U.S. Bank Merchant Services offers a full suite of payment solutions for small and midsize businesses, including in-person and mobile payments, POS systems, ecommerce tools, invoicing, and buy now, pay later options. Backed by U.S. Bank and powered by Elavon, it combines traditional merchant account pricing with modern payment features.

Unlike many bank processors, U.S. Bank publishes baseline transaction rates for merchants who apply online. These rates mainly apply to entry-level accounts, while most businesses are quoted custom pricing based on factors such as processing volume, industry, and the payment tools used. Additional fees for software, hardware, and account maintenance may also apply.

U.S. Bank Merchant Services is included in our list of the best merchant services and earned an updated expert score of 4.06 out of 5 for 2026, reflecting its strong feature set, broad payment support, and competitive options for established businesses.

In this review, we break down U.S. Bank Merchant Services pricing, POS and online payment options, payout timelines, and integrations to help you decide whether its bank-based pricing model is a better fit than flat-rate providers like Square or Stripe.

- U.S. Bank Merchant Services overview

- Is U.S. Bank Merchant Services right for you?

- U.S. Bank Merchant Services alternatives

- U.S. Bank Merchant Services pricing

- Payment types

- U.S. Bank Merchant Services features

- U.S. Bank Merchant Services ease of use and expert score

- U.S. Bank Merchant Services user reviews

- Frequently asked questions (FAQs)

- Bottom line

U.S. Bank Merchant Services overview

Deciding Factors

| Supported Business Types | FlexibleRetail, restaurants, professional services, healthcare, mobile businesses, automotive, B2B manufacturing, wholesale |

|---|---|

| Standout Features |

|

| Monthly Software Fees | $0-$99 per location |

| Setup and Installation Fees | $0–$99 |

| Contract Length | Month-to-month |

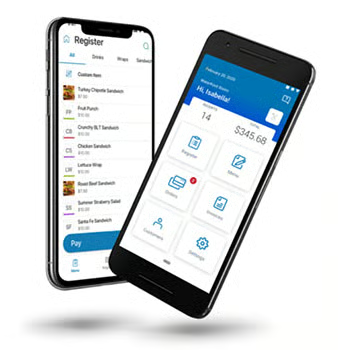

| Point-of-Sale Options | talech POS system, Oracle, Aloha, CenPOS, NRS, most payments-agnostic POS systems, and those operating on the Elavon network. Contact U.S. Bank for information on specific integrations |

| Payment Processing Fees |

|

| Customer Support |

|

Visit U.S. Bank Merchant Services

Is U.S. Bank Merchant Services right for you?

Many traditional merchant account providers focus primarily on large or enterprise-level businesses. While U.S. Bank is one of the largest financial institutions in the U.S., its merchant services offerings are flexible enough to support small and midsize businesses, particularly those that already bank with U.S. Bank.

U.S. Bank Merchant Services can integrate with a wide range of POS and business management systems. Merchants can work directly with a U.S. Bank representative to enable payment processing on many payment-agnostic POS systems or those operating on the Elavon network. U.S. Bank also offers native POS solutions, including mobile, smart terminal, and industry-specific systems, which may be easier to set up for businesses that prefer an all-in-one solution.

U.S. Bank Merchant Services is best for:

- Businesses with a U.S. Bank account: Merchants that use a U.S. Bank business checking account may qualify for faster funding, sometimes as soon as the same business day.

- Established small and midsize businesses: U.S. Bank Merchant Services is a good fit for businesses that want a traditional merchant account with in-person and online payment options and are comfortable with custom pricing.

- Businesses that need industry-specific POS options: Retailers, restaurants, and service-based businesses can choose from POS systems designed for their specific workflows, rather than relying on a one-size-fits-all solution.

U.S. Bank is not ideal for:

- Startups or microbusinesses seeking instant setup: Businesses seeking immediate approval, simple onboarding, and flat-rate pricing may find fintech providers such as Square or PayPal easier to use.

- Merchants that want fully transparent, self-serve pricing: Because pricing and add-on features often require a consultation, U.S. Bank Merchant Services is less suited for businesses that prefer to see all costs upfront.

- High-risk merchants: U.S. Bank Merchant Services does not support most high-risk industries. Businesses in these categories should consider dedicated high-risk merchant account providers.

U.S. Bank Merchant Services alternatives

| Best for | Monthly Fee From | |

|---|---|---|

| Traditional merchant account with better integration options | $0 |

| Visit Chase | ||

| New and small businesses, free POS | $0 |

| Visit Square | ||

| Low rates: interchange-plus pricing with no monthly fee | $0 |

| Visit Helcim | ||

Are you looking for the lowest rates? Leading merchant service providers offer custom payment processing rates based on your business size, type, and average order value. To find the most affordable option for you and compare multiple processing rates, read our guide on the cheapest credit card processing companies.

U.S. Bank Merchant Services pricing

3.38 / 5

U.S. Bank Merchant Services follows a traditional merchant account pricing model. While it publishes baseline transaction rates for online applicants, many merchants are ultimately quoted custom pricing based on business type, processing volume, and the POS system selected. This structure is similar to other bank-backed processors, such as Chase Payment Solutions, and differs from flat-rate providers like Square.

U.S. Bank does not require long-term contracts and generally offers month-to-month service, which we view as a positive. However, total costs can increase as merchants add POS software, additional devices, or advanced features, which reduced its overall pricing score.

Plans and monthly fees

U.S. Bank Merchant Services offers several POS software tiers. Availability and features depend on the business type and POS solution selected.

| Plan | Best For | Monthly Fee | Setup Fee |

|---|---|---|---|

| Mobile / Entry-Level | Mobile businesses and basic payment acceptance | $0 | $0 |

| Starter | Small retail or service businesses | $29 | Up to $99 |

| Standard | Growing retail or restaurant businesses | $69 | $99 |

| Premium | High-volume or multi-location businesses | $99 | $99 |

Plan features typically scale with price and may include higher product limits, reporting tools, employee management, and industry-specific POS functionality. Entry-level plans are limited and may not support advanced inventory, reporting, or integrations.

Payment processing

For merchants who apply online, U.S. Bank lists the following baseline transaction rates:

- In-person transactions: 2.6% + 10 cents

- Online transactions: 2.9% + 30 cents

- Keyed-in transactions: 3.5% + 15 cents

These rates are competitive with other major processors and comparable to Square’s standard pricing. However, they do not include additional account, software, or hardware-related fees. Custom pricing, including interchange-plus models, may be available for higher-volume or established businesses.

U.S. Bank also offers rate review and “meet or beat” pricing for merchants switching from another processor, though final rates depend on underwriting and account setup.

Additional and ongoing fees

Depending on the setup, merchants may incur additional charges, including:

- POS software fees: $0 to $99 per month for additional software license

- Setup and onboarding fees: Up to $99

- Additional device or terminal fees: Often around $29 per device per month

- Online ordering tools: May require a paid add-on

- Advanced reporting or industry features: Often included only in higher-tier plans

Some services, such as faster funding and certain ACH options, are available only to merchants with a U.S. Bank business checking account. Its basic checking account requires a minimum deposit of $100 and zero monthly maintenance fee. This is a huge advantage over Chase Payment Solutions, where a $2,000 minimum balance is required.

Hardware costs

U.S. Bank Merchant Services offers mobile card readers, smart terminals, and full countertop POS setups. Hardware may be rented monthly or purchased outright, depending on the device.

Rental agreements usually require:

- A monthly hardware fee

- Return of equipment upon cancellation

- Optional insurance or damage protection fees

Because hardware pricing and availability can change, merchants must confirm current costs during the application or consultation process.

Ingenico Moby/5500 card reader

|  |

|---|---|

Newland N910 terminal card reader

|  |

talech Register

|  |

Setup and application

U.S. Bank Merchant Services offers a partially self-service application process. Merchants can start online, particularly for basic payment setups, by submitting business and banking information for review. Applications are subject to underwriting, and approval timelines vary based on business type, risk level, and the payment solutions requested.

For simple mobile or entry-level payment acceptance, setup can be relatively quick once the account is approved. Merchants will need to configure their POS software or mobile app and connect compatible hardware before processing payments. More advanced setups, such as full POS systems, industry-specific solutions, or third-party integrations, typically require assistance from a U.S. Bank representative.

Assisted onboarding may involve a one-time setup fee, depending on the POS system and level of support required. Merchants using advanced POS features or custom integrations should expect a guided setup process rather than a fully self-serve experience.

While U.S. Bank supports multiple POS systems beyond its native options, confirming compatibility with a preferred POS or business management solution usually requires a phone consultation. This consultation helps ensure the selected software, hardware, and integrations work correctly with U.S. Bank’s payment processing services.

Contract and terms of service

U.S. Bank Merchant Services does not require any long-term contracts, even if you are renting the equipment instead of purchasing outright. All plans are on a month-to-month basis, and there are no cancellation fees.

Because of the wide customization options, the terms of service (TOS) will depend on your preferred POS system. If you choose to use talech, you will receive a separate talech TOS on top of the U.S. Bank payments TOS.

Visit U.S. Bank Merchant Services

Payment types

4.75 / 5

U.S. Bank Merchant Services supports all major payment types used by small and midsize businesses, including in-person, mobile, online, invoicing, and alternative payment methods. While coverage is broad, some features require specific POS solutions, add-on software, or higher-tier plans, which can increase monthly costs and prevent U.S. Bank from earning a perfect score in this category.

Mobile payments

U.S. Bank Merchant Services supports mobile payment processing through its mobile POS and smart terminal solutions. Businesses can accept payments using a smartphone or tablet paired with a compatible card reader, as well as through dedicated mobile terminals.

Supported payment methods typically include:

- Credit and debit cards

- Contactless payments

- Apple Pay and Google Pay

Depending on the setup, merchants can accept payments by manually entering card details, using a mobile card reader, or processing tap-to-pay transactions. Mobile payment features and hardware availability vary by POS solution and plan.

Ecommerce and online payments

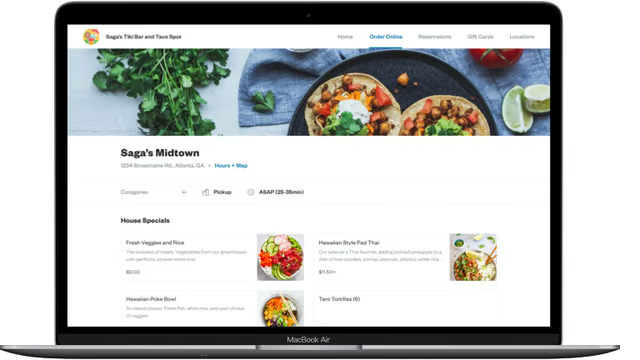

U.S. Bank Merchant Services offers several options for accepting online payments. These include hosted checkout pages, online ordering tools, and ecommerce integrations supported through the Elavon payment gateway.

Online ordering tools are often bundled with higher-tier POS plans or offered as paid add-ons for lower-tier plans. While suitable for restaurants and businesses offering pickup or delivery, these tools may be limited compared to standalone ecommerce platforms. Businesses that require more advanced customization or integrations may need to use third-party ecommerce software compatible with the Elavon network.

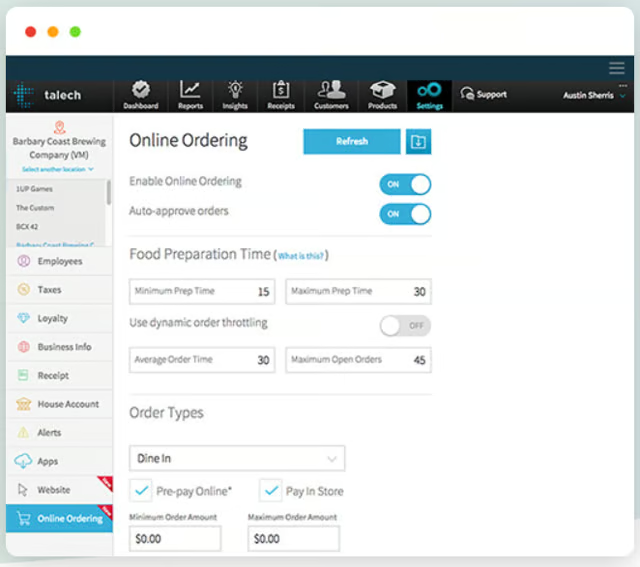

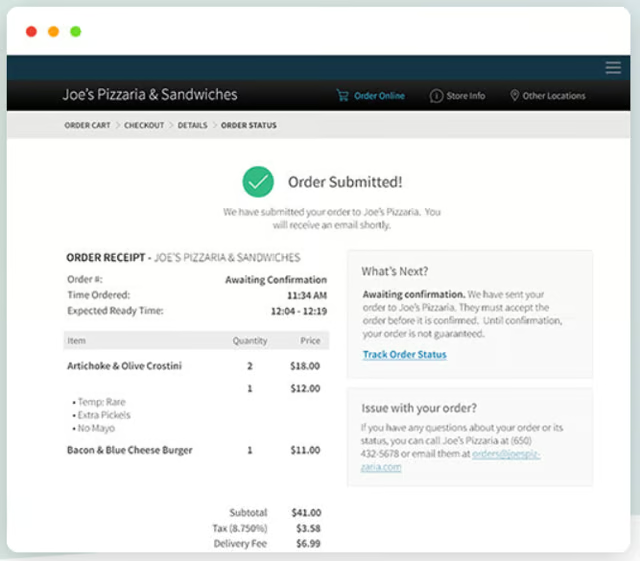

The talech Online Ordering allows customers to create a branded website for online selling and order management. (Source: U.S. Bank Merchant Services)

The website can be customized with your business colors and images. (Source: talech)

The Online Ordering system is best for food-service businesses. (Source: talech)

The online ordering system allows you to take and manage orders. (Source: talech)

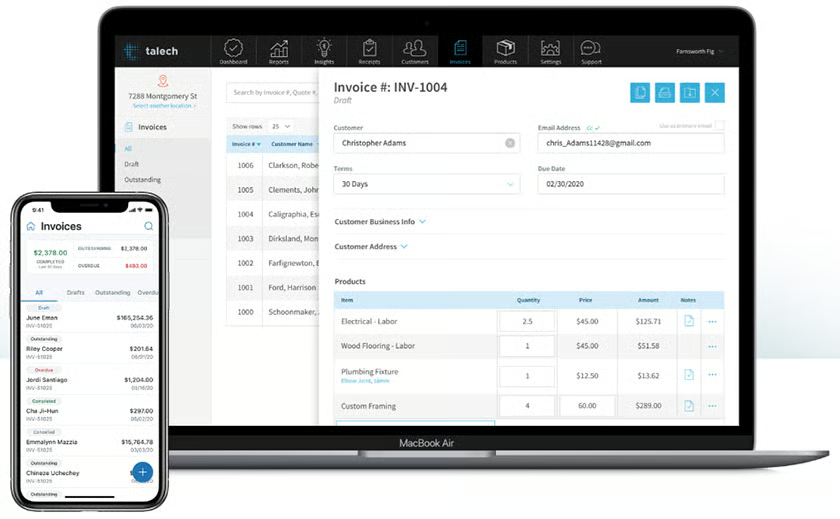

Invoicing

U.S. Bank Merchant Services includes invoicing capabilities through its supported POS and payment software. Merchants can create, send, and track invoices electronically, with the ability to email invoices to customers and monitor payment status.

Some setups allow for automated reminders and basic invoice management, making invoicing a useful option for service-based businesses. Feature availability depends on the POS system and plan selected.

ACH and bank transfers

ACH payments are not included directly with U.S. Bank Merchant Services plans. Instead, ACH functionality is available through U.S. Bank’s cash management and treasury services, specifically SinglePoint Essentials, which is offered as part of U.S. Bank’s business banking products.

Through SinglePoint Essentials, businesses can send and receive ACH payments for use cases such as customer billing, vendor payments, payroll, and recurring transactions. Supported features include ACH credits and debits, scheduled and recurring payments, and same-day ACH for eligible transactions. These services are accessed through U.S. Bank’s online banking and cash management platform, rather than through POS software or the merchant services dashboard.

ACH services through SinglePoint Essentials involve separate fees billed at the banking level. Based on U.S. Bank’s current business pricing disclosures, costs may include a monthly cash management access fee, per-item ACH transaction fees, and additional charges for same-day ACH. Pricing and availability vary by business checking account type and transaction volume.

In addition to ACH, U.S. Bank business customers can use Zelle for Business to send and receive bank-to-bank payments. Zelle transactions are typically fast and can be completed within minutes, but they are limited to customers who also use the Zelle network. Zelle is best suited for one-off payments and small-dollar transfers rather than automated billing or recurring payments.

Overall, U.S. Bank offers strong ACH and bank transfer capabilities for businesses that already bank with U.S. Bank. However, because these tools are handled separately from merchant services, they should be viewed as complementary banking solutions rather than built-in payment types within U.S. Bank Merchant Services.

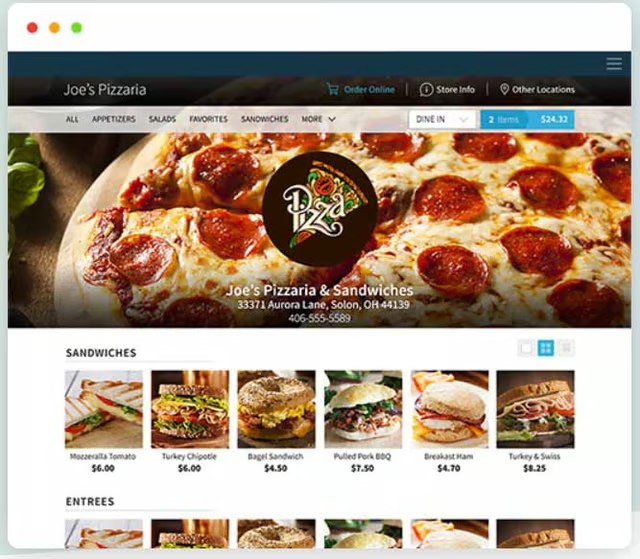

POS system and virtual terminal

U.S. Bank Merchant Services places a strong emphasis on POS-based payment solutions. Rather than offering a single proprietary system, U.S. Bank supports multiple POS options, including mobile POS apps, smart terminals, and full countertop systems designed for retail, restaurant, and service-based businesses.

Merchants can accept in-person payments, print receipts, track inventory, manage customers, and access basic reporting tools depending on the POS solution and software tier selected. Entry-level setups are suitable for mobile or low-volume businesses, while more advanced POS features, such as detailed inventory management and employee tools, are available through higher-tier plans or industry-specific systems.

Most U.S.-Bank-supported POS solutions also include virtual terminal functionality, allowing merchants to manually enter a customer’s card details to process payments when cards are not physically present. This is useful for phone orders, back-office transactions, or situations where a card reader is unavailable.

Paper checks

U.S. Bank supports check payments through Remote Deposit Capture (RDC), which allows businesses to deposit checks by taking photos through a compatible device or banking app. Funds may be available the same business day, depending on the account type and deposit time.

While RDC is a banking feature rather than a core merchant service, it adds flexibility for businesses that still accept paper checks.

U.S. Bank Merchant Services features

4.06 / 5

U.S. Bank Merchant Services scores well for its breadth of features, particularly for businesses that want payment processing backed by a large bank. Standout strengths include faster funding for U.S. Bank customers, strong customer support availability, and access to a wide ecosystem of POS solutions and business services.

However, some advanced features and integrations require add-on services or separate banking products, which affects overall value and transparency.

Integrations

U.S. Bank Merchant Services supports integrations through the Elavon payment network and compatible POS systems rather than offering a single, open marketplace. Ecommerce platforms such as Shopify and Wix are supported through approved gateways and integrations, while shopping carts and gateways like Authorize.net and NMI can be used depending on the merchant’s setup.

POS-based integrations vary by solution. Businesses using U.S. Bank-supported POS systems can access integrations for accounting, employee management, and operational tools. Accounting integrations commonly include QuickBooks, Xero, and Sage, while restaurant and retail systems may support hardware and operational integrations such as receipt printers, barcode scanners, and kitchen display systems.

U.S. Bank payment processing can also be used with select third-party and industry-specific POS systems, including solutions for restaurants, automotive businesses, healthcare providers, and B2B or wholesale merchants. Because integration availability depends on the POS platform and business type, merchants typically need to consult with a U.S. Bank representative to confirm compatibility.

Fraud protection and security

U.S. Bank Merchant Services offers a range of security and risk management tools designed to help businesses reduce fraud and manage compliance. These may include PCI compliance support, fraud monitoring, chargeback management tools, and risk controls for card-not-present transactions.

Additional security services, such as advanced fraud tools or ACH risk controls, are generally offered through U.S. Bank’s banking or treasury products and may involve extra fees. Availability and pricing depend on the merchant’s account structure and payment methods used.

Offline processing

Some U.S.-Bank-supported POS solutions offer offline or store-and-forward capabilities, allowing merchants to continue accepting transactions during temporary internet outages. Transactions are processed once connectivity is restored.

Offline processing is most commonly available on select mobile POS apps and smart terminals, and functionality varies by device and POS software. Not all transactions or payment types are guaranteed to be approved offline, so this feature works best as a short-term backup rather than a primary processing method.

Surcharging and cost recovery tools

U.S. Bank Merchant Services supports credit card surcharging for eligible merchants operating in states where surcharging is permitted. This allows businesses to pass on credit card processing costs to customers, subject to card network rules and local regulations.

Surcharging setup and compliance requirements vary, and merchants should confirm eligibility and configuration details with U.S. Bank before enabling this feature.

Funding speed

U.S. Bank Merchant Services offers faster funding options for businesses that also maintain a U.S. Bank business checking account. Eligible merchants may receive funds as soon as the same business day, depending on transaction timing and account setup.

This faster funding option is generally included for U.S. Bank customers, while merchants without a U.S. Bank account may experience standard payout timelines.

Customer support

U.S. Bank Merchant Services provides 24/7 customer support via phone, with additional support available through email, online resources, and in-branch assistance. Merchants can access an online knowledge base and schedule appointments with representatives as needed.

Larger or more established businesses may also receive dedicated account management, which can be helpful for setup, troubleshooting, and ongoing account reviews.

U.S. Bank Merchant Services ease of use and expert score

4.06 / 5

U.S. Bank Merchant Services earned an above-average score for ease of use, driven largely by its reliable customer support, flexible POS options, and lack of long-term contracts. Merchants can begin the application process online for basic payment setups, and U.S. Bank offers 24/7 phone support, which is a notable advantage compared with many fintech-based processors that limit live assistance.

Setup simplicity depends on the type of solution selected. Entry-level payment processing can be relatively straightforward, while businesses that require advanced POS systems, integrations, or industry-specific tools typically need to speak with a U.S. Bank representative. This consultation-based approach can be helpful for complex setups but may slow onboarding for merchants who prefer a fully self-service experience.

We also gave U.S. Bank credit for offering month-to-month service and avoiding early termination fees, even when hardware is rented rather than purchased outright. While we generally caution against hardware rentals, U.S. Bank’s equipment agreements are more flexible than those of many traditional merchant account providers and do not lock merchants into long-term contracts.

On the downside, U.S. Bank Merchant Services lacks transparency in certain areas. Integration options, add-on features, and total costs are not fully disclosed online, which can make it difficult for merchants to evaluate the service without a phone consultation. In addition, while U.S. Bank is a well-established institution, there are relatively few user reviews that focus specifically on its merchant services offering rather than its banking products.

Overall, U.S. Bank Merchant Services performs well for established small and midsize businesses that value support, stability, and bank-backed infrastructure. It offers a lower barrier to entry than many traditional merchant accounts, but businesses that want advanced features should expect additional monthly, setup, or device-related fees. These trade-offs ultimately kept U.S. Bank from earning a higher ease-of-use score, but it remains a solid option for merchants comfortable with a more guided onboarding process.

U.S. Bank Merchant Services user reviews

There are limited online reviews that focus specifically on U.S. Bank Merchant Services. Most public feedback about U.S. Bank centers on its banking products, making it difficult to isolate merchant services-related experiences.

To add context, we also reviewed feedback for talech, its POS software provider, and Elavon, the underlying payment processor. Negative talech reviews commonly mention technical issues with the POS system and inconsistent support, while Elavon reviews often cite billing concerns, such as unexpected fees or account holds. These complaints are typical of traditional merchant account providers and may vary depending on the merchant’s setup.

User Review Snapshot

- U.S. Bank (Trustpilot): 1.3 out of 5 stars from 1,300+ reviews (mostly banking-related)

- talech (Trustpilot): 1.2 out of 5 stars from 100+ reviews

- Elavon (Trustpilot): 4.2 out of 5 stars from 500+ reviews

Overall, the lack of merchant services–specific reviews makes it difficult to draw firm conclusions from user feedback alone. Merchants should clarify pricing, support expectations, and setup details during onboarding to avoid surprises.

Methodology

Frequently asked questions (FAQs)

Click through the sections below to read answers to common questions about U.S. Bank Merchant Services:

Does U.S. Bank offer merchant services?

Yes, U.S. Bank offers merchant services to businesses of all sizes, in addition to its checking, credit card, and other business banking solutions.

What POS system does U.S. Bank use?

U.S. Bank owns a cloud-based POS system, talech, that supports POS services to merchants by default. However, you can speak with a U.S. Bank Merchant Services representative if you need a different solution or have a particular business solution in mind.

What is Elavon?

Elavon is a payment processor and provides payment processing services to U.S. Bank. However, note that there are other payment gateways and processors that can integrate with U.S. Bank Merchant Services.

Does U.S. Bank offer same-day funding?

Yes, eligible merchants, especially those with a U.S. Bank business checking account, may receive funds as soon as the same business day. Availability depends on account setup and transaction timing.

Does U.S. Bank Merchant Services support ACH payments?

ACH payments are not included with U.S. Bank Merchant Services plans. Businesses can send and receive ACH payments through separate U.S. Bank banking and cash management products, which require additional setup and fees.

Bottom line

U.S. Bank Merchant Services is a bank-backed payment processor that offers a wide range of in-person and online payment solutions, along with industry-specific POS options and fast funding for eligible U.S. Bank customers. It can be a good fit for established small and midsize businesses that want traditional merchant account pricing, flexible POS setups, and reliable support.

While U.S. Bank does offer low-cost entry options for basic payment acceptance, most businesses should expect additional monthly, setup, or device fees as they scale or add features. Businesses that prefer fully transparent, flat-rate pricing and instant self-service setup may find fintech providers like Square or Stripe easier to use.