Helcim is my top pick for the best merchant services provider because it offers transparent interchange-plus pricing, no monthly fee, automatic volume discounts, and tools for accepting in-person, online, invoice, and recurring payments.

The best merchant services provider should help your business accept payments securely, keep processing costs manageable, and get paid without locking you into unnecessary fees or long-term contracts. The right choice depends on how you sell, your monthly sales volume, average ticket size, payment types, hardware needs, and whether you need POS, invoicing, ecommerce, or recurring billing tools.

For this guide, I compared merchant services providers based on pricing, contract terms, payment types, funding speed, chargeback fees, hardware, POS tools, integrations, customer support, and overall value for small businesses.

| Best for | Monthly Fee | |

|---|---|---|

| Helcim | Lowest processing fees | $0 (with POS) |

| Square | Startups needing POS and payments | $0-$149 (with POS) |

| Payment Depot | Growing businesses needing custom rates | $0 |

| Chase Payment Solutions | Direct bank processing | $0 (with POS) |

| GoDaddy Payments | GoDaddy ecommerce sellers | $0 |

| U.S. Bank Merchant Services | Fast funding and bank-backed processing | $0-$99 |

| Stax | High-volume businesses | $99-$199 |

| PaymentCloud | High-risk businesses | $10-$45 |

| Stripe | Custom online payments | $0 |

| PayPal | PayPal checkout and flexible payments | $0-$30 (with POS) |

- Best merchant services compared

- Compare merchant services costs with our payment processing calculator

- How I chose the best merchant services for small businesses

- Helcim: Best for lowest credit card processing fees

- Square: Best all-in-one POS and payment processing

- Payment Depot: Best for growing businesses

- Chase Payment Solutions: Best for direct bank processing

- Chase Merchant Services

- GoDaddy Payments: Best for GoDaddy ecommerce sellers

- U.S. Bank Merchant Services: Best for fast funding

- US Bank Merchant Services

- Stax: Best for high-volume businesses

- PaymentCloud: Best for high-risk businesses

- Stripe: Best for customizable online payments

- PayPal: Best for flexible checkout options

- How to choose the best merchant services for your business

- Merchant services vs merchant account vs payment processor

- How do I apply for a merchant account?

- Frequently asked questions (FAQs)

- Bottom line

Best merchant services compared

| My Score (out of 5) | Pricing model | Swipe/Chip Transaction | Chargeback Fee | |

|---|---|---|---|---|

| Helcim | 4.51 | Interchange-plus | From interchange + 0.15% + 6 cents | $15 refundable |

| Square | 4.49 | Flat-rate | 2.6% + 15 cents | Waived up to $250/month |

| Payment Depot | 4.43 | Custom/interchange-plus | Custom quote (Interchange + 0.2%-1.95%) | $25 |

| Chase Payment Solutions | 4.14 | Flat-rate or custom | 2.6% + 10 cents | $25 |

| GoDaddy Payments | 4.13 | Flat-rate | 2.3% | $15 |

| U.S. Bank Merchant Services | 4.06 | Flat-rate or custom | 2.6% + 10 cents | $35 |

| Stax | 4.04 | Membership pricing | Interchange + 8 cents | $25 |

| PaymentCloud | 3.97 | High-risk/custom | 2%-3.5% | $25-$45 |

| Stripe | 3.96 | Flat-rate/custom | 2.7% + 5 cents | $15 refundable |

| PayPal | 3.93 | Flat-rate | 2.29% + 9 cents | $20 |

Compare merchant services costs with our payment processing calculator

Use the calculator below before choosing a merchant services provider. The lowest published rate is not always the lowest total cost once you factor in monthly fees, online transactions, chargebacks, and average ticket size.

Best Merchant Services Calculator

| Provider | Monthly Cost | Effective Rate |

|---|---|---|

| Square | ||

| Helcim | ||

| Chase | ||

| Payment Depot | ||

| Stax | $99 | |

| QuickBooks | ||

| Stripe | ||

| PayPal | ||

| PaymentCloud | Custom | Custom |

| U.S. Bank Merchant Services - Mobile plan | $0 | |

| U.S. Bank Merchant Services - Starter plan | $29 | |

| U.S. Bank Merchant Services - Standard plan | $69 |

How I chose the best merchant services for small businesses

To evaluate the best merchant services, I fact-checked each provider to ensure that pricing and features were accurate. I then scored each one on 23 data points, prioritizing value for money and ease of use. See my full methodology below.

Why you can trust Fit Small Business

Helcim: Best for lowest credit card processing fees

Why I chose Helcim

When I evaluated merchant services providers for this guide, Helcim stood out for its transparent interchange-plus pricing and built-in cost optimization tools. Unlike flat-rate processors, Helcim charges interchange plus a small markup and does not require a monthly subscription, which can reduce processing costs for businesses with consistent transaction volume.

Helcim also includes several payment tools at no extra cost, including POS software, invoicing, subscription billing, and an online payment gateway. The platform automatically applies volume discounts as your processing grows and can capture Level 2 and Level 3 data for eligible B2B transactions to help qualify for lower interchange rates. Helcim also offers Fee Saver, a program that allows merchants to pass credit card processing fees to customers through surcharging or convenience fees.

Because Helcim provides a traditional merchant account, businesses must complete an application and underwriting process before approval. While this requires more setup than payment facilitators like Square, it typically results in more stable accounts and lower long-term processing costs.

Read our guide to merchant accounts to learn more about dedicated or traditional merchant accounts (like Helcim) vs payment facilitators (like Square).

Who should use Helcim

Helcim is best for established businesses that want to minimize credit card processing costs with transparent interchange-plus pricing. It also works well for B2B companies, wholesalers, and professional services that benefit from Level 2 and Level 3 processing.

Helcim pricing

- Monthly fee: $0

- Card-present transaction fee: From interchange plus 0.15% + 6 cents

- Card-not-present transaction fee: From interchange plus 0.15% + 15 cents

- American Express transaction fee: 0.10% + 10 cents

- Tap-to-pay on iPhone: + 10 cents per transaction

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $15 per lost dispute

- Card readers: $199

- POS terminal: $349 or $32/month for 12 months

Helcim also has a free credit card processing program called Helcim Fee Saver, which allows merchants to pass processing fees over to customers via a surcharge or convenience fee.

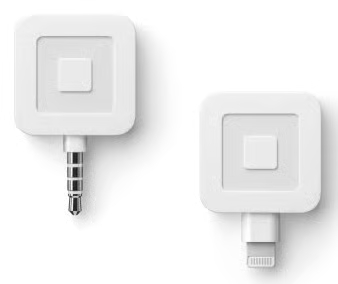

Helcim hardware

| Card Reader | Smart Terminal |

|---|---|

|  |

| $199 | $349 or $32 per month for 12 months |

| Tap, Chip & PIN transactions | Standalone device with built-in POS app, tap, chip, and PIN-enabled transactions |

| Buy Helcim Card Reader | Buy Helcim Smart Terminal |

Standout features

- Automated volume discounts: Helcim automatically lowers your processing markup as your monthly transaction volume increases. Unlike many providers that require negotiating better rates, Helcim applies these discounts automatically as your business grows.

- Transparent pricing structure: Helcim combines interchange-plus pricing with no monthly subscription fee and refundable chargeback fees. This transparent pricing model can result in lower effective processing costs compared with flat-rate processors.

- Free credit card processing: Helcim’s Fee Saver feature allows merchants to pass credit card processing fees to customers through surcharging or convenience fees. This option can significantly reduce or eliminate processing costs for businesses that choose to shift those fees to card payments instead of cash or ACH transactions.

- Built-in payment tools: Helcim includes POS software, invoicing, subscription billing, CRM tools, and an online payment gateway at no additional cost, features many processors charge extra for.

- Level 2 and Level 3 processing: Helcim can automatically capture the additional transaction data required for Level 2 and Level 3 B2B transactions, helping eligible businesses qualify for lower interchange rates.

Related reading:

Square: Best all-in-one POS and payment processing

Why I chose Square

In my evaluation of merchant services providers for this guide, Square stood out for its simplicity, accessibility, and all-in-one business tools. Unlike traditional merchant account providers, Square operates as a payment facilitator, which means businesses can sign up and start accepting payments without going through a lengthy underwriting process.

Square includes POS software, payment processing, ecommerce tools, invoicing, and mobile payment capabilities in a single platform. Businesses can accept payments in person, online, through invoices, virtual terminals, and even QR codes without needing additional integrations or third-party software.

While Square’s flat-rate pricing is typically higher than interchange-plus providers like Helcim, the platform’s free software, simple setup, and lack of monthly fees make it one of the most cost-effective options for small businesses and startups.

Square also leads our list of the best free POS software, free merchant accounts, and retail credit card processors.

Who should use Square:

Square is best for new and small businesses that want an easy way to start accepting payments with minimal upfront costs. Its free POS software, simple flat-rate pricing, and quick signup process make it one of the easiest merchant services platforms to launch with.

Square pricing

- Monthly fee: $0 to $149

- Card-present transaction fee: 2.6% + 15 cents

- Ecommerce and invoice transaction fee: 2.9% + 30 cents

- Card-not-present transaction fee: 3.5% + 15 cents

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: Waived up to $250 per month for chargeback protection

- Card reader: $59

Square hardware

| Magstripe Reader | Contactless and Chip Reader | Square Terminal | Square Handheld |

|---|---|---|---|

|  |  |  |

| First free, additional $10 | $59 | $299 or $27 per month for 12 months | $399 or $37 per month for 12 months |

| Accepts payments via magstripe (swiped), available in jack or lightning connector. | Bluetooth reader that accepts EMV (chip), and near-field communications (NFC), such as Apple Pay and Google Pay payments. Optional countertop dock and phone case mount. | Stand-alone mobile POS that can take orders, accept card payments, and issue receipts with built-in printer. | Portable POS device with built-in barcode scanner that accepts tap, chip, and mobile wallet payments. |

| Buy Magstripe Reader | Buy Contactless Reader | Buy Square Terminal | Buy Square Handheld |

Related: Square Hardware Comparison: Which Square POS Device Is Best for Your Business?

Standout features

- Free POS software and business tools: Square’s free plan includes POS software, inventory tracking, reporting, invoicing, ecommerce tools, and customer management features, allowing small businesses to run their operations without additional software subscriptions.

- Multiple payment methods: Square supports in-person payments, online checkouts, invoices, manually keyed transactions, ACH bank transfers, recurring billing, and buy now, pay later (BNPL) options, giving businesses flexibility in how they accept payments.

- Chargeback protection: Square waives up to $250 per month in chargeback dispute fees, which is a generous policy compared with many traditional merchant services providers.

- Affordable hardware ecosystem: Square offers a range of hardware options for different business sizes, including mobile card readers, countertop terminals, and full POS registers. New merchants also receive a free card reader when they sign up.

- CBD payment program: Square supports online sales of hemp and hemp-derived CBD products through its specialized CBD program, which is uncommon among mainstream payment processors.

Related reading:

Payment Depot: Best for growing businesses

Why I chose Payment Depot

Payment Depot stood out for its customizable pricing and strong integration capabilities. Like Helcim, it uses an interchange-plus pricing model that can reduce processing costs compared with flat-rate processors.

Payment Depot supports a wide range of payment options, including in-person payments, ecommerce checkouts, invoicing, virtual terminals, and subscription billing. Businesses can also integrate the service with popular POS platforms and payment gateways, which provides more flexibility than processors that require proprietary hardware or software ecosystems.

Another advantage is that Payment Depot operates under Stax, a well-established payments company. Businesses that need additional features, such as advanced subscription tools, surcharging programs, or developer-focused payment solutions, can transition to Stax products as they scale.

Because Payment Depot is a traditional merchant account provider, businesses must complete an application and underwriting process before approval. While this may make onboarding slower for very small or new businesses, it often results in more stable merchant accounts and the ability to negotiate better processing rates over time.

Who should use Payment Depot:

Payment Depot is best for growing businesses that want customized processing rates and a flexible payment solution that can scale with their operations.

Payment Depot pricing

- Monthly fee: $0

- Transaction fees: Custom-quoted (variable rates from around 0.2% to 1.95%)

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: From $49

- Other fees: Payment Depot will charge a $19.99 monthly fee for Payment Card Industry (PCI) non-compliance if you do not keep your business compliant

Payment Depot hardware

Payment Depot has a wide selection of card readers available, including mobile and countertop solutions from popular brands like Clover, Poynt, and SwipeSimple. Those hardware items have quote-based pricing.

| Mobile Card Reader | Smart Terminals | POS Hardware |

|---|---|---|

|  |  |

| Swipe Simple B250 | Clover and Dejavoo | Clover |

| Visit Payment Depot | ||

Standout features

- Custom interchange-plus pricing: Payment Depot offers custom-quoted interchange-plus processing rates, allowing businesses to negotiate pricing based on transaction volume and business type.

- Flexible POS integrations: Unlike processors that require proprietary systems, Payment Depot integrates with several popular POS platforms and payment gateways, giving businesses more flexibility in choosing their hardware and software setup.

- Powerful virtual terminal: Payment Depot’s virtual terminal allows businesses to accept manually entered payments, digital wallets, and card-not-present transactions through a secure web-based interface.

- Business funding options: Merchants can apply for business financing through Payment Depot if they meet eligibility requirements, such as minimum credit scores and monthly revenue thresholds.

Related reading:

Chase Payment Solutions: Best for direct bank processing

Why I chose Chase Payment Solutions

When I evaluated merchant services providers for this guide, Chase Payment Solutions stood out as one of the few options offered directly by a major bank. Businesses that process payments through Chase benefit from having their processor and deposit account within the same financial institution, which can improve funding speed and simplify payment management.

Chase offers both flat-rate pricing for small businesses and negotiable interchange-plus rates for larger merchants This flexibility makes it a viable option for businesses that expect to scale and want the ability to negotiate processing costs as their transaction volume grows.

Another advantage is access to Chase QuickAccept, a mobile payment app available to Chase Business Checking customers. QuickAccept allows businesses to accept payments through mobile devices and receive same-day deposits, which can help improve cash flow compared with processors that require longer settlement times.

Chase also provides built-in analytics tools that use its banking and payment data to deliver insights into sales trends, customer behavior, and business performance. These reporting features can help merchants identify growth opportunities and better understand their transaction patterns.

Who should use Chase Payment Solutions:

Chase Payment Solutions is best for businesses that want a merchant services provider directly connected to their bank, especially those already using Chase Business Checking.

Chase Payment Solutions pricing

- Monthly fee: $0

- Card-present transaction fee: 2.6% + 10 cents

- Card-not-present transaction fee: 3.5% +10 cents

- ACH processing fee:

- Real-time deposits: 1% (capped at $25), non reversible

- Same-day deposits: 1% (capped at $25), reversible

- Standard deposits (1 business day): $2.50 for the first 10 transactions, 15 cents for additional, reversible

- Contract length: Most plans are month-to-month

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: From $49

Chase Payment Solutions hardware

| Chase Smart Terminal* | Countertop Terminal | Mobile Terminal | Chase QuickAccept Mobile Card Reader* | Chase Wireless Terminal | Chase Countertop Terminal |

|---|---|---|---|---|---|

|  |  |  |  |  |

| $499 | $299 | $399 | $49 | $499 | $399 |

| Wireless, Wi-Fi-enabled credit card terminal with digital and email receipts, transaction search, and more. | Ethernet or Wi-Fi connection with 24/7 support. Color screens with tipping functions and built-in receipt printers. | Same as the countertop terminal, but with a mobile battery that can power 450 transactions between charges. | Use the Chase Mobile app and optional card reader to accept swipe, chip, and contactless payments on the go. | Lightweight, Wi-Fi and 4G-enabled credit card machine to accept tap, dip, swipe or keyed-in card payments at your counter or on-the-go. Print receipts on the spot. | Wired credit card machine to accept tap, dip, swipe, keyed-in card payments or digital wallets at your counter. Print receipts on the spot. |

| Visit Chase Payment Solutions® | |||||

Standout features

- Same-day deposits: Chase offers same-day deposits for eligible transactions, especially for businesses using Chase Business Checking and the QuickAccept mobile payment app. This faster settlement can improve cash flow compared with processors that take several days to release funds.

- Business analytics tools: Chase provides built-in reporting tools that analyze payment and banking data to generate insights into sales trends, customer behavior, and business performance.

- Direct bank processing: Because Chase acts as both the payment processor and the receiving bank, transactions can move through fewer intermediaries, which may improve funding reliability and security.

- 24/7 customer support: Chase provides round-the-clock customer support along with online resources and help documentation.

Related reading:

GoDaddy Payments: Best for GoDaddy ecommerce sellers

Why I chose GoDaddy Payments

GoDaddy Payments stands out for its seamless integration with GoDaddy’s website builder and ecommerce platform. Businesses that already run their website or online store through GoDaddy can activate payment processing quickly without needing additional gateways or third-party integrations.

The platform supports multiple payment methods, including in-person payments, online checkouts, invoices, and virtual terminal transactions. Businesses can manage payments, orders, and website activity from the same dashboard, which simplifies operations for small teams.

GoDaddy Payments also offers competitive flat-rate pricing with no monthly subscription fees or long-term contracts. This straightforward pricing structure makes it a practical option for small businesses that want predictable payment processing costs without negotiating custom rates.

While the platform does not offer the same level of POS functionality or third-party integrations as providers like Square or Stripe, it works well for businesses that prioritize simplicity and already operate within the GoDaddy ecosystem.

Who should use GoDaddy Payments:

GoDaddy Payments is best for small businesses already using GoDaddy’s website builder or ecommerce platform that want a simple, integrated payment processing solution.

GoDaddy Payments pricing

- Monthly fee: $0

- Card-present transaction fee: 2.3%

- Card-not-present transaction fee: 2.7% + 30 cents

- Invoices/Online payment links: 2.8% + 30 cents

- Keyed-in (virtual terminal): 3.5%

- ACH processing fee: 0.8% (max $10)

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $15

- Card readers: From $79

GoDaddy Payments hardware

| Magstripe Reader | Contactless and Chip Reader | Square Terminal |

|---|---|---|

|  |  |

| $275 | $399 | $499 |

| EMV chip, magstripe, contactless payments, 6” touchscreen display, WiFi, Bluetooth, mobile capability (4G) | EMV chip, magstripe, contactless payments, 8” touchscreen display, 5” touchscreen display, WiFi, Bluetooth, mobile capability (4G LTE) | EMV chip, magstripe, contactless payments, 10.1” touchscreen display, detachable for back-office tasks, vertical tilt for viewing angle, WiFi, Bluetooth |

| Visit GoDaddy Payments | ||

Standout features

- Built-in ecommerce integration: GoDaddy Payments works natively with GoDaddy websites and online stores, allowing businesses to accept payments without configuring a separate payment gateway.

- Competitive flat-rate pricing: GoDaddy offers lower flat-rate processing fees than many competitors, especially for in-person payments.

- Unified business dashboard: Merchants can manage website activity, orders, payments, and customer data from a single GoDaddy dashboard.

- Virtual terminal and invoicing: Businesses can accept card-not-present payments and send invoices directly through GoDaddy’s payment tools.

U.S. Bank Merchant Services: Best for fast funding

Why I chose U.S. Bank Merchant Services

U.S. Bank Merchant Services stands out for its fast funding capabilities and bank-backed payment infrastructure. Businesses that already use U.S. Bank for business banking can benefit from seamless payment processing and faster access to deposited funds.

The provider offers a traditional merchant account that supports credit cards, ACH payments, invoicing, and online payments. Merchants also receive tools such as fraud protection, reporting dashboards, and access to dedicated account support.

One of its most notable features is Everyday Funding, which allows eligible businesses to receive funds the same day transactions occur, including weekends. This capability can significantly improve cash flow compared with processors that take one to two business days to settle payments.

U.S. Bank Merchant Services also supports surcharging programs and debit card optimization tools that can help businesses reduce processing costs. While its advertised pricing uses flat rates, larger businesses may also qualify for custom pricing depending on transaction volume.

Who should use U.S. Bank Merchant Services:

U.S. Bank Merchant Services is best for businesses that want fast access to funds and prefer working with a bank-backed payment processor.

U.S. Bank Merchant Services pricing

- Mobile: $0

- Unlimited users

- Up to 100 products

- Starter: $29+ per month

- Unlimited users

- Up to 500 products

- Standard: $69+ per month

- One-time set-up fee of $99

- Unlimited users and products

- Good for retail shops and small restaurants

- Premium: $99+ per month

- One-time set-up fee of $99

- Unlimited users and products

- Good for large restaurants and multi-location businesses

- Processing fees:

- In-person transactions: 2.6% + 10 cents

- Keyed-in transactions: 3.5% + 15 cents

- Online transactions: 2.9% + 30 cents

U.S. Bank Merchant Services hardware

| Mobile card reader | Handheld POS terminal | POS Register |

|---|---|---|

|  |  |

| Pair with a smartphone to accept contactless payments | Accept card payments with high sales mobility | Full register system for restaurants and retail shops |

| Visit US Bank Merchant Services for pricing | ||

Standout features

- Same-day funding: U.S. Bank’s Everyday Funding service allows businesses to receive deposits on the same day transactions are processed, including weekends for eligible accounts.

- Surcharging and debit optimization: Businesses can use surcharging programs and debit optimization tools to shift credit card fees to customers or reduce processing costs.

- Fraud protection tools: U.S. Bank offers multiple fraud prevention layers through services like Real-Time Payments monitoring, SinglePoint account controls, and IBM Trusteer Rapport security tools.

Stax: Best for high-volume businesses

Why I chose Stax

In my evaluation of the best merchant services providers, Stax stood out for its membership-based pricing model, which separates the processor’s markup from transaction fees. Instead of paying a percentage markup on every transaction, businesses pay a monthly subscription and process payments at interchange plus a small fixed fee. This structure can significantly reduce processing costs for merchants with large sales volumes.

The platform supports a full range of payment methods, including in-person transactions, online payments, virtual terminals, and recurring billing. Businesses that rely heavily on invoicing or subscription payments can also benefit from Stax’s built-in billing tools and automation features.

Stax also offers a flexible ecosystem with integrations for popular POS systems, ecommerce platforms, and business tools. This flexibility makes it a strong option for companies that want more customization than proprietary payment platforms typically provide.

Because Stax provides a traditional merchant account, businesses must complete an application and underwriting process before approval. While the monthly subscription fee may be higher than other providers in this guide, high-volume merchants can often offset that cost through lower transaction markups.

Who should use Stax:

Stax is best for businesses with high monthly transaction volumes that want to reduce effective processing costs through wholesale-style pricing.

Stax pricing

- Monthly fee: $99-$199 (depends on processing volume and software packages)

- Card-present transaction fee: Interchange plus 8 cents

- Card-not-present transaction fee: Interchange plus 15 cents

- Contract length: Month-to-month, 30 days’ notice to cancel

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: Custom quote

Stax hardware

Stax hardware is custom-quoted. A selection of BBPOS mobile readers, Z terminals, and PAX terminals are available. We have previously been quoted $100 for mobile readers, $175 to $300 for Z terminals, and $500 to $650 for PAX models. These are available for purchase for a one-time fee, or through monthly fees with protection plans.

| Mobile Card Reader | Smart Terminals | POS Hardware |

|---|---|---|

|  |  |

| Swipe Simple B250 | Clover and Dejavoo | Clover |

| Visit Stax | ||

Standout features

- Membership-based pricing: Stax uses a subscription model that allows businesses to process payments at interchange plus a small fixed fee, which can reduce effective transaction costs for high-volume merchants.

- All-in-one payment platform: Stax Pay provides a unified dashboard for managing in-person, online, and mobile payments while offering reporting tools and payment links for websites.

- Surcharging solution: CardX by Stax allows merchants to shift credit card processing fees to customers while maintaining legal compliance with surcharging regulations.

- Subscription and recurring billing tools: Stax Bill enables automated recurring payments and subscription management, including a self-service customer portal and support for multiple payment gateways.

PaymentCloud: Best for high-risk businesses

Why I chose PaymentCloud

PaymentCloud specializes in helping mid-risk and high-risk businesses obtain merchant accounts that other processors may decline. The company works with a network of partner banks and guides merchants through a structured application process to improve approval odds.

The platform supports a wide range of payment methods, including in-person payments, online transactions, invoicing, subscriptions, and manually entered payments. Businesses can also integrate PaymentCloud with many POS systems, gateways, and ecommerce platforms.

Another advantage is pricing flexibility. PaymentCloud offers custom quotes based on business type, transaction volume, and risk profile. Depending on the business model, merchants may qualify for flat-rate pricing or interchange-plus rates.

Because high-risk merchant accounts typically involve more underwriting and monitoring, businesses should expect higher processing costs than with standard processors. However, PaymentCloud’s banking partnerships and experience with high-risk industries can make it one of the most reliable options for businesses that have difficulty securing payment processing elsewhere.

Who should use PaymentCloud:

PaymentCloud is best for businesses in high-risk industries, such as tobacco, vape, firearms, and liquor, that may struggle to obtain approval from traditional merchant service providers.

PaymentCloud pricing

PaymentCloud’s fees are always custom-quoted based on specific business factors. Flat-rate and interchange rates are available depending on your business needs, and discounts are available for high-volume businesses. The pricing below are estimates we obtained from PaymentCloud.

- Monthly fee: $10 to $45

- Typical low-risk transaction fees: 2% to 3.1%

- Typical mid-risk transaction fees: 2.25% to 3.4%

- Typical high-risk transaction fees: 2.7% to 4.3%

- Payment gateway monthly fee: $15

- One-time virtual terminal fee: $15 to $45

- Contract length: None, month-to-month options available

- Early termination fees: Waived

- Chargeback fees: $25 to $45

- Cross-border fees: 1% to 2%

- 1000+ integrations available, no API required

PaymentCloud hardware

PaymentCloud has many options for card readers and POS systems. However, PaymentCloud does not disclose specific models or pricing on its site. You’ll need to contact the provider for a specific quote.

If you’re migrating over to PaymentCloud from a different processor, PaymentCloud will reprogram your existing equipment if possible.

Standout features

- High-risk merchant account approval: PaymentCloud supports industries that many payment processors decline, including firearms, tobacco products, CBD, bail bonds, and other regulated categories.

- Chargeback monitoring and protection: Businesses receive dispute alerts, tracking tools, and prevention analytics to help manage chargebacks and reduce risk.

- Flexible integrations: PaymentCloud works with a wide range of POS systems, payment gateways, and ecommerce platforms, allowing businesses to keep their existing software when switching processors.

Related reading: Best high-risk merchant account providers

Stripe: Best for customizable online payments

Why I chose Stripe

Stripe is widely used by online businesses that need flexible payment infrastructure and deep customization options. The platform provides a large library of APIs and developer tools that allow companies to build custom checkout experiences, subscription systems, and payment workflows.

Stripe supports a broad range of payment methods and international transactions. Businesses can accept payments in more than 135 currencies and offer local payment methods in many global markets, making the platform a strong option for companies selling internationally.

In addition to developer tools, Stripe also offers no-code checkout options and prebuilt integrations that make it easier to connect payments to websites and ecommerce platforms. This combination of flexibility and scalability allows businesses to start with simple integrations and expand into more customized payment systems as they grow.

However, Stripe focuses primarily on online payments and developer-driven integrations. Businesses looking for a ready-to-use POS system or mobile payment solution may find platforms like Square or PayPal easier to implement.

Who should use Stripe:

Stripe is best for online businesses that need a highly customizable payment platform, especially companies that process international transactions or require developer-level payment integrations.

Stripe pricing

- Monthly fee: $0

- Card-present transaction fee: 2.7% + 5 cents

- Card-not-present transaction fee: 2.9% + 30 cents

- Keyed-in transaction fee: 3.4% plus 30 cents

- ACH: 0.8%, $5 cap

- Invoicing: + 0.4% to 0.5%

- Recurring Billing: + 0.5% to 0.8%

- 1% additional fee for international cards and currency conversion

- Contract length: None, pay-as-you-go billing

- Early termination fee: $0

- Chargeback fee: $15 per lost dispute

- Chargeback protection and coverage available for 0.4% transaction fee

- Card readers: $59 to $349

Stripe hardware

You will need to sign up for a Stripe merchant account to access the purchase hardware options within the merchant account dashboard.

| Stripe Reader M2 | BBPOS WisePOS E | Stripe Reader S700 |

|---|---|---|

|  |  |

| $59 | $249 | $349 |

| Accept EMV chip, contactless, and mobile wallet payments. This battery-powered reader connects to your POS app via Bluetooth. | Android-based POS with a 5-inch display including PIN functionality. Connects to a third-party POS app via Wi-Fi. | Android-based smart reader for mobile and countertop use. Customize or use pre-built elements. Connects via WiFi or Ethernet. |

| Visit Stripe | ||

Standout features

- Global payment support: Stripe allows businesses to accept payments in more than 135 currencies and supports local payment methods in many international markets.

- Advanced developer tools: Stripe’s APIs and software development kits allow businesses to build custom checkout flows, subscription systems, and payment workflows.

- Stripe invoicing: Businesses can create branded invoices with payment links, automated numbering, and integrated payment tracking.

- Fraud prevention tools: Stripe uses machine learning and network data to detect suspicious transactions and reduce fraud risk, while allowing merchants to customize fraud detection rules.

Related reading:

PayPal: Best for flexible checkout options

Why I chose PayPal

PayPal remains one of the most widely recognized digital payment platforms, with hundreds of millions of active consumer accounts worldwide. Businesses that offer PayPal at checkout can often improve conversion rates because customers can complete purchases without manually entering card or shipping details.

The platform supports a wide range of payment methods, including PayPal wallet payments, credit and debit cards, digital wallets, QR code payments, and invoicing. PayPal can be used as a standalone payment processor or added alongside other merchant accounts to expand checkout options.

Like Square, PayPal operates as a payment facilitator, allowing businesses to create accounts quickly without a traditional merchant account application process. This simplifies onboarding for small businesses and startups that want to start accepting payments immediately. Read our Square vs PayPal comparison to learn more.

However, because PayPal uses an aggregated merchant account structure, accounts may occasionally experience reviews or temporary holds if unusual activity is detected. Businesses that depend on daily deposits may prefer a traditional merchant account provider for greater account stability.

Who should use PayPal:

PayPal works well for solopreneurs, small businesses with occasional sales, and online merchants that want to offer PayPal as an additional checkout option.

PayPal pricing

- Monthly fee: $0 to $30

- In-person transaction fee: 2.29% plus 9 cents

- Online transaction fee: 2.59% to 2.99% plus 49 cents

- Keyed-in processing fee: 3.49% + 9 cents

- Invoice payment processing fee: 3.49% + 9 cents

- QR code payment fee: 2.29% + 9 cents

- PayPal Checkout transaction fee: 3.49% plus 49 cents

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $20

- Card readers: $29 to $199

PayPal hardware

| PayPal Card Reader | PayPal Terminal |

|---|---|

|  |

| $79 (first one is $29) | $199 (with barcode scanner: $239) |

| Accept chip, PIN, and contactless payments. Connect to Zettle POS app via Bluetooth. Battery lasts eight hours or 100 transactions. Optional charging dock available. | Portable touch-screen POS pre-programmed with PayPal Zettle. Accept chip, PIN, contactless, and QR payments. Battery lasts 12 hours (four to six hours with intensive use). |

| Visit PayPal | |

Standout features

- Instant PayPal payouts: Funds received in a PayPal account are available immediately. Merchants can also transfer funds instantly to a linked bank account for a 1.5% fee.

- Social selling integrations: PayPal Business can connect with platforms like Facebook and Instagram, allowing merchants to accept payments directly through social commerce channels.

- International payment support: PayPal allows businesses to accept payments from customers worldwide, with support for multiple currencies and cross-border transactions.

- Fastlane guest checkout: PayPal’s Fastlane feature allows returning customers to complete purchases quickly without creating an account, improving checkout speed and reducing friction.

- Smart Receipts: PayPal digital receipts can include personalized product recommendations and promotions based on purchase history.

Related reading:

- Best mobile credit card processors

- Best credit card payment apps

- Best nonprofit credit card processing solutions

Methodology: How I evaluated the best free merchant services

Please note that my scores are based on the currently available features and information. This list will be regularly updated based on the latest technology and user demands to ensure that I provide you with the best information.

How to choose the best merchant services for your business

Choosing the best merchant services provider starts with understanding how your business accepts payments, how much you process each month, and which pricing model fits your sales volume. A startup with low transaction volume may benefit from simple flat-rate pricing, while an established or high-volume business may save more with interchange-plus, membership, or custom pricing.

Use the tables below to narrow your options by business type and pricing model, then compare processing rates, monthly fees, hardware, funding speed, chargeback fees, contract terms, and integrations before choosing a provider.

Merchant services by pricing model

Merchant services providers use different pricing models, so the best option depends on your sales volume, average ticket size, and payment mix. A startup may benefit from simple flat-rate pricing, while an established retailer or high-volume business may save more with interchange-plus, membership, or custom pricing.

| Pricing model | Best for | Providers to compare |

|---|---|---|

| Flat-rate pricing | Startups and low-volume sellers that want predictable fees | Square, PayPal, GoDaddy Payments |

| Interchange-plus pricing | Established businesses that want transparent processing costs | Helcim, Payment Depot |

| Membership pricing | High-volume businesses that can offset monthly fees with lower markups | Stax |

| Custom pricing | Larger or specialized businesses that can negotiate rates | Payment Depot, Chase Payment Solutions, U.S. Bank Merchant Services |

| High-risk processing | Businesses in harder-to-approve industries | PaymentCloud |

The cheapest merchant services provider is not always the one with the lowest advertised rate. Compare the pricing model against your monthly sales volume, average transaction size, online sales, keyed-in payments, chargebacks, and monthly fees.

Best merchant services by business type

The best merchant services provider for your business depends on how you sell, how much you process, and whether you need POS tools, ecommerce payments, bank-backed processing, or high-risk approval support.

| Business type | Recommended provider | Why |

|---|---|---|

| New small business | Square | Fast setup, no application process, and free POS tools |

| Established retail business | Helcim | Transparent interchange-plus pricing and automatic volume discounts |

| Growing business | Payment Depot | Custom pricing and strong integrations |

| Bank-first business | Chase Payment Solutions or U.S. Bank Merchant Services | Direct bank processing and fast funding options |

| High-risk business | PaymentCloud | High-risk underwriting and bank partnerships |

| Ecommerce business | Stripe or GoDaddy Payments | Online checkout, payment links, and ecommerce integrations |

| High-volume business | Stax | Membership pricing can reduce effective rates |

| PayPal-friendly business | PayPal | Recognized checkout option and simple online payments |

Use this table as a starting point, then compare each provider’s processing rates, monthly fees, hardware costs, chargeback fees, funding speed, and contract terms before choosing.

Step 1: Start with your sales volume and average ticket size

Estimate how much you process each month and your average transaction size. These two numbers help determine whether flat-rate, interchange-plus, membership, or custom pricing will likely cost less.

Low-volume businesses may prefer predictable flat-rate pricing. Higher-volume businesses should compare effective rates after monthly fees, per-transaction fees, and volume discounts.

Step 2: Choose a pricing model

Merchant services providers use different pricing models, and the cheapest option depends on how your business sells. Flat-rate pricing is easier to understand, while interchange-plus and membership pricing can be cheaper at higher volumes.

Compare flat-rate pricing, interchange-plus pricing, membership pricing, custom pricing, and high-risk processing before choosing a provider.

Step 3: List your payment types

Make a list of every payment type your business accepts or plans to accept. This may include in-person card payments, online checkout, mobile wallets, invoices, recurring billing, ACH payments, keyed-in payments, subscriptions, and payment links.

Some providers are stronger for in-person POS payments, while others are better for ecommerce, recurring payments, or custom online checkout.

Step 4: Check hardware and POS needs

Decide whether you need mobile card readers, countertop terminals, POS registers, Tap to Pay, cash drawers, receipt printers, barcode scanners, or full POS systems.

If you already use a POS system, confirm whether the merchant services provider integrates with it or requires you to switch platforms.

Step 5: Compare online payment tools

For ecommerce or remote payments, check whether the provider offers payment links, hosted checkout pages, invoices, subscriptions, digital wallets, ACH, and buy now, pay later options.

Also review whether you need developer tools, a payment gateway, fraud prevention, or integrations with ecommerce platforms like Shopify, WooCommerce, BigCommerce, or GoDaddy.

Step 6: Review funding speed and chargeback fees

Funding speed affects cash flow, especially for small businesses with tight margins. Compare standard deposit timing, same-day funding, instant transfer fees, and weekend deposit availability.

Also check chargeback fees, dispute support, refund rules, and whether chargeback fees are refundable if you win a dispute.

Step 7: Check integrations

Your merchant services provider should connect with the tools you already use. Common integrations include POS systems, ecommerce platforms, accounting software, invoicing tools, CRM systems, subscription billing, and inventory management software.

Good integrations reduce manual work and help keep payment, sales, inventory, and customer records accurate.

Step 8: Confirm contract terms and cancellation fees

Before applying, review the contract, cancellation policy, monthly minimums, PCI compliance fees, equipment leases, gateway fees, and any long-term agreement.

Avoid providers that make pricing hard to understand or require expensive cancellation terms unless the savings clearly justify the commitment.

Step 9: Test support and application requirements

Support matters because payment issues can affect revenue immediately. Check support hours, phone availability, live chat, onboarding help, dispute support, and hardware troubleshooting.

Also review the application process. Some providers approve businesses quickly, while traditional merchant accounts and high-risk processors may require business documents, bank statements, processing history, or underwriting review.

Merchant services vs merchant account vs payment processor

Merchant services, merchant accounts, payment processors, payment gateways, and POS payment providers are related, but they are not the same thing. Understanding the difference can help you compare providers more accurately.

| Term | Meaning | Best example |

|---|---|---|

| Merchant services | Tools and services that let businesses accept card, online, invoice, ACH, and digital payments | Helcim, Square, Chase |

| Merchant account | A business account that temporarily holds card payment funds before settlement | Traditional processors and banks |

| Payment processor | Company that moves transaction data and funds between the customer, card network, bank, and business | Stripe, PayPal, Chase |

| Payment gateway | Software that securely accepts online payments | Stripe, Authorize.net, PayPal |

| POS payment provider | A processor bundled with point-of-sale software and hardware | Square, Clover, Toast |

In everyday use, many people use these terms interchangeably. The main thing to remember is that merchant services is the broader category. A merchant account, payment processor, payment gateway, and POS payment provider are specific parts of how a business accepts and manages payments.

How do I apply for a merchant account?

Choosing the merchant services you want for your business is just the beginning. Depending on the solution you choose, you’ll need to submit an application.

Our guide walks you through the application process, the documents you’ll need, red flags to watch out for, and tips for negotiating lower rates.

Frequently asked questions (FAQs)

What are the best merchant services for small businesses?

Helcim is the best merchant services provider for established small businesses that want transparent interchange-plus pricing and no monthly fee. Square is better for startups that need simple setup and POS tools, while Stax and Payment Depot are better for higher-volume businesses.

What are merchant services?

Merchant services are the tools and financial services that let businesses accept credit cards, debit cards, online payments, digital wallets, ACH payments, invoices, and other customer payments.

What is the difference between merchant services and a merchant account?

Merchant services include the full set of payment tools a business uses to accept payments. A merchant account is the account that holds card payment funds before they are deposited into your business bank account.

What is the cheapest merchant services provider?

The cheapest merchant services provider depends on your sales volume and average ticket size. Square is often affordable for new or low-volume businesses, while Helcim, Stax, or Payment Depot may be cheaper for established or higher-volume businesses.

How much do merchant services cost?

Merchant services costs depend on transaction rates, monthly fees, chargeback fees, hardware, payment gateway fees, PCI compliance, and funding speed. In-person rates are usually lower than online or keyed-in payment rates.

What merchant services are best for online payments?

Stripe is best for customizable online payments, while PayPal is best for businesses that want a familiar digital wallet checkout option. GoDaddy Payments is a strong fit for sellers already using GoDaddy ecommerce tools.

What merchant services are best for high-risk businesses?

PaymentCloud is the best option in this guide for high-risk businesses because it specializes in underwriting and bank partnerships for industries that may have difficulty getting approved by standard processors.

Bottom line

Choosing the right merchant account provider can save your business lots of money in fees each month. The best payment processors are also easy to use, offer good value with business solutions, and integrate with popular software. Plus, merchant accounts should be transparent and reliable.

Visit Helcim, our top pick, to see if it’s a good fit for your business.