truly need very high limits or if a more modest amount provides adequate protection.

Why accuracy matters when getting a CGL insurance quote

It can be tempting to leave out details when applying for commercial general liability insurance in hopes of lowering the price. That approach can backfire. Insurers rely on accurate information to price and approve coverage. Misrepresenting your business, even unintentionally, can result in denied claims later. Coverage investigations like these can lead to denied claims, and the financial consequences are often far more costly than paying a slightly higher premium upfront.

Being honest about your operations and claims history does not mean you cannot find affordable CGL policy insurance. Many small businesses qualify for competitive rates while still fully disclosing their risk.

Commercial general liability insurance coverage

Commercial general liability insurance provides broad protection against many of the most common risks small businesses face. A CGL policy insurance is designed to cover third-party claims related to injuries, property damage, and certain nonphysical harms tied to your business operations.

Most commercial general liability policy insurance includes two main limits:

- Per-occurrence limit, which is the maximum the policy will pay for a single claim

- Aggregate limit, which is the total amount the policy will pay during the policy period

Within those limits, CGL insurance includes several specific types of coverage.

What a CGL policy typically covers

| Coverage type | What it covers | Limit notes |

|---|---|---|

| Property damage |

| Shares an aggregate limit with bodily injury |

| Bodily injury |

| Shares an aggregate limit with property damage |

| Personal and advertising injury |

| May have a separate limit depending on the insurer |

| Medical payments |

| Separate limit, often around $5,000 |

| Product liability |

| Often has its own coverage limit |

| Damage to premises rented to you |

| Typical limit around $100,000 |

How CGL coverage is structured

Commercial general liability insurance is generally divided into three parts:

- Coverage A: Bodily injury and property damage

- Coverage B: Personal and advertising injury

- Coverage C: Medical payments

What commercial general liability insurance doesn’t cover

Commercial general liability insurance is designed to protect your business from claims made by other people, not losses to your own property or employees. Because of that, there are several common situations that a CGL policy insurance does not cover.

Common exclusions under CGL insurance

| Not covered by CGL | What you need instead |

|---|---|

| Damage to your own property | Commercial property insurance to protect equipment, inventory, and office space from theft, vandalism, or damage |

| Professional mistakes or bad advice | Professional liability insurance to cover errors, omissions, and service-related claims |

| Employee injuries or illnesses | Workers’ compensation insurance to cover medical costs and lost wages |

| Employment-related claims | Employment practices liability insurance (EPLI) for harassment, discrimination, or wrongful termination claims |

Who needs CGL insurance?

Most small business owners should strongly consider carrying commercial general liability insurance, even when it is not legally required. CGL insurance is a foundational policy that helps protect businesses from common third-party claims that can arise during day-to-day operations.

You may be required to carry a commercial general liability policy insurance if you:

- Rent or lease a business space

- Work at client locations

- Participate in trade shows, markets, or public events

- Need to meet licensing or certification requirements

- Work with government agencies or public contracts

When CGL insurance is required

In most states, there is no blanket requirement for general liability insurance. However, many licensing boards, landlords, event organizers, and government entities require proof of CGL insurance before allowing you to operate, sign a contract, or access a job site.

Contractors working on local, state, or federal projects are almost always required to carry commercial general liability insurance as part of their contract terms.

In some cases, states may mandate CGL insurance for specific industries. For example, Maryland requires security guard companies to register with the state police and provide proof of general liability insurance before operating.

These businesses, in particular, should purchase general liability:These businesses, in particular, should purchase general liability:Click to show

- Auto body shops

- Beauty and hair salons

- Churches

- Contractors

- Daycares

- DJs & videographers

- Electricians

- Food trucks

- Food vendors

- Gyms owners

- Handypersons

- HVAC technicians

- Janitorial & cleaning services

- Landscapers

- Nannies

- Nonprofits

- Painters

- Personal trainers

- Restaurants

- Swim instructors

- Bakeries

Why general liability claims are becoming more expensive

Commercial general liability insurance protects businesses as liability claims continue to grow in both frequency and severity.

Recent industry reporting shows that large liability claims are becoming more common, with jury awards reaching into the tens of millions across multiple industries. These outcomes are often driven by rising medical costs, increased litigation expenses, and changing jury expectations. As a result, the average cost of general liability claims has continued to increase year over year.

Data from insurance analytics firms indicates that liability claim severity, meaning the average cost per claim, has risen substantially in recent years. Higher legal fees and larger settlements have contributed to this trend, putting greater financial pressure on businesses without adequate coverage.

Without commercial general liability insurance, a business found legally responsible for an incident would be fully responsible for medical bills, legal defense costs, settlements, and court judgments. In today’s legal environment, even a single serious claim can create expenses that reach hundreds of thousands or even millions of dollars.

Ways to get commercial general liability insurance

When you are ready to purchase commercial general liability insurance, you can choose from several common options based on how much guidance you want and how involved you want to be in the process.

You can get CGL insurance by:

- Buying directly from an insurance carrier. Contact an insurance company that underwrites commercial general liability policy insurance and request a quote. This option works best if you already know what coverage you need and want to work directly with a provider.

- Working with an insurance broker or agency. A broker or agency compares CGL insurance options from multiple carriers and helps you find coverage that fits your business risks and budget. This is a good choice if you want expert guidance and pricing comparisons.

- Using an insurance referral service. A referral service matches your business with a broker or agent based on your industry, location, and insurance needs. This option can save time if you are not sure where to start.

How to get proof of general liability insurance

Proof of general liability insurance is typically provided in the form of a certificate of insurance, often called a COI. You can request a COI directly from your insurance provider after your commercial general liability policy insurance is active.

Many insurers allow you to generate a certificate instantly through an online dashboard or mobile app. Other providers may require you to submit a request or contact your agent, who will issue the certificate on your behalf.

If you work in an industry where clients, landlords, or event organizers regularly ask for proof of CGL insurance, it is worth choosing a provider that makes certificates easy to access and share. Fast access to COIs can help prevent delays when signing contracts or booking jobs. Some insurers offer digital tools that let policyholders create and send certificates online or through a mobile app.

Bundling general liability insurance

While you can purchase general liability insurance on its own, many small businesses choose to bundle it with other coverage. The most common option is a business owner’s policy, often called a BOP.

A BOP combines multiple types of commercial coverage into a single policy, typically including:

- Commercial property insurance

- Commercial general liability insurance

- Business interruption coverage

This bundled approach is designed specifically for small businesses that need broad protection without managing multiple separate policies.

Why businesses choose to bundle CGL insurance

Bundling general liability insurance into a business owner’s policy offers several advantages.

- Simpler coverage management. You manage one policy with one insurer, which makes renewals, billing, and policy changes easier to handle.

- Lower overall cost. A BOP is usually more affordable than purchasing commercial general liability insurance, property insurance, and business interruption coverage separately.

- Easier shopping experience. Instead of comparing multiple standalone policies, you only need to evaluate one bundled option, which can save time and reduce confusion.

Commercial general liability enhancements

One of the advantages of a commercial general liability policy insurance is how flexible it can be. Many insurers allow you to expand a standard CGL insurance policy with endorsements, sometimes called riders. Endorsements add specific types of coverage to better match your business risks without requiring a separate standalone policy.

Below are some of the most common enhancements businesses add to their CGL policy insurance:

Hired and non-owned auto

This endorsement extends coverage to vehicles your employees use for business purposes that your company does not own. It is often useful for businesses like restaurants or delivery services, where employees drive their own cars for work.

Tools and equipment coverage

Contractors and service professionals can add coverage for tools and equipment through an endorsement. While CGL insurance mainly covers third-party claims, this add-on provides limited first-party protection for tools without purchasing a separate policy.

Errors and omissions

Also known as professional liability insurance, errors and omissions coverage protects against claims related to professional mistakes or failure to deliver services as promised. Some insurers include this coverage automatically for certain industries, while others offer it as an optional endorsement.

Liquor liability

Standard commercial general liability insurance does not cover alcohol-related incidents. Businesses that sell or serve alcohol, such as restaurants or bars, may be able to add liquor liability as an endorsement to extend coverage to alcohol-related claims.

Sexual abuse and molestation coverage

Businesses and organizations that work closely with children or vulnerable populations may need this endorsement. It provides protection against claims related to abuse allegations and is commonly added by daycares, camps, counseling services, and religious institutions.

These are just some of the most common ways to expand a commercial general liability policy insurance. Available endorsements vary by insurer and industry, and some businesses may have access to many additional options. Reviewing endorsements carefully helps ensure your CGL insurance aligns with how your business actually operates.

Frequently asked questions (FAQs)

Does a sole proprietor need general liability insurance?

Yes. Any business that interacts with customers or the public should strongly consider commercial general liability insurance. Whether you operate as a sole proprietor or an LLC, CGL insurance provides the same type of protection against third-party claims.

Is general liability insurance legally required?

In most states, general liability insurance is not required by law. However, it is often required by landlords, clients, event organizers, or licensing authorities. Many businesses must also provide proof of CGL insurance in the form of a certificate of insurance (COI) when signing contracts.

What does CGL cover?

Commercial general liability insurance helps protect your business from claims related to negligence, including bodily injury, property damage, and personal or advertising injury. Coverage typically includes legal defense costs, settlements, and judgments tied to covered claims.

Is general liability insurance the same as product liability?

No. General liability insurance and product liability insurance are different, but they are closely related. Product liability covers injuries or damage caused by products your business manufactures or sells. Many commercial general liability policies include product liability coverage, but it is important to confirm this with your insurer.

How much does CGL insurance cost?

Most small businesses pay between $170 and $13,000 per year for commercial general liability insurance, though costs vary by industry, location, and risk level. Low-risk businesses may pay less, while higher-risk businesses, such as contractors or HVAC companies, may pay significantly more.

Do I need commercial general liability if my business is an LLC?

Yes. Forming an LLC does not prevent your business from being sued. Commercial general liability insurance helps cover legal defense costs, settlements, and judgments if your business is found legally responsible for a claim, regardless of its legal structure.

Do I need any other type of insurance apart from CGL coverage?

Often, yes. While commercial general liability insurance is a core policy, many businesses need additional coverage. Workers’ compensation insurance is required in most states if you have employees. Depending on your operations, you may also need professional liability, commercial property, or commercial auto insurance.

Bottom line

Commercial general liability insurance is a foundational form of protection for most small businesses. It helps cover the cost of third-party claims involving bodily injury, property damage, and certain nonphysical harms that can arise during everyday operations. While CGL insurance is not legally required in most states, it is often necessary to meet contract, licensing, or landlord requirements.

Costs vary based on industry risk and business size, but for many small businesses, the price of coverage is far less than the financial impact of a single liability claim. Choosing the right policy and coverage limits can help protect your business and keep unexpected claims from becoming a major setback.