Payroll reports help you track labor costs, manage cash flow, stay compliant with tax laws, and maintain employee trust. As payroll becomes more automated and more regulated, accurate reporting becomes one of your most important financial controls.

Payroll reports are documents generated from your payroll data that show critical information about employee pay, taxes, deductions, and employer liabilities. While they’re often associated with IRS filings, payroll reports can also be your guide in day-to-day business decisions, from forecasting cash needs to catching payroll errors.

For small businesses in particular, payroll reports provide visibility into one of your largest and most sensitive expenses. Running these reports consistently and carefully helps you spot cost trends, reduce risk, and ensure employees are paid accurately and on time.

In this guide, we’ll cover the most important payroll reports, how to create them, and how running them regularly supports both compliance and business stability.

Essential payroll reports

Running payroll reports should be part of your regular payroll process, and not just something you do at tax time. These reports give you the information you need to meet federal and state filing requirements and help you understand how payroll affects your cash flow, labor costs, and overall business health.

Some payroll reports are essential because they support compliance and core financial tracking. Others are helpful but optional. The reports below fall into the “must-run” category for most small businesses.

Payroll register report

The payroll register is one of the most important payroll reports you’ll run. It provides a detailed breakdown of each employee’s pay for a specific pay period, including gross wages, taxes withheld, deductions, and net pay.

You should run a payroll register every time you process payroll. If you manage payroll manually, this means compiling pay data into a spreadsheet so you can clearly see what was paid and withheld. If you use payroll software, the payroll register is typically a standard report you can generate automatically after each payroll run.

The payroll register report is useful for several critical tasks, such as:

- Preparing annual tax forms, including Form W-2

- Reviewing payroll for errors before payments are finalized

- Reconciling payroll expenses with your accounting records

- Providing documentation for your accountant, bookkeeper, or auditor

Because it captures the full picture of what you paid and why, the payroll register is often the first report you review when something looks off or when you need to explain payroll costs to a lender, advisor, or tax agency.

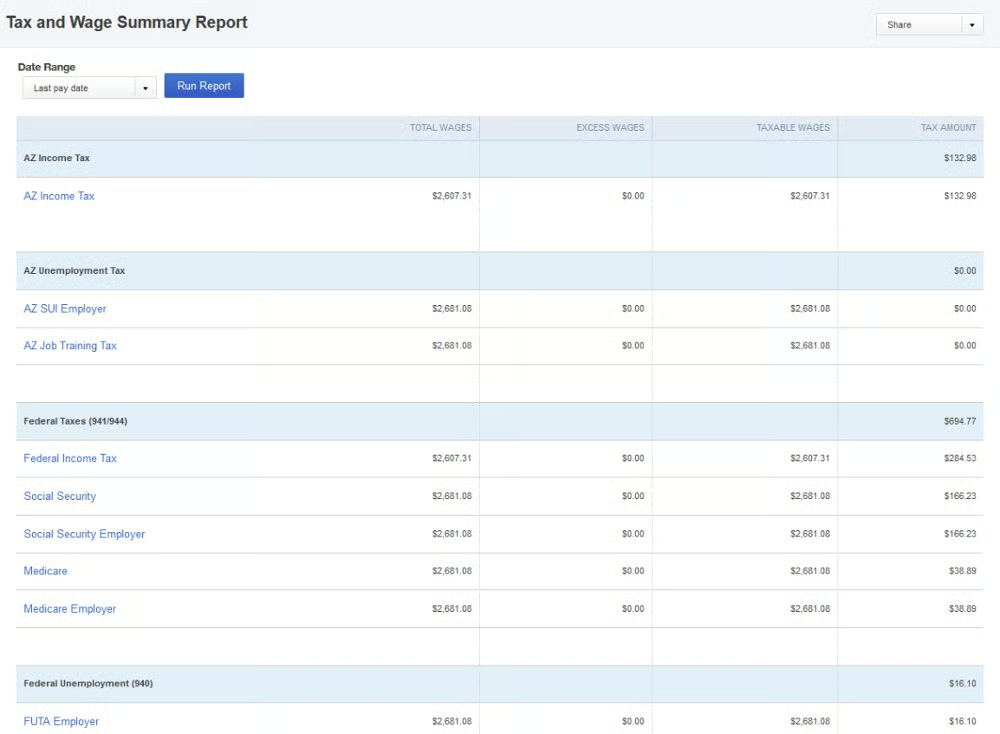

Payroll tax and wage summary

A payroll tax and wage summary report shows each employee’s taxable wages and the total payroll taxes paid for a specific period. Unlike the payroll register, which provides line-by-line detail, this report rolls your data up into a clear summary that’s designed specifically for tax reporting.

You’ll rely on this report when filing state and local payroll taxes, and in many cases, the information it contains is required to complete those filings accurately and on time. Because filing schedules vary by jurisdiction, it’s important to run this report for the correct period, whether that’s monthly, quarterly, or annually.

This report helps you:

- Prepare accurate state and local tax filings by clearly showing each employee’s taxable wages and total taxes owed for the filing period.

- Spot calculation issues early, such as an employee whose state tax withholding suddenly drops to zero or doesn’t match prior periods.

- Avoid penalties and notices by confirming that the wages and taxes you’re reporting align with what you actually paid and withheld.

If you use payroll software, generating a payroll tax and wage summary report is typically straightforward and built into the system. If you manage payroll manually, you’ll need to compile each employee’s taxable wages and taxes paid into a spreadsheet for the period you’re reviewing, which increases the risk of errors if records aren’t carefully maintained.

Workers’ compensation wages report

A workers’ compensation wages report shows the wages you’ve paid that are subject to workers’ compensation insurance. Insurers use this information to calculate your premiums, which means even small reporting errors can affect what you owe.

If you use payroll software, this report is typically generated automatically based on employee classifications and earnings. If you track payroll manually, you’ll need to compile wage data for each employee (including overtime, bonuses, and tips) into a spreadsheet for the pay period you’re reviewing. Because premiums are tied directly to wages, it’s best to run this report with each payroll cycle rather than waiting until audit time.

Reviewing this report regularly helps you:

- Estimate workers’ compensation premiums more accurately, so you’re not surprised by adjustments at the end of the year.

- Catch classification issues early, such as an employee being assigned to the wrong job class or rate code.

- Support audits and claims by showing exactly what an employee earned if a workplace injury occurs.

For example, if an employee is injured and there’s a dispute about their average earnings, this report provides documented proof of wages paid at the time of the incident. Keeping it up to date not only supports compliance with state requirements but also helps protect your business financially if a claim or audit arises.

Retirement plan contributions report

A retirement plan contributions report shows how much you and your employees have contributed to retirement plans during a specific period. It tracks both employee deferrals and any employer contributions, which makes this valuable when confirming that contributions were calculated correctly and deposited on time.

This report is also usually generated automatically based on each employee’s elections and pay if you’re using payroll software. If you run payroll manually, you’ll need to compile wage data and contribution amounts (both pre-tax and post-tax) for every employee, along with any employer match or profit-sharing contributions you offer. The report typically shows the type of retirement plan, individual contribution amounts, and total contributions for the period.

A periodic review of this report will help you:

- Verify contributions are accurate and timely, which is especially important for meeting Department of Labor and IRS requirements.

- Catch setup or deduction errors early, such as an employee contributing at the wrong percentage or missing an employer match.

- Answer employee questions confidently, using clear records if someone asks whether their contributions were processed correctly.

For example, if an employee notices that a paycheck didn’t reflect their 401(k) contribution, this report lets you quickly confirm whether the deduction was taken and when it was deposited. Keeping this report up to date protects your business from compliance issues while reinforcing trust with employees who rely on these benefits for long-term financial planning.

Voluntary payroll reports

Not every payroll report is tied to a federal or state filing, but that doesn’t make these reports optional in practice. Voluntary payroll reports help you understand where your payroll dollars are going and give you visibility into costs that aren’t always obvious from a single payroll run.

These reports are especially useful when you’re planning ahead, like when preparing a budget, evaluating benefits costs, or deciding when it’s time to hire. While you may not be required to generate them on a set schedule, reviewing these reports regularly helps you make informed decisions based on real payroll data rather than estimates or assumptions.

In other words, voluntary payroll reports won’t keep you compliant on their own, but they help you stay in control of your payroll costs and avoid surprises as your business grows.

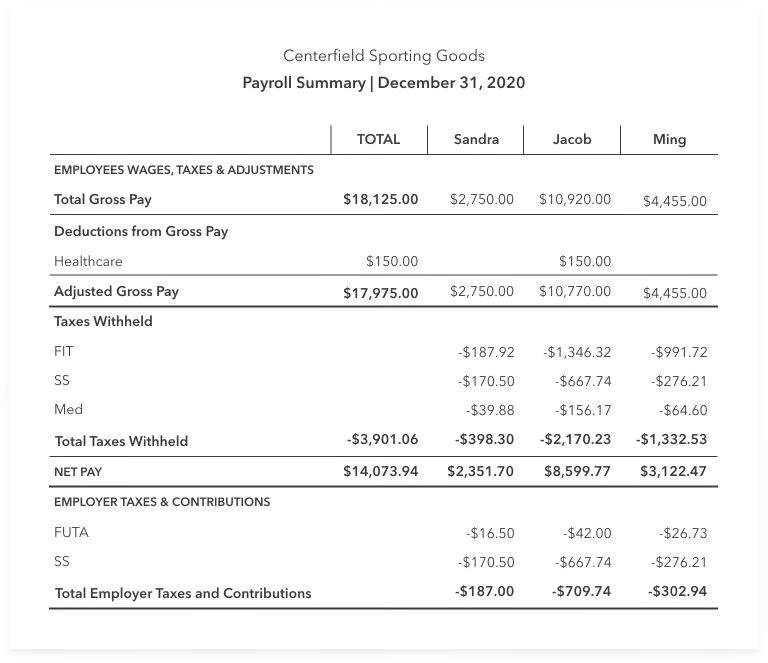

Payroll Summary

A payroll summary report gives you a high-level view of your company’s payroll activity over a specific period. Instead of focusing on individual paychecks, it shows aggregate payroll information, which is useful for recordkeeping, compliance, and financial planning.

Running this report regularly helps you meet Fair Labor Standards Act (FLSA) record-retention requirements, which generally require employers to keep most payroll records for at least three years. It’s also one of the first reports lenders ask for when you apply for a business loan, since it helps them understand your ongoing employee-related expenses.

Payroll summary reports typically include:

- Employee name, hire date, and end date (if applicable)

- Gross pay

- Adjusted gross pay

- Net pay

- Employer taxes and contributions

This also comes as a standard report that you can generate on demand with payroll software. If you’re doing it manually, you’ll need to pull data from individual employee records and consolidate it into a single spreadsheet, which can be time-consuming and harder to keep consistent over time.

Reviewing a payroll summary report helps you:

- See total payroll costs at a glance, including wages, employer taxes, and contributions

- Provide documentation quickly when a lender, accountant, or advisor requests it

- Track changes over time, such as payroll growth after new hires or pay increases

For example, if you’re preparing a loan application or annual financial review, this report lets you clearly show how much you spend on payroll each month without digging through individual pay records.

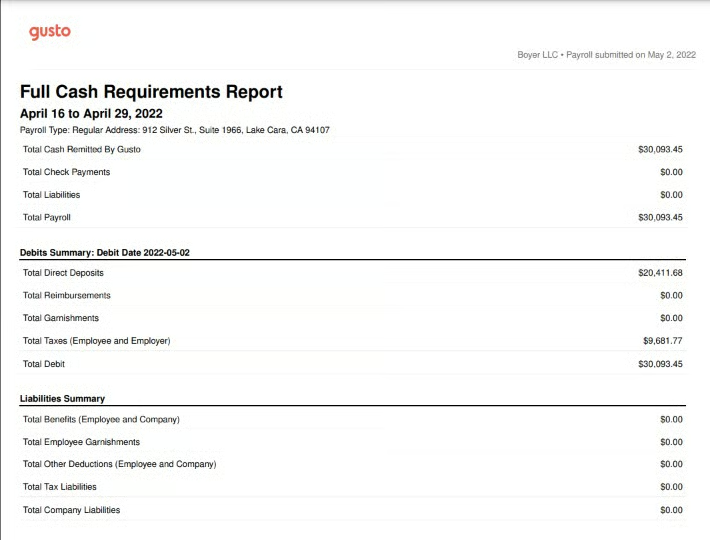

Cash requirements report

A cash requirements report shows you exactly how much money you need on hand to run payroll for an upcoming pay period. Instead of looking only at employee wages, it accounts for total payroll outflow, including taxes, benefit withholdings, and other deductions, so you’re not caught short when payroll is due.

A typical cash requirements report breaks payroll costs down into:

- Employee wages

- Payroll taxes

- Benefits withholdings

- Other deductions

All of this information feeds into the report, which helps you:

- Confirm you have enough cash available to cover payroll without dipping into reserves or credit.

- Avoid last-minute scrambles, such as transferring funds or delaying payments.

- Plan around uneven cash flow, especially if your revenue fluctuates month to month.

Let’s say your payroll falls just before a major customer payment comes in. In that case, this report helps you anticipate the gap and plan accordingly, rather than discovering it on payday.

If you process payroll manually, it’s best to create this report as part of your payroll workflow so you can easily transfer the figures as you calculate pay. If you use payroll software, this report is often generated automatically once payroll is processed, giving you an immediate snapshot of the total cash needed.

If you process payroll manually, it’s best to create this report as part of your payroll workflow so you can easily transfer the figures as you calculate pay. If you use payroll software, this report is often generated automatically once payroll is processed, so you have an immediate snapshot of the total cash needed.

Benefits and deductions report

A benefits and deductions report shows how much you and your employees are paying for benefits and other non-tax deductions during each pay period. It breaks these costs down by employee and gives you a picture of the true cost of employment beyond wages alone.

This report typically includes:

- Employee name

- Employer-paid benefit costs (such as health insurance or employer retirement contributions)

- Employee-paid portions of benefits

- Other non-tax deductions

If you run payroll manually, it’s easier to create this report alongside payroll since you’re already collecting the necessary information. Many small businesses duplicate this data into a spreadsheet to track benefit costs over time. If you use payroll software, this report also comes as a standard option.

With this report on hand, it’s easier to:

- Understand the full cost of employing each worker aside from their take-home pay.

- Evaluate benefit offerings, such as whether premiums or deductions have increased year over year.

- Plan for growth by estimating how new hires will affect total compensation costs.

This report comes especially handy if you’re considering adding a new benefit or increasing employer contributions, and would like to see how those changes would impact your payroll budget. While it shouldn’t be the sole factor in staffing decisions, running a benefits and deductions report at least annually gives you valuable insight into how benefits affect your bottom line.

Employee time report

An employee time report shows how many hours each employee worked during a specific pay period. For hourly employees, this report is essential for accurate payroll. When paired with time tracking or project management tools, it can also show how employee time is allocated across projects, clients, or tasks.

Many small businesses rely on employee time reports to calculate payroll when they don’t use a fully integrated payroll system. In those cases, employees may track their hours using timesheets, which are then compiled into a single report before payroll is processed. If you use payroll software with built-in time tracking (or enter hours directly into your system), this report can usually be generated automatically with minimal effort.

With an employee time report, you have a view to:

- Ensure employees are paid correctly, especially for overtime or variable schedules.

- Spot inconsistencies, such as missing hours or unusually high time entries.

- Identify workload or efficiency issues, particularly if projects are running behind schedule

For example, if an employee consistently logs full-time hours but assigned work isn’t being completed on time, the time report gives you a starting point for a productive conversation. While this report is often run every pay period for payroll purposes, reviewing it quarterly or as issues arise can provide additional operational insight.

Time off expense report

A time off expense report shows what it actually costs your business to provide paid time off (PTO). Unlike an employee time report, which tracks hours worked, this report focuses on the wages paid for time employees are not working, such as vacation, sick leave, or other paid leave.

A time off expense report helps you:

- Understand the true cost of PTO, especially as your team grows.

- Compare leave usage over time, such as year-over-year increases in paid time off.

- Plan for staffing and coverage, particularly during peak vacation periods.

If you create this report manually, you’ll need to list each employee’s name, hourly rate, and the total amount of paid time off taken during the period you’re reviewing. Multiplying time off hours by pay rates gives you a clear estimate of PTO-related payroll costs. If you use payroll software that tracks employee hours and leave balances, this report is usually accessible from your dashboard.

Time off expense reports are most useful when reviewed alongside payroll and benefits reports. This way, you have a more complete picture of labor costs. Running this report at least semi-annually helps you budget accurately and avoid underestimating the impact of paid time off on your overall payroll expenses.

How to create a payroll report

Creating a payroll report isn’t complicated, but it does require intention. Whether you’re preparing a report for tax filing or reviewing payroll costs internally, the goal is the same: pull accurate data for the right time period and use it to make informed decisions.

No matter how you manage payroll—spreadsheets or payroll software—creating a payroll report generally follows three key steps.

1. Decide what information you need

Start by clarifying why you’re running the report. Are you filing taxes, reviewing labor costs, or checking for errors? The purpose of the report determines what data should be included.

If you use payroll software, you can usually select from standard reports or customize which fields to include. For example, if you’re reviewing overall payroll expenses, you may not need employee names or identifying details. Keeping reports focused makes them easier to review and reduces the chance of overlooking important information.

If you use spreadsheets, you’ll need to manually pull data from your payroll records and consolidate it into a report. Because this step involves manual data entry, it’s especially important to double-check figures to avoid errors that could lead to incorrect filings or poor business decisions.

2. Select the right time period

Next, choose the time range the report should cover. For IRS or state filings, this is usually non-negotiable. You’ll need to run the report for the exact period required, such as a specific quarter or calendar year.

For internal reports, you have more flexibility. The key is choosing a time frame that gives you meaningful insight. For example, reviewing benefits costs over a full year will provide a more accurate picture than looking at a single month, especially if your headcount or benefits offerings changed during the year.

Not every report needs to be run every payroll cycle. Annual reports, like those used to prepare W-2s, only need to be generated once per year. Others, such as cash requirements or payroll registers, are most useful when run with every payroll.

3. Review and use the results

Once the report is generated, take time to review it before acting on the data. For compliance-related reports, confirm that the time period is correct and scan for obvious discrepancies, such as unusually high or low totals.

Comparing reports over time can also help you catch issues. For example, if your quarterly payroll taxes differ significantly from the previous quarter and nothing major changed, it may signal an error worth investigating.

For internal analysis, use the report to understand where your payroll dollars are going. An annual benefits report, for instance, can reveal how much you’re spending on employee benefits and help you plan for the year ahead. The real value of a payroll report is in using the information to make better decisions.

Payroll report best practices and tips

While payroll reports are historical records, they’re tools you can use to manage cash flow, spot issues early, and stay compliant as your business grows. The key is building payroll reporting into your regular process.

Here are a few best practices to help you get the most value from your payroll reports.

- Be consistent with when you run reports: Generate payroll reports on a predictable schedule that aligns with your pay cycle. While not every report needs to be run every time, your payroll process should clearly define which reports are run each payroll, quarterly, or annually.

- Keep payroll data accurate and up to date: Payroll reports are only as reliable as the data behind them. Make sure employee details, hours worked, pay rates, tax settings, and benefit elections are correct before payroll is processed. Even small errors can snowball into compliance issues, corrections, or penalties later.

- Use a payroll system you can rely on: Manual payroll increases the risk of errors and makes reporting harder to maintain as your business grows. A reliable payroll system automates calculations, keeps records organized, and allows you to generate standard reports quickly. This saves time and reduces the chance of mistakes that are costly to fix after the fact.

- Don’t just file them, review your reports: Running a report is only half the job. Reviewing payroll reports regularly helps you catch errors, monitor trends, and make informed decisions. For example, a steady rise in overtime costs may signal workload imbalances or the need to hire additional staff.

- Know when to bring in expert help: If you’re unsure about payroll reporting requirements or notice inconsistencies you can’t explain, it’s worth consulting a professional. An accountant or payroll specialist can help you confirm compliance, interpret reports correctly, and fine-tune your payroll process.

Read our top tips for managing your payroll to ensure your process is efficient and error-free.

Benefits of payroll reports

Payroll reports help you understand the full impact of payroll on your business. When reviewed regularly, they provide clear, actionable insights that support compliance, cost control, and smarter decision-making. In summary, payroll reports help:

- Simplify compliance and tax filing by consolidating payroll data needed for federal, state, and local reports, including quarterly filings like Form 941.

- Improve visibility into payroll costs, helping you understand how wages, benefits, taxes, and deductions affect your bottom line.

- Spot issues early, such as rising overtime, benefit cost increases, or payroll errors, before they become costly problems.

- Track business performance over time, using payroll data to evaluate productivity, profitability, and operational efficiency.

- Support smarter decision-making, giving you reliable data to guide hiring, compensation, and growth planning.

Payroll Report Frequently Asked Questions (FAQs)

How often should I generate payroll reports?

The frequency of generating payroll reports depends on your pay schedule, business needs, and the type of report. It’s standard practice to generate certain payroll reports each pay period, like the payroll register and payroll tax and wage summary. Other reports may only need to be run as needed or as required by the IRS or your state tax agency.

What should I do if I find errors in a payroll report?

Should you discover errors in any payroll report, correct it immediately. Errors can lead to legal issues, financial penalties, and unhappy employees. If the error relates to employee wages or deductions, ensure you communicate the issue and any corrections made to the affected employee immediately.

How long should I keep my payroll reports?

We recommend keeping your payroll reports as part of your regular payroll records, which should be kept for at least three years. Some states require you to keep these records longer so make sure you’re checking with your local and state laws to ensure compliance.

Bottom line

Running regular payroll reports not only gives you deep insights into your company’s operations, but it can also help you streamline federal and state filings. You can create these reports manually but using payroll software is the best way to ensure accuracy with payroll reporting, helping you effectively manage your business.