Maintaining an effective accounts receivable (A/R) management system is an important duty of the bookkeeper that can help your business grow, even if you expose yourself to the risks of selling goods and services on account. Creating an efficient management process can be made easier by following some well-established accounts receivable best practices—and we’ll take a look at 13 of them, from sending invoices and using invoicing software to segregating A/R duties and recording customer payments promptly.

- 1. Send Invoices Within 48 Hours

- 2. Personalize Invoices

- 3. Record Customer Payments Promptly

- 4. Establish a Formal Credit Policy

- 5. Address Customer Concerns

- 6. Act Swiftly When Customers Miss a Payment Deadline

- 7. Utilize Sales Orders to Manage Orders Efficiently

- 8. Use Invoicing Software

- 9. Integrate A/R With Accounting Software

- 10. Segregate A/R Duties

- 11. Estimate or Write Off Bad Debts

- 12. Offer Multiple Payment Options

- 13. Monitor A/R Efficiency

- What Is A/R Management?

- Frequently Asked Questions (FAQs)

- Bottom Line

1. Send Invoices Within 48 Hours

An invoice is an official document that requests payment from the customer. While you can request payment orally, issuing a formal invoice is better in case of future disagreements. Whenever possible, you should send one within 48 hours after finishing work or delivering the goods. By sending invoices immediately, customers are likely to pay quickly since the service or product is still fresh in their minds.

This also reduces your administrative burden, as sending invoices promptly prevents a backlog of unpaid work, ensures accurate financial data, and strengthens collection efforts. Potential payment problems can be identified sooner, allowing for proactive measures and increasing the likelihood of on-time payments.

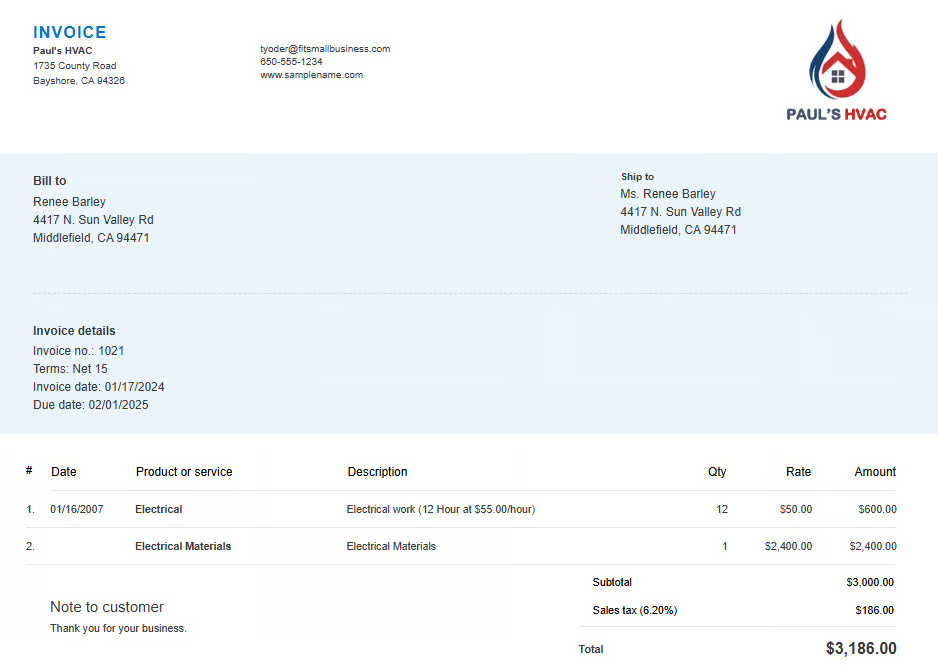

2. Personalize Invoices

An invoice is more than just a document detailing a transaction—personalized invoices add to the aesthetic value and are a reflection of your company’s professionalism. Adding your brand’s colors, for instance, help your invoices stand out and promote your company. If customers can easily identify your invoices, they may also remember them and pay them as early as possible.

An expertly designed invoice should ideally contain the following features:

- Invoice number

- Date

- Due date

- Customer information

- Itemized list of products or services

Your company logo, color scheme, and contact info should also be prominently displayed. Customizable templates allow for tailoring the invoice to your specific needs and industry.

3. Record Customer Payments Promptly

Just like sending invoices within 48 hours of receipt, it is important to record when a customer has paid your invoice. This ensures financial statements accurately reflect the company’s financial position and allows you to quickly identify discrepancies between bank statements and accounting records. Accurate cash flow projections also become possible with up-to-date payment information.

4. Establish a Formal Credit Policy

A credit policy is a form of control that protects your business from customers who don’t pay on time. Before extending credit to customers, they must undergo a strict and formal vetting process. You must set requirements, terms, and conditions that would identify the good debtors.

For example, you can set maximum credit limits to put a ceiling to the number of purchases they can make on account. Along the way, you can increase credit limits based on the customer’s payment patterns.

5. Address Customer Concerns

The primary reason customers don’t pay on time is because they are dissatisfied with the service or product provided. Have a system in place to address their concerns by putting them in touch with the proper person, preferably not your A/R clerk as they may be ineffective since they generally aren’t involved in that part of the business. Client concerns need to be dealt with before any collection calls.

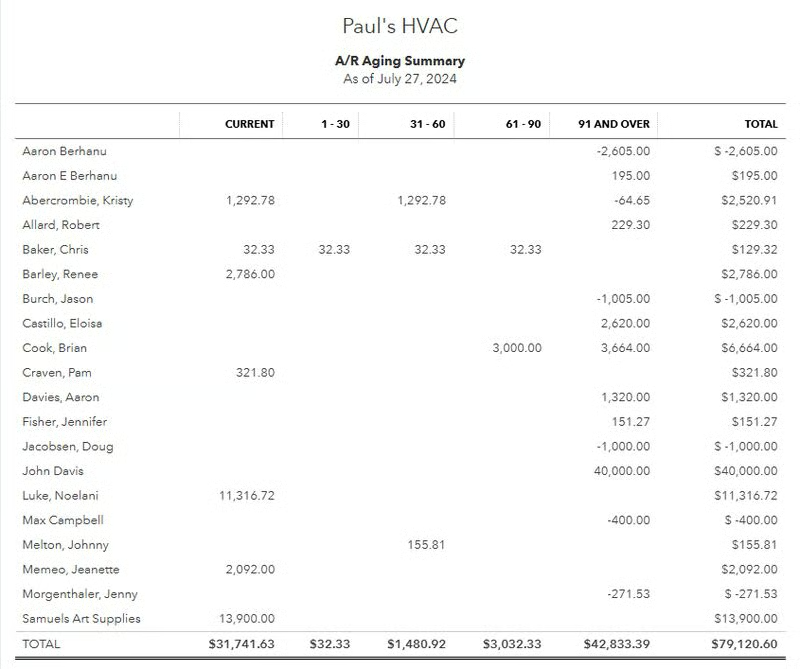

6. Act Swiftly When Customers Miss a Payment Deadline

When a customer misses a payment, you should give them the benefit of the doubt, but don’t be complacent. Generate an A/R aging report at least once a week to monitor the accounts that will come due or have become due.

If an account is past due even just for a day, contact the customer immediately to discuss it with them. Collecting from slow-paying customers is an unpleasant task, but it only becomes worse the longer you wait.

Oftentimes, missed payments can be resolved quickly with a timely phone call. In case the customer isn’t responding to your calls, you can send a collection letter by mail or email within 48 hours, whichever your customer prefers.

7. Utilize Sales Orders to Manage Orders Efficiently

A sales order (SO) is a document that helps your employees check if the products awaiting shipment match the details and specifications of the customer’s order. By clearly defining product details, quantities, prices, and delivery terms, SOs can reduce the risk of errors.

SOs provide a structured process for order fulfillment, from order entry to shipment. They also help track inventory levels, preventing a stockout and overstocking. Accurate and timely order fulfillment, facilitated by sales orders, enhances customer satisfaction.

8. Use Invoicing Software

Using one of the best invoicing software not only makes it quick and easy to create, send, and monitor invoices but also reduces your workload. The platform automates invoice creation, saving time and reducing manual errors and calculation mistakes that may occur when not using software. Other useful features include automated payment reminders (which can reduce late payments) and payment tracking (which allows you to monitor payment status).

9. Integrate A/R With Accounting Software

One of the best accounts receivable tips we have is to be sure that the software you use to track and record A/R payments is integrated with the software that records deposits and reconciles your bank account. This will ensure that the A/R payments received agree with the checks deposited in the bank account.

Integrating A/R with accounting software allows for improved cash flow management because payments are automatically recorded in the software, accelerating cash flow. This provides real-time insights into an outstanding invoice, allowing for effective collection strategies.

10. Segregate A/R Duties

Segregation of duties in A/R is a critical internal accounting control that helps prevent errors, fraud, and inefficiencies. By assigning different responsibilities to different individuals, you create a system of checks and balances. When one person handles multiple A/R functions, there’s a higher risk of fraudulent activities, so segregation reduces this risk by making it more difficult for an individual to manipulate the system.

Ideally, one person should process SOs and issue invoices and another should receive checks and apply them to outstanding invoices. In very small companies with only one bookkeeper, the owner should review all incoming checks and compare them to outstanding invoices before giving them to the bookkeeper, who should be in charge of reconciling the bank statements.

11. Estimate or Write Off Bad Debts

Bad debts are invoices that you determine will never be collected. When they arise, you should write them off the books so that they are excluded from your income and assets. However, companies using the cash basis of accounting do not have bad debt expenses since they don’t recognize income until cash is received.

GAAP

12. Offer Multiple Payment Options

Providing multiple payment options is a crucial aspect of modern A/R management. It enhances customer satisfaction, accelerates cash flow, and expands your customer base. By offering popular options like credit and debit cards, electronic checks, ACH payments, and cash or check, you will be able to accommodate customers with different financial situations or preferences. Some payment methods, like credit cards, offer quicker processing times as well.

This can also lead to a competitive advantage, as providing multiple payment methods sets your business apart from competitors with limited options. You can also drastically reduce the risk of theft or payment fraud by accepting credit cards and limiting the handling of physical cash. You’ll want to evaluate the costs associated with different payment options, factor them into your pricing, and choose a reliable payment processor that can handle multiple payment types.

13. Monitor A/R Efficiency

Use the A/R turnover ratio, the number of times you convert A/R into cash, to evaluate how effective your business is at quickly collecting A/R. Assume the A/R turnover during 2023 is 3.5. It means that we’ve collected A/R 3.5 times during the year. However, in 2024, the A/R turnover is 2.5.

A higher A/R turnover is better, so we can say that the time to collect our A/R was worse in 2024 as compared with 2023. You should track how the turnover ratio changes over time as you implement new policies and procedures.

What Is A/R Management?

A/R management is the process of extending credit to customers, issuing accurate invoices, and collecting timely payments from customers. It’s a set of policies and procedures that a company follows to manage credit sales. Managing A/R starts with credit evaluation and ends with the collection process.

A sound A/R management system should have the following:

Uniform Credit Standard

A credit standard is a set of procedures used to evaluate the creditworthiness of a customer. It answers the questions, “Which customer should be granted credit?” and “How much is the limit?” You should also consider the 5 Cs of credit to determine if the customer passes the minimum criteria you set. Applying a uniform credit standard can avoid future problems with customers claiming they’re treated unfairly.

Industry-appropriate Credit Term

A credit or payment term usually has two components:

- The cash discount, wherein you give a special discount to induce prompt payment

- The due date or the last day of the credit term

For example, you gave a customer a credit term of n/30. This term means that the customer can pay within 30 days or on the 30th day. In this case, some customers will maximize the credit term since there’s no reward for paying early. Hence, you can try adding an early payment discount to induce prompt payment. A term of 2/10, n/30 looks attractive since customers might want to get two percent off if they pay within 10 days.

Collection Program

An effective collection program will help you collect faster, providing you with cash for other business needs. Collection programs involve:

- Sending periodic statements of accounts

- Calling customers to remind them of their outstanding invoices

- Sending collection letters

- Hiring a debt collector or filing a collection suit as remedies of last resort

Aside from reducing the age of receivables, a sound collection program also reduces the risk of default. If customers pay on time or earlier, you can utilize the cash payment to replenish stocks or settle trade payables. Collecting faster and earlier reduces the risk of defaults and losses due to bad debts.

Frequently Asked Questions (FAQs)

Why is accounts receivable management important?

Receivables represent sales that have been earned but not yet collected. If not managed properly, businesses may experience cash flow problems.

What is the most important aspect of managing receivables?

Customer credit approval is a crucial aspect of A/R management. If you give credit to customers who will likely miss payments, your business will suffer the consequences.

How often should I send invoices?

Generally, invoices should be sent immediately upon delivery of goods or services, within 48 hours. This will likely require sending invoices daily.

What is the best approach to collecting overdue payments?

Start with polite reminders, and if that isn’t successful, then escalate to phone calls. Consider collection agencies or legal action as a last resort. For more information, read our guide on how to make collection calls.

Bottom Line

Managing A/R is challenging without a solid process to help you monitor A/R transactions efficiently. Poor A/R management can lead to slow-paying customers and a lack of cash when you need it. With our accounts receivable best practices, you can improve your credit granting and collection process and serve your customers even better.