Payroll reconciliation helps ensure employees are paid correctly and that payroll transactions are recorded accurately in your accounting records. Done consistently, it reduces errors, supports compliance, and prevents small discrepancies from turning into costly fixes, penalties, or employee frustration.

There are two components to payroll reconciliation. The first is reconciling a payroll cycle before processing it, and the second is performing a balance sheet reconciliation to find errors. This guide will walk you through everything you need to know to complete both and make pay runs a little less stressful.

Tools like QuickBooks Workforce (formerly QuickBooks Payroll) can help by posting payroll entries directly to the general ledger, tracking payroll liabilities, and minimizing manual data entry. This makes payroll account reconciliation easier to manage and more consistent over time. Sign up today and save 50% on your first three months.

Payroll reconciliation components

Payroll account reconciliation usually has two parts: reviewing payroll details before pay runs and reconciling payroll-related balance sheet accounts after payroll is processed. In small businesses, the first is typically handled by the payroll admin or office manager, while the second is reviewed by a bookkeeper or accountant. I recommend understanding how both work, even if you only handle one, so you can spot issues early and avoid surprises.

Payroll summary reconciliation steps

Before submitting payroll, it’s important to perform a reconciliation to avoid having to correct any potential mistakes. Here are simple steps you can follow:

This report gives you a full snapshot of what payroll is about to look like for a pay period. At this stage, I recommend doing a quick, high-level review. Look for anything that feels off, such as missing employees, unusually high or low pay amounts, or unexpected line items. The next steps are where you’ll dig into pay rates, hours, and deductions more closely.

If you use pay processing tools like QuickBooks Workforce, you can usually pull a payroll register report in just a few clicks and review it alongside prior pay runs. That makes it easier to spot changes or inconsistencies before you move on to the next steps.

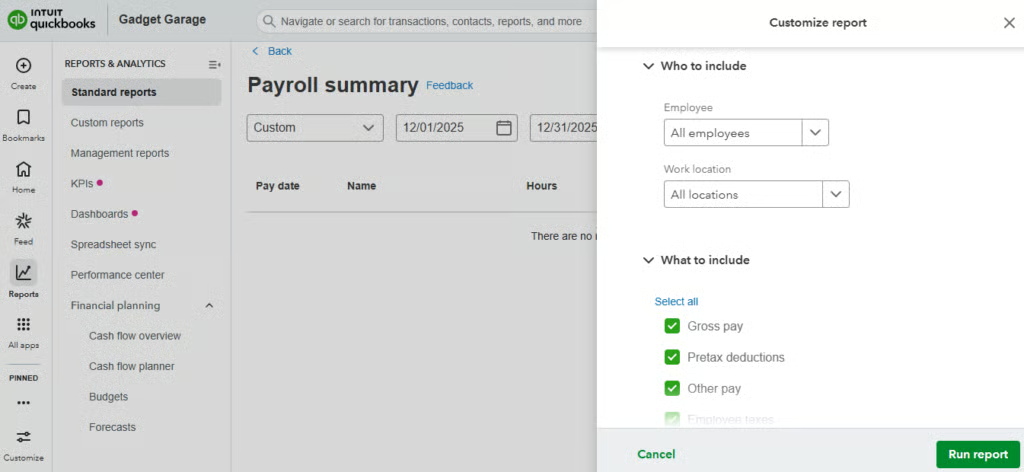

With QuickBooks Workforce, you can create a custom summary report by choosing the details you need, such as the work location, pretax deductions, and more. Source: QuickBooks Workforce

Pay rate errors are one of the most common payroll issues, especially for hourly employees. Rates can change due to role changes, shift differentials, temporary assignments, or promotions, and those updates may not automatically be reflected in payroll.

I suggest comparing the pay rates in your payroll summary to your approved pay rate records. If an employee works multiple roles, double-check that the correct rate was applied to the correct hours.

For hourly employees, their actual hours worked deserve extra attention during payroll account reconciliation. This is where small entry errors can quickly turn into over- or underpayments.

Start by reviewing time records to confirm that regular hours, overtime, and any paid time off were entered correctly for the pay period. Then, double-check overtime calculations, since they’re easy to miss and often the source of employee questions.

If you use payroll software with integrated time tracking, this step is usually more straightforward. For example, QuickBooks Workforce, paired with QuickBooks Time, allows approved hours to flow directly into payroll, which helps reduce manual data entry and the risk of errors.

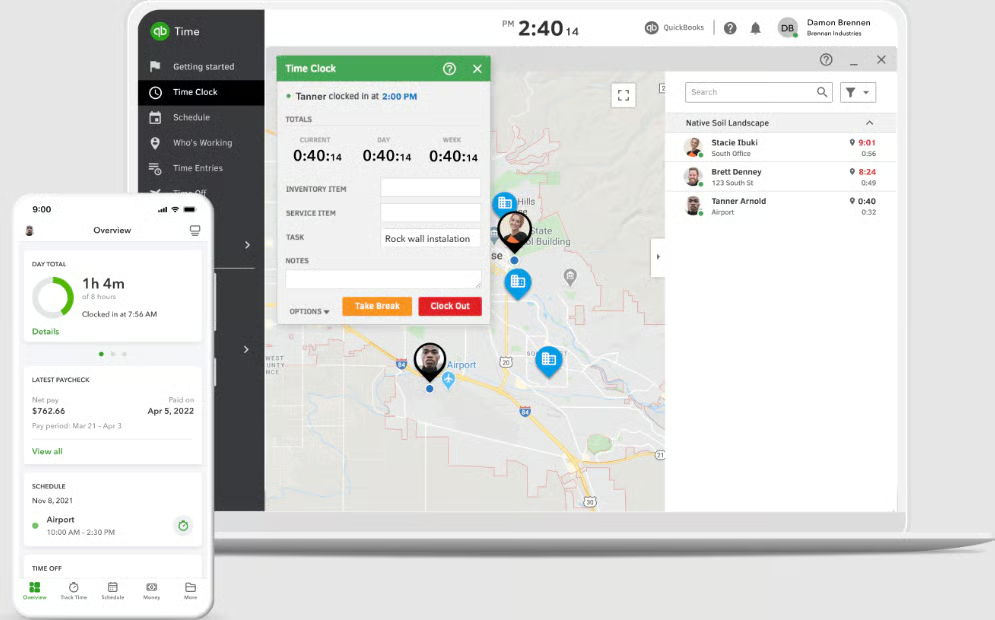

With QuickBooks Time, you can track employee work hours, access timesheets, and approve attendance-related requests online or via the Workforce mobile app. Source: QuickBooks Time

Most payroll deductions stay fairly consistent from one pay period to the next, but they’re still worth reviewing during payroll reconciliation. These regular deductions include, but are not limited to:

- Federal and state income taxes

- Social Security and Medicare

- Health insurance premiums

You should also pay close attention to anything that’s new or one-time for the pay period. This might include benefits adjustments, expense reimbursements, or garnishments. A quick review here helps confirm deductions align with what you expect and prevents surprises after payroll is processed.

Once you’ve reviewed pay rates, hours worked, deductions, and employee details, you’re ready to process payroll. At this point, the goal of payroll reconciliation is to feel confident that what you’re approving matches your expectations for the pay period.

Balance sheet reconciliation steps

This review occurs after payroll is processed and focuses on ensuring that payroll-related accounts in your books reflect what actually happened. The best way to reconcile this is to list all payroll-related balance sheet

To help simplify the process, we have a payroll reconciliation spreadsheet you can use for free. Download the form and follow the step-by-step instructions below.

Start by making a list of the balance sheet accounts you need to reconcile each month. Common payroll-related accounts include:

- Accrued payroll: Wages employees have earned but haven’t been paid yet, often because payroll was processed after the work period ended.

- Payroll tax payable: Federal, state, and local payroll taxes that have been withheld or accrued but not yet remitted.

- 401(k) or retirement contributions payable: Employee retirement contributions, along with any employer match, that have been withheld from paychecks but not yet sent to the plan provider.

- Health insurance payable: Employee-paid premiums and employer contributions that have been recorded as expenses but not yet paid to the insurance provider.

- Garnishments payable: Court-ordered deductions, such as child support or wage garnishments, that have been withheld from employee pay but not yet paid to the appropriate agency.

Keep in mind that most of the accounts you’ll be reconciling will likely be liability accounts. This means the money should stay in the account until you pay it out.

The point of reconciling your payroll accounts is to ensure nothing is lingering too long. When you do find items that don’t clear from your payroll balance sheet accounts each month or quarter, you may likely have forgotten to pay a bill, or a transaction wasn’t recorded correctly.

You’ll need to make copies for each payroll account on the balance sheet and for each month. Label the spreadsheet with the account name and month. You should have a beginning and ending balance for each that ties to the general ledger (GL) balance records. Leave space for reconciling items as well.

Reconciling items are transactions that aren’t reflected correctly or at all in the GL. You’ll find it causes your GL to be out of balance, meaning it won’t be clear how the account’s beginning balance transitioned to the ending balance.

Using payroll software integrated with an accounting system, like QuickBooks Payroll with QuickBooks Online, allows you to export general ledger details reports for each payroll account and use them as the basis for your reconciliation. This makes it easier to trace balances back to specific payroll runs and payments without manually rebuilding the data.

Once your worksheets are set up, gather the payroll reports you need to support payroll account reconciliation. From your accounting system, pull GL detail reports for each payroll-related balance sheet account. These reports should show beginning balances, transactions, and ending balances for the period you’re reconciling.

From your payroll system, gather reports such as:

- Payroll registers

- Payroll tax reports

- Payroll liability reports

- Deduction and benefits reports

If benefits are involved, itemized invoices from insurance or retirement providers can also help explain differences between what was withheld and what was paid.

If you use QuickBooks Payroll with QuickBooks Online, you can trace balances back to specific payroll runs, tax payments, or benefit deductions without jumping between systems. You can even connect your company bank account or corporate credit card to QuickBooks to help you match actual transactions to bank records.

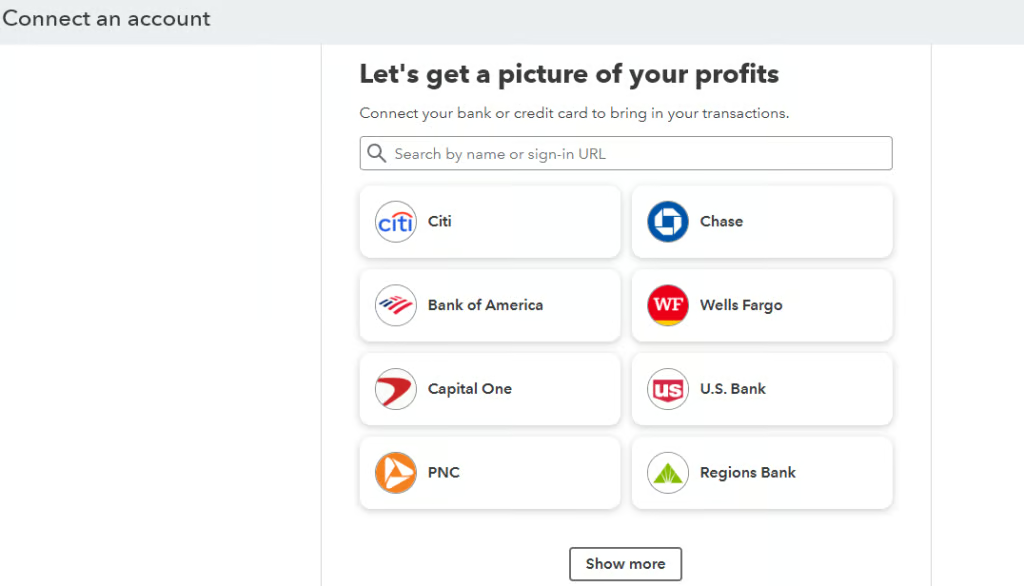

QuickBooks can connect with major banks and credit card companies. Source: QuickBooks

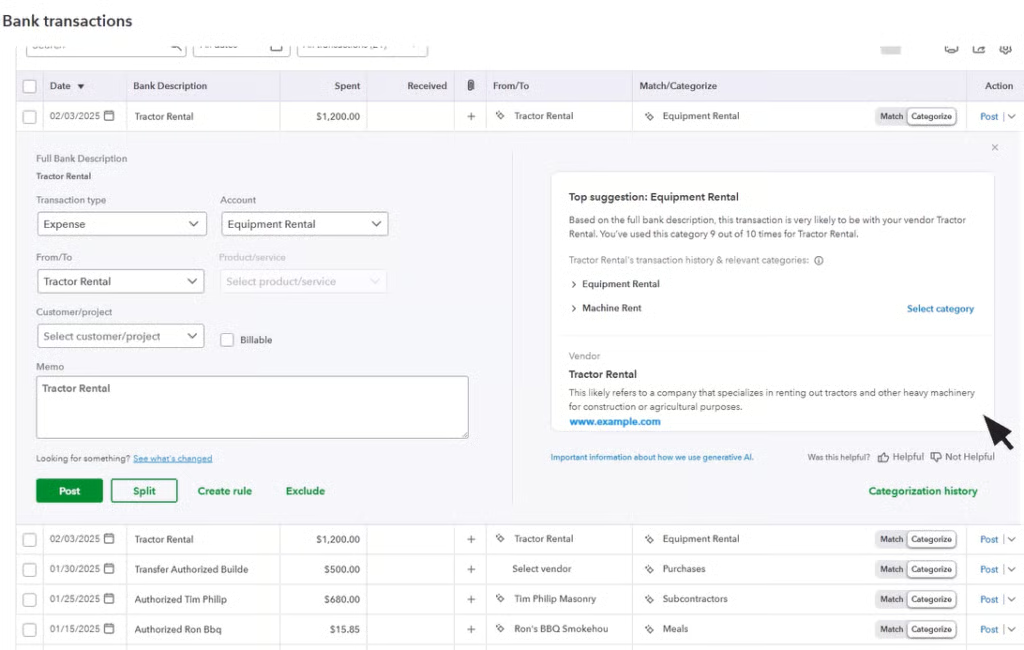

QuickBooks will automatically download your recent bank transactions so you can review, categorize, and add them to your books. This provides you with an easier way of reconciling transactions and reduces the need for manual data entries.

QuickBooks has AI tools that suggest the account that best fits the transaction so you can post it to the correct category (e.g., equipment rental, payroll, etc). Source: QuickBooks Online

Once you’ve gathered your payroll and accounting reports, enter the relevant transaction into your reconciliation worksheet. If your payroll and/or accounting software allows you to export transactions, you can paste them directly into the spreadsheet. Otherwise, you may need to enter them manually.

As you enter the data, compare the transactions from your payroll and accounting reports to the activity recorded in each balance sheet account. This step helps confirm that what was withheld, accrued, or paid through payroll matches what shows up in your books.

If there is a balance at month-end, you’ll need to sift through each debit and credit to find those that did not clear completely. When dealing with numerous transactions, I always found it helpful to delete the debits and credits that net to $0, so it’s easy to see what’s remaining.

Once reconciling items are identified, the next step is to understand why they exist and determine how they should be resolved. In the example above, the first step would be to review the health insurance invoice. Is it itemized by employee?

Also, look at your payroll deduction report for the month. Take a look at the employee paychecks you withheld $500 from for the month, or $250 from each pay period. Are the employees still with the company? Are they showing on the invoice?

Depending on the answers to these questions, you may need to reverse the $500 transaction and refund the employee, work with the insurance company to determine whether the invoice needs to be corrected, or hold the money to pay next month’s bill.

Common payroll reconciliation mistakes to watch for

Even with a solid payroll process, payroll account reconciliation issues still come up. Here are some of the common mistakes:

- Pay rate changes not updated before pay runs: Promotions or pay raises that aren’t captured or entered into the payroll system in time can result in incorrect pay.

- Incorrect or late time entries: Unapproved or manually entered hours increase the risk of under- or overpayments.

- Benefits invoices that don’t match payroll deductions: If an employee leaves or changes coverage and the provider isn’t notified in time, the invoice amount may not align with the payroll deductions.

- 401(k) contributions that need to be reversed: If an employee leaves before contributions are vested, those amounts may still sit in a liability account and require adjustment.

- Employee-paid charges recorded as business expenses: This occurs when costs that should have been covered by employee deductions are mistakenly recorded as company expenses instead.

- Payroll tax payments recorded incorrectly or paid late: Timing differences are common, especially for businesses that pay taxes quarterly.

- Voided payroll-related checks not syncing to the GL: This happens when a check is voided in the payroll system but not reflected correctly in the accounting records (having payroll software that’s integrated with your GL can eliminate this issue, because it automates the process).

Payroll reconciliation frequently asked questions (FAQs)

How often should payroll reconciliation be done?

This should be done every pay period before payroll is processed. Meanwhile, payroll reconciliation for balance sheet accounts is typically done monthly, with additional reviews around tax filing deadlines.

What causes payroll reconciliation discrepancies?

Common causes include incorrect pay rates, missed hours, benefit changes, terminated employees, timing differences in tax payments, or payroll entries that didn’t post correctly to the general ledger.

What happens if payroll isn’t reconciled?

Without payroll reconciliation, errors can go unnoticed, leading to incorrect pay, compliance issues, penalties, and employee frustration.

Can payroll software help with payroll reconciliation?

Yes, it can. Payroll software that integrates with accounting systems — like QuickBooks Payroll paired with QuickBooks Online — can automate journal entries, track payroll liabilities, and reduce manual data entry, making payroll reconciliation easier to manage.

Bottom line

As a small business owner, it won’t hurt to learn how to reconcile payroll. Even if you hire a bookkeeper to handle the reconciliation for you, you still need to know what to expect so you can spot when something is off. If expectations and actual payments don’t match exactly, the differences should be cleared promptly.