Completing Form 1065 starts with document assembly — you’ll need the company’s balance sheet and income statement. If you don’t have those, you can use informal reports or spreadsheets that show totals for the company’s income, expenses, and asset and liability categories.

Once you’ve gathered your documents, fill out the form’s sections for general information and income and /?C “deductions, followed by Schedules B, K, L, M-1, and M-2 (found on Pages 2 through 5). Lastly, you’ll complete a Schedule K-1 for each partner that shows their share of income, deductions, credits, and more.

Thank you for downloading!

Quick Tip

Tax software can make completing your Form 1065 much easier, and will also allow you to file it electronically. TaxAct is our top choice for filing business returns.

I’ll show you how to complete Form 1065 for your partnership using ABC Company’s balance sheet and income statement below.

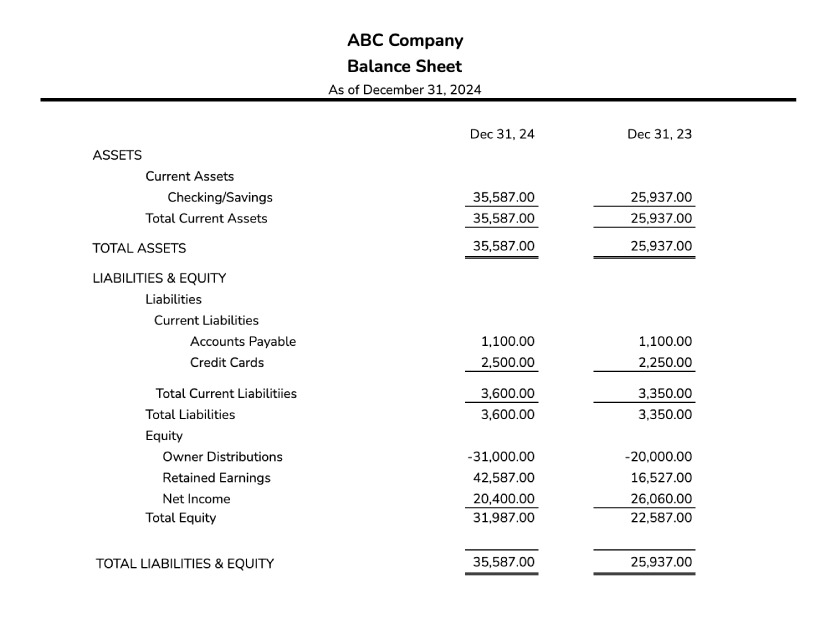

ABC Company’s Balance Sheet

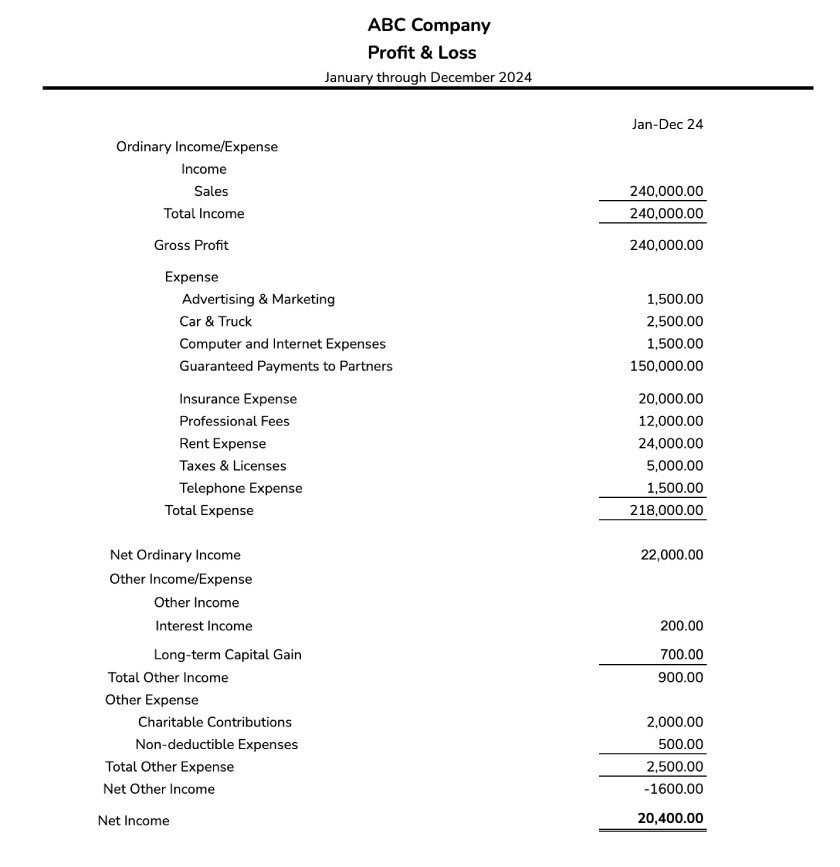

ABC Company’s P&L Statement

Step 1: Gather information needed to complete Form 1065

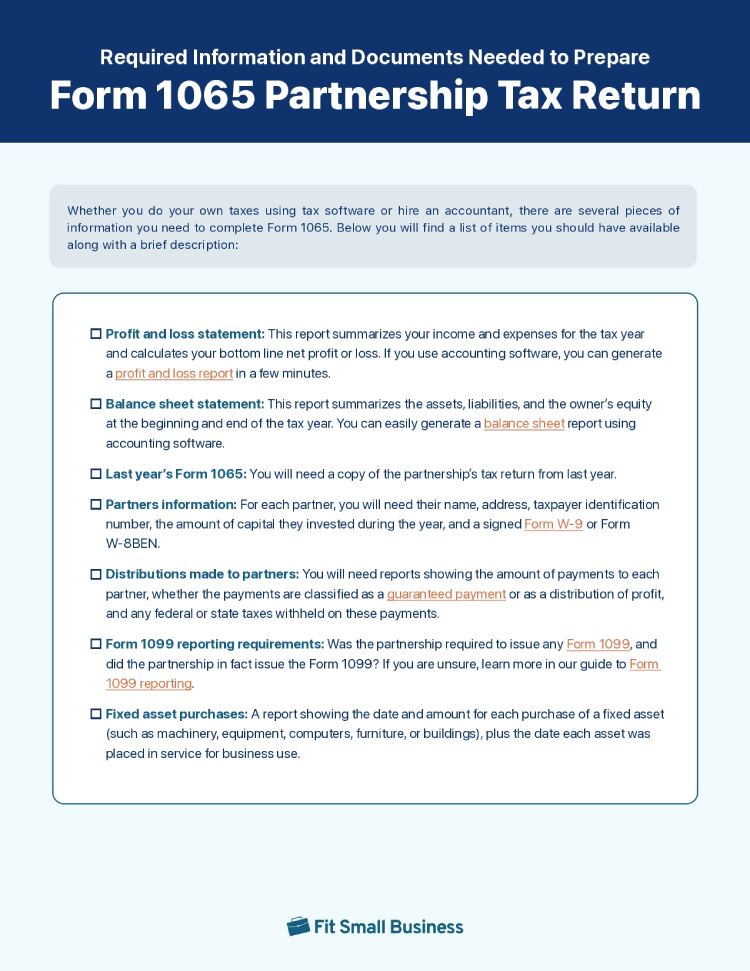

You’ll need financial statements for the tax year, information for each of the partners, and in-depth details about fixed assets and tax payments. Our free Form 1065 checklist linked above will help you in filling out your Form 1065.

The information and reports needed to prepare Form 1065 for a partnership include:

- P&L statement: This summarizes the partnership’s income and expenses for the tax year and calculates the bottom line net P&L.

- Balance sheet: This summarizes the assets, liabilities, and owner’s equity as of the end of the tax year.

- Prior year Form 1065: Refer to last year’s partnership return when preparing this year’s return.

- Employer identification number (EIN): This is your federal EIN, also known as a taxpayer identification number (TIN). If this is the first return for a new partnership, you’ll need to apply for one from the IRS before filing the partnership return. Our article on how to get an EIN will guide you.

- Business start date: Provide the date you started the business.

- Principal business activity code: This numeric code represents the principal line of business the partnership is engaged in. Select the code that best describes your partnership from the list provided in the IRS’s Form 1065 Instructions.

- Principal business activity: This is a short description of the nature of the partnership’s business activity. Examples include manufacturing, retail, food service, and professional services.

- Principal product or service: This is a short description of the primary product or service the partnership offers. Examples include toys, restaurants, and accounting.

- Accounting method: Cash or accrual are the most common accounting methods. For more details, check out our comparison of the cash vs accrual accounting method.

- Number of partners: This is the total number of partners in the business.

- Partners’ information: For each partner, you’ll need their name, address, TIN, the amount of capital they invested during the year, and a signed Form W-9 or Form W-8BEN.

- Distributions made to partners: You’ll need reports showing the amount of payments to each partner, whether those payments are classified as a guaranteed payment or as a distribution of profit, and any federal or state tax withheld on these payments.

- Form 1099 reporting requirements: You’ll need to know if the partnership is required to issue any Forms 1099 and whether the partnership issued them. For more details, check out our guide to Form 1099 reporting.

- Fixed asset purchases: You’ll need a report showing the date and amount for each purchase of a fixed asset, such as machinery, equipment, computers, furniture, or buildings. You’ll also need to know the date each asset was placed in service for business use.

- Fixed asset sales: If any fixed assets were sold during the period, you’ll need the date of sale, the sales proceeds, and a description of the asset(s) sold.

If you use an accounting program like QuickBooks, you can easily run P&L and balance sheet reports in a few minutes. Read our review of QuickBooks Online to learn about how the solution can help your business.

If you already use it but need guidance, check out our tutorials:

Step 2: Fill out general information

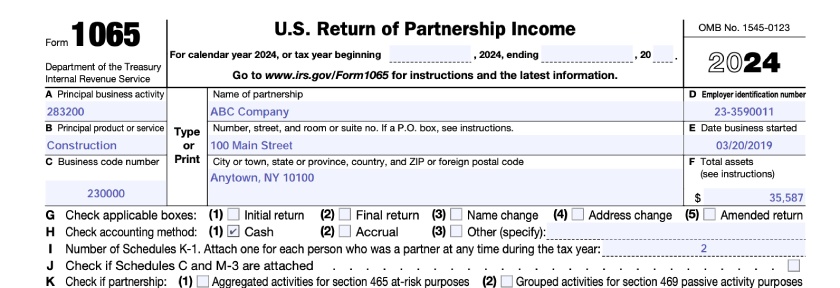

Now that you have financial statements and information about the partnership and the partners, let’s begin preparing the partnership tax return, starting at the top of Form 1065.

While it’s not recommended that you complete the form by hand (using tax software is preferred), you can download IRS Form 1065 if you’d like to see the form in its entirety. The top portion of Form 1065 asks for general information about the partnership, such as the name, address, and type of business the partnership operates.

Form 1065 General Information

Information that’s reported at the top of Form 1065 includes:

- Name of the partnership

- Address of the partnership

- Principal business activity and business code

- Federal EIN

- Date that the business started

- Accounting method

Step 3: Fill out income and deductions

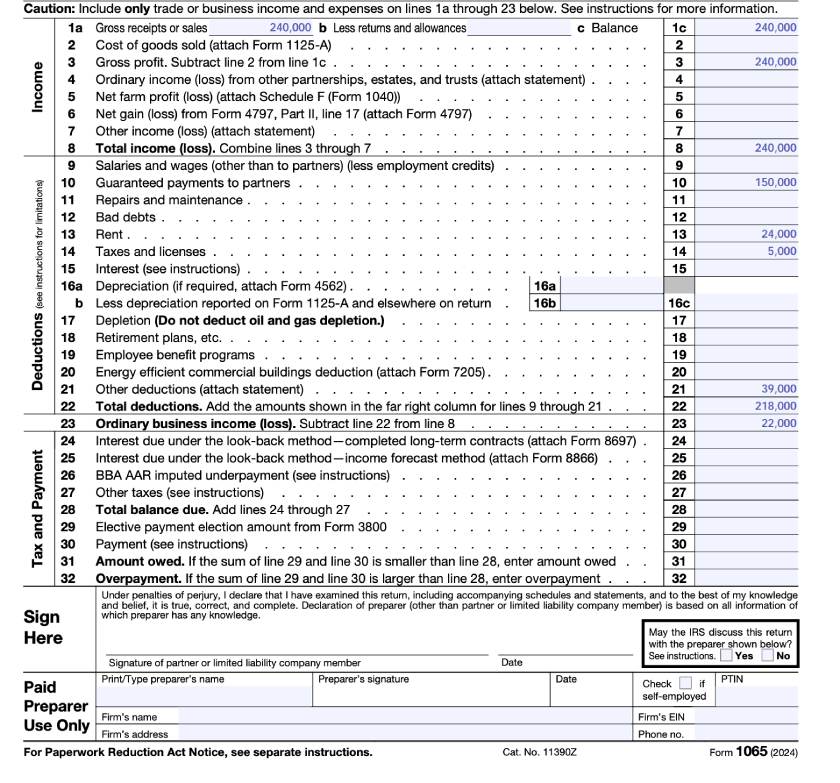

Page 1 of Form 1065 reports the business income and deductions of the partnership. Details about income and expenses will come from the partnership’s P&L statement.

Page 1 of Form 1065 includes only ordinary business income (or loss) and deductions, the net of which flows to Schedule K, line 1 of Form 1065 (Step 5). Dividends, interest, and rental income from investments should not be reported on Page 1 — they should be reported directly on Schedule K. Including them on both Page 1 and Schedule K would double-count them.

Special tax deductions, such as Section 179, are also shown directly on Schedule K instead of Page 1. Briefly skip ahead to step 5, and review the income and deductions included separately on Schedule K lines 2 through 13 to ensure you exclude them from Page 1.

Form 1065 Business Income & Expenses

Note: Guaranteed payments to partners (line 10) made in exchange for services are similar to a salary paid to the partner. However, since partners are not allowed to be employees of the partnership, they are instead contractually promised distributions in place of a salary. This compensation is referred to as a guaranteed payment, which appears in multiple places on the return.

While guaranteed payments are deducted for book purposes (as shown in the sample P&L statement above), they are not deductible for tax purposes. While they are deducted on Page 1, line 10, they are then added back to income as a separately stated item on Schedule K, line 4. In addition to being income, guaranteed payments must be shown as partnership distributions on Schedule K, line 19.

Step 4: Fill out Schedule B

Schedule B, found on Pages 2 through 4 of Form 1065, asks 31 questions that require yes or no responses. You may need to look at the instructions for Form 1065 because these questions are quite technical.

One of the most important questions on Schedule B is question #4. Your answer to this question will determine if you need to fill out Schedules L, M-1, and M-2, Item F on Page 1 of Form 1065, or Item L on Schedule K-1.

Let’s look at question #4 and see if it applies to our tax return:

Does the partnership satisfy all four of the following conditions? Yes/No

- The partnership’s total receipts for the tax year were less than $250,000.

- The partnership’s total assets at the end of the tax year were less than $1 million.

- K-1s are filed with the return and given to the partners on or before the deadline for the partnership return, including any extensions.

- The partnership isn’t filing and isn’t required to file Schedule M-3.

If “yes,” then the partnership isn’t required to complete Schedules L, M-1, and M-2; item F on Page 1 of Form 1065; or item L on Schedule K-1. Our sample corporation answers “yes” to this question, so we don’t need to file those schedules. However, many businesses choose to complete these sections anyway to demonstrate to the IRS that they keep complete books. For illustrative purposes, I’ve completed these schedules, as shown below.

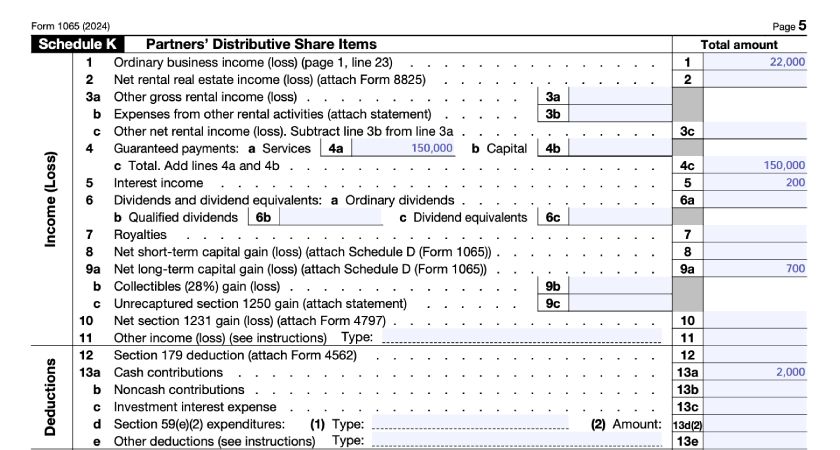

Step 5: Fill out Schedule K

The partnership’s income, deductions, and credits for the year are all listed on Schedule K. The amounts shown on Schedule K will be allocated to each partner using Schedule K-1. Each partner will get a Schedule K-1 so that they can report their share of the partnership’s income on their own tax returns.

Line 1 of Schedule K reports the ordinary business income or loss from Page 1. Lines 2 through 13 report other items of income and deductions as shown in the sample P&L statement. Be careful not to report any income or deduction on both Page 1 and lines 2 through 11 — except for guaranteed payments, which are a deduction on Page 1 and income on Schedule K, line 4.

Form 1065, Schedule K Income and Deductions

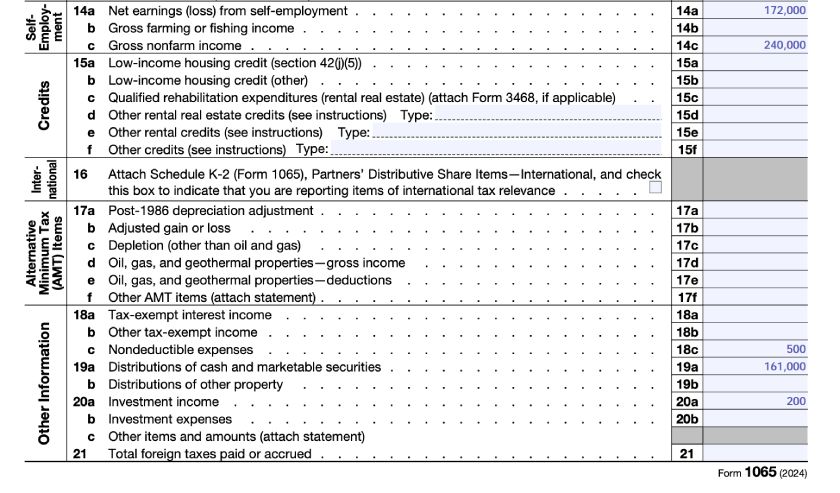

Lines 14 through 21 of Schedule K are for informational purposes and don’t affect the total taxable income reported by the partnership. Partners use this information to make certain tax calculations on their individual tax returns.

It’s fine for amounts on lines 14 through 21 to also be included on Page 1 or in the income and deduction section at the top of Schedule K. For example, foreign interest payments listed on line 16(i) should also be deducted as an interest expense on Page 1.

Here is how we calculated the numbers for our sample company:

- Line 14a, Net Earnings from self-employment, includes both the ordinary business income from line 1 and the guaranteed payments from line 4a.

- Line 14c, gross nonfarm income, is the total gross receipts from Page 1.

- Line 18c is the nondeductible expenses from the sample P&L statement.

- Line 19a is the 2025 increase in ownership distributions shown on our sample balance sheet plus the guaranteed payments to partners.

- Line 20a, investment income, is the interest income from line 5. Notice it does not include any capital gains shown on lines 8 or 9.

Form 1065, Schedule K, Lines 14 through 21

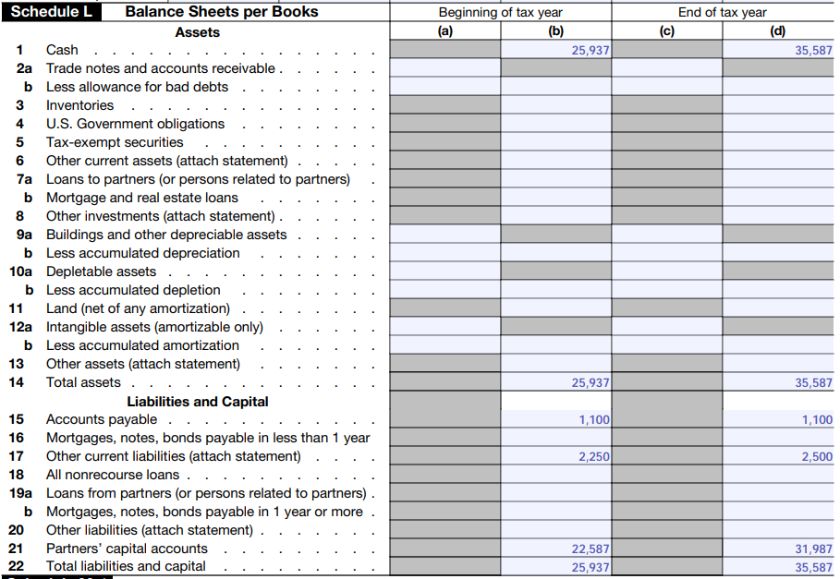

Step 6: Fill out Schedule L

Schedule L is used to give the IRS information about all of the partnership’s assets, debts, and equity at the beginning and end of the tax year. If you use an accounting program, this information will come directly from your balance sheet report.

Since our sample partnership meets all of the requirements of Schedule B, question 4, it’s unnecessary for the partnership to fill out Schedule L. However, we’ll complete Schedule L as it confirms all the income and deduction information has been entered and the return balances. The information for Schedule L comes directly from the sample balance sheet.

Form 1065, Schedule L Balance Sheet

Step 7: Complete analysis of net income (loss) per return

Lines 1 and 2 at the top of Page 5 summarize the income and loss shown on Schedule K. It then separates the income or loss by partner type. Our example partnership has all general, individual partners, so the entire income is shown on both line 1 and line 2a, column ii.

Form 1065, Page 6, Analysis of Net Income

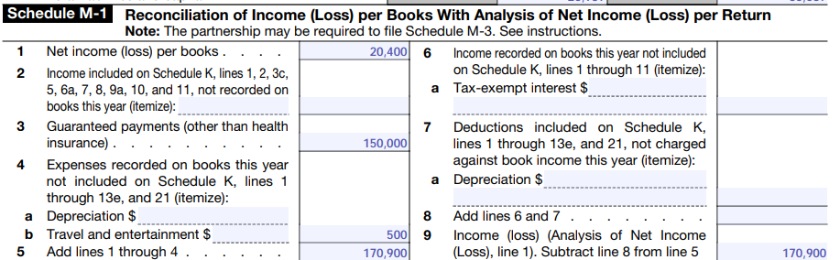

Step 8: Fill out Schedule M-1

Note: If you answered “Yes” to Schedule B, question 4, you don’t need to complete Schedule M-1.

The purpose of Schedule M-1 is to show any differences in how income and expenses are reported for bookkeeping and tax purposes. Any differences between the two methods are summarized on Schedule M-1.

Some common book-tax differences include:

- The adjustment for any nondeductible meals

- Guaranteed payments to partners

- Tax-exempt interest income

- Nondeductible expenses, such as fines, penalties, or entertainment

- Political contributions

- Differences between tax depreciation and book depreciation

The best way to tackle Schedule M-1 is to

- Review your P&L statement and enter the net income on Line 1 of Schedule M-1;

- Review the income and deductions you reported on Page 1 and Schedule K lines 2 through 13; and then

- Enter the net of those amounts on Schedule M-1, Line 9.

Compare the P&L statement and tax return income line-by-line to determine all differences. These differences must be shown on Schedule M-1, lines 2 through 9. For instance, if depreciation expense on the P&L statement is greater than depreciation expense on Page 1 of Form 1065, then the difference must be reported on Schedule M-1, line 4.

Even though our sample partnership meets all the requirements for Schedule B, question 4, and this schedule isn’t needed, we’ll still fill it out to show how important it is to keep track of all your income and expenses to gain a better understanding of your tax liability.

Form 1065, Schedule M-1

Step 9: Fill out Schedule M-2

The purpose of Schedule M-2 is to show changes to the partners’ capital account for the year and to calculate the ending balance. The beginning and ending capital account balance should agree to Schedule L. The cash distributions shown on Line 6 are the guaranteed payments to partners plus cash distributions as shown on Schedule K, line 19a.

Form 1065, Schedule M-2

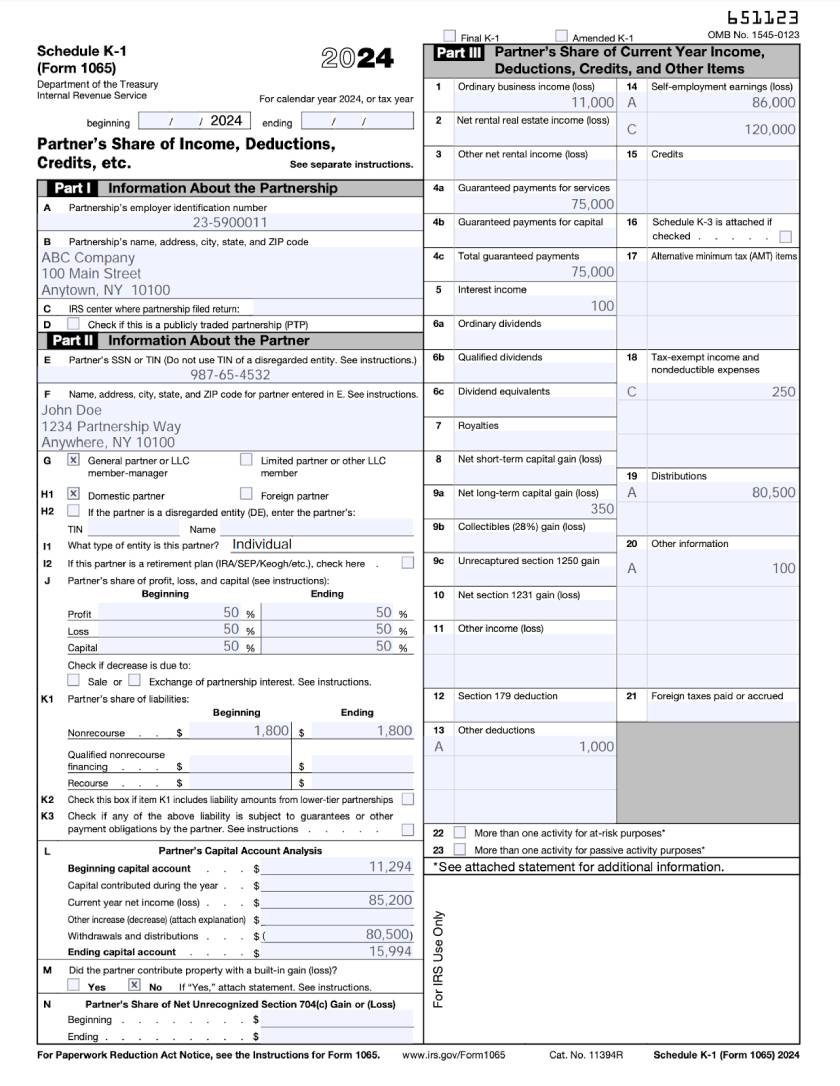

Step 10: Fill out Schedule K-1 for each partner

After filing Form 1065, each partner is provided a copy of their Schedule K-1 by the partnership. The K-1 reflects the partner’s share of income, deductions, credits, and other items that a partner will need to report on their individual tax return. The information you’ll need to fill out for each Schedule K-1 will come from Schedule K of Form 1065.

For ABC Company, we’ve assumed that each partner is allocated 50% of all income and deductions and that each was paid a guaranteed payment of $75,000. Below is the Schedule K-1 prepared for one of the 50% partners. If you answered “Yes” to question 4 on Schedule B, then you’re not required to complete box L.

Form 1065 Schedule K-1

Tips to help you prepare your Schedule K-1 include:

- Amounts should total to Schedule K. The amounts in Part III of Schedule K-1 are an allocation of amounts from Schedule K. Therefore, each line item totaled across all Schedule K-1s must equal the amount from Schedule K.

- Furnish Schedule K-1 by the due date. The partnership needs to distribute a Schedule K-1 to each partner by the filing deadline (March 15 — or September 15 with an extension.)

- Amounts flow from Schedule K-1 to Form 1040. Partners take the amounts shown on their Schedule K-1 and report them on their personal tax return.

This allocation process is how partnership income, deductions, and credits pass through to the partners’ personal tax returns.

Form 1065 partnership return due dates

The deadline to file Form 1065 is March 15 for calendar year partnerships. However, you can file IRS Form 7004 to get an extension to September 15.

Common mistakes made when completing Form 1065

When completing Form 1065, there are a few common errors that you should check for before finalizing your return.

Out-of-balance tax return

Just like a set of financial statements, a partnership return must balance. Here are a list of line items from your Form 1065 that must be equal for your return to balance.

- Page 1, line 23 must equal Schedule K, line 1

- Schedule L, line 14 must equal Schedule L, line 22 for the the beginning and end of the year

- Schedule M-1, Line 1 must equal the net income shown on your statement of profit or loss

- Schedule M-1, line 9 must equal Page 6, Analysis of Net Income (Loss) per Return, Line 1

- Schedule M-2, line 1 must equal Schedule L, line 21 for the beginning of the year

- Schedule M-2, line 9 must equal Schedule L, line 22 for the end of the year

- All lines on Schedule K must equal the same line summed across all Schedules K-1.

Improper allocation of partner percentages

Over time, the ownership percentages in a partnership may change. If those ownership percentages are not updated on the tax return, the wrong amount of income may be allocated to each partner.

The ownership percentages should agree with the allocation set forth in the partnership agreement (including any amendments). Allocation should be confirmed for profit, loss, capital, and recourse or nonrecourse debt.

Incomplete sections

While every section may not apply, the required ones should be completed to avoid rejection of the filing by the IRS. In addition, incomplete sections could result in improper treatment of tax items by partners. For example, if the preparer does not identify the activity as active or passive, the K-1 items may not be properly allocated by the partners.

Footnote omission

Box 20 of the Schedules K-1 issued from Form 1065 is used to provide supplemental information to the partners. For instance, details related to the Section 199A deduction would be included here. If that information were omitted by the Form 1065 preparer, each partner may not get the proper deduction.

Box 20 has a substantial amount of codes for a preparer to choose from to provide each partner with precise and accurate information on the operations of the business. Without relevant supplemental information, the partners may be unable to file accurate returns.

Frequently asked questions (FAQs)

If you formed an LLC or other business entity with the state, then you will need to file Form 1065. However, if you have a general partnership and both spouses own and operate the business, you may elect to file two Schedule Cs under the rules for qualified joint ventures. Learn more about Qualified Joint Ventures.

No. The partnership or LLC files one Form 1065, which tallies up income, deductions, and credits for the year. Then, it allocates the income, deductions, and credits to each partner using Schedule K-1. Each partner uses the information on their Schedule K-1 to prepare their own personal tax return.

Yes, LLCs and partnerships can have foreign partners, but foreign ownership comes with additional tax responsibilities. The LLC or partnership may need to withhold federal and state taxes on the income allocated to foreign partners. Most foreign partners need a US TIN and need to file their own tax returns in the US.

Yes, Form 1065 can be amended. Note that partnerships subject to the Bipartisan Budget Act (BBA) of 2015 must file an administrative adjustment request (AAR) instead of an amended return.

Bottom line

I recommend that Form 1065 be completed using tax software and, as a practice aid, use the PDF file of Form 1065 on the IRS’s website. While the preparation of a simple operational partnership may be straightforward, partnerships with many partners or complex asset holdings may warrant the use of a CPA. If you’re unsure about a required line item, it is also a good idea to consult the Form 1065 instructions on the IRS’s website.