Learning how to accept credit card payments online for free usually means finding a provider with no monthly, setup, or cancellation fees. Credit card processing itself is not free because card networks and processors charge transaction fees on every card sale, including non-negotiable interchange fees.

For most small businesses, Square is one of the easiest ways to start accepting payments online because it has no monthly minimums, no application process, and free tools for online checkout, invoices, a virtual terminal, and POS. Other strong options include Stripe or Shopify for ecommerce, Helcim for recurring billing and zero-cost processing options, and PaymentCloud for high-risk businesses.

- Best free online credit card payment options

- Can I avoid credit card processing fees?

- What are the most affordable ways to accept credit card payments online?

- What are the costs of accepting payments online?

- How do I choose the right payment processor?

- How can I cut down on my credit card processing fees?

- Frequently asked questions (FAQs)

- Bottom line

Best free online credit card payment options

| Best for | Monthly Fee | |

|---|---|---|

| Helcim | Zero-cost payment processing, accepting alternative payment methods, and recurring payment tools | $0 (with POS) |

| Stripe | Free invoicing, low-cost ACH processing, and custom online checkouts | $0-$10 |

| PaymentCloud | High-risk merchants looking for surcharging tools | $10-$45 |

| Square | Free and instant access to merchant services for small and new businesses | $0-$165 (with POS) |

| Shopify | Merchants using the Shopify ecommerce platform | $5-$299 |

| Payment Depot | Businesses with growing sales volume | $0 |

| PayPal | Solopreneurs and occasional sellers | $0-$30 (with POS) |

| CardX | Businesses looking for surcharging features | $29+ |

Can I avoid credit card processing fees?

There are ways to avoid some of the credit card processing fees when accepting online payments. You can pass on the fees to your customers or choose a different payment method altogether.

Learn more: How to Accept Payments Online in 5 Steps

Consider adding a “zero-cost” credit card processing program

In some US states, it’s legal for merchants to pass on their credit card processing fees to customers. Depending on where a business is located, the following methods are available for those who accept credit cards online:

- Convenience Fee: Fixed amount added as a fee at checkout

- Credit Surcharging: Credit card processing fees that are added to the product price

- Cash Discounting: Discounts offered to customers who pay with cash; cash discounting for online purchases is possible with merchant processors that offer ACH payment processing services.

However, these online payment methods are far from being absolutely free. Zero-cost credit card processing doesn’t let businesses avoid other processing fees, such as merchant account costs and transaction fees for ACH and debit card payments.

Additionally, merchants should make sure that their website has a system in place to verify that customers are located in states that allow all methods.

Several payment processing providers offer these services, but merchants should be aware of key factors that make a reliable zero-cost credit card payment processor.

- Helcim: For merchants that accept ACH payments

- CardX by Stax: For out-of-the-box, fully compliant online credit surcharging

- PaymentCloud: For high-risk merchants that want both traditional and credit surcharging payments

Zero-cost payment processors compared

| Monthly Fee | Transaction Fee | Chargeback Fee | |

|---|---|---|---|

| Helcim | $0 | 0.5% + 25 cents (ACH) | $15(reversible) |

| CardX | From $29 | From 2.91% (debit card transactions) | Debit card chargeback fee not disclosed |

| PaymentCloud | $0-$30 | Custom | $25 |

Read more: Free Credit Card Processing for Small Businesses

Add online ACH & echeck as alternative payment methods

One of the most affordable ways to accept payments online is through an ACH (automated clearing house) transfer. If you have ever received a direct deposit paycheck from your employer or paid bills online using your bank account, those are examples of ACH payments.

For businesses, ACH payments often have significantly lower transaction fees than credit or debit card payments. I’ve found it to be a popular option for companies that bill via invoice or have recurring payments, such as freelance creatives and law firms.

Popular social payment apps like Venmo and Zelle also use ACH payments to transfer money for free.

That said, ACH payment authorization is not instant, unlike card payment transactions. They also require the customer to enter their bank account and routing numbers, so it’s not ideal for retailers or other online businesses that have shopping cart functions.

Some of the best ways to accept ACH payments online include the following:

- Stripe: Free invoicing for online businesses with low-cost ACH processing and competitive credit card payment processing

- Square: Free invoicing software with built-in estimates and contracts builder, plus no cap ACH payment processing

- Helcim: Free merchant account with low-cost ACH processing for large-volume businesses

- PaymentCloud: Low-cost ACH processing for high-risk merchants

ACH & echeck processors compared

| Monthly Fees | ACH Fee | ACH Minimum | ACH Cap | |

|---|---|---|---|---|

| Stripe | $0-$10 | 0.8% | None | $5 |

| Square | $0-$20 | 1% | 1% | None |

| Helcim | $0 | 0.5% + 25 cents | None | $6 |

| PaymentCloud | $10-$45 | 0.5%-1.5% | None | None |

Learn more:

What are the most affordable ways to accept credit card payments online?

Although it’s impossible to accept credit card payments online for free, choosing a processor with low, competitive fees can still save your business a lot of money. The cheapest way to accept credit card payments for your business depends on what and how much you are selling.

Additionally, passing on credit card processing fees to customers may not be an available option because it is illegal in some states, or merchants risk losing customers.

Here are the cheapest credit card processing strategies for online sales:

Sell from an ecommerce platform

If you’re a retail business needing to accept credit cards online to sell products, my suggestion as to the most straightforward and economical option is to use an ecommerce platform or website builder with built-in payment processing. Opting for an ecommerce store with integrated payments simplifies the process of setting up and managing your store. It also allows you to collect and act on more detailed information about your customers.

The most affordable online store solutions with built-in payment processing include the following:

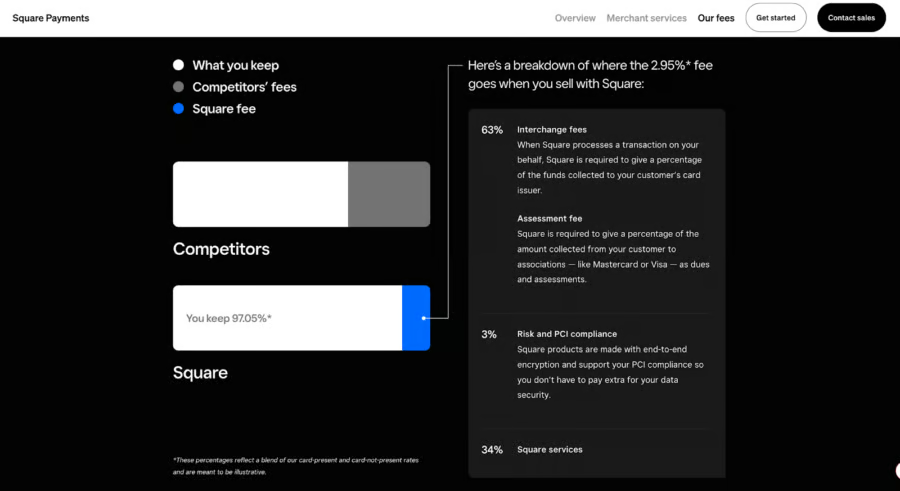

- Square: Free online store with low-cost transaction fees, best for brick-and-mortar businesses wanting to accept payments online. Online transaction fees are 2.9% plus 30 cents.

- Shopify: Affordable small-business solution with ecommerce plans starting at $5 per month, best for new ecommerce businesses. Online transaction fees range from 2.4% + 30 cents to 2.7% + 30 cents, depending on your plan.

Ecommerce platforms compared

| Monthly Fees | Online Transaction Fees | Payment Processor | Multichannel Sales | Best for | |

|---|---|---|---|---|---|

| Square | $0-$149 | 2.9%-3.3% + 30 cents | Square Payments | Included | Small brick-and-mortar businesses |

| Shopify | $5-$399 | 2.4%-2.7% + 30 cents | Shopify Payments or third-party processor for a fee | Included | Ecommerce businesses |

Both Square and Shopify also have native tools to set up recurring billing or subscriptions. Learn more in our comparison of Shopify vs Square.

Related reading:

Apply for a traditional merchant account

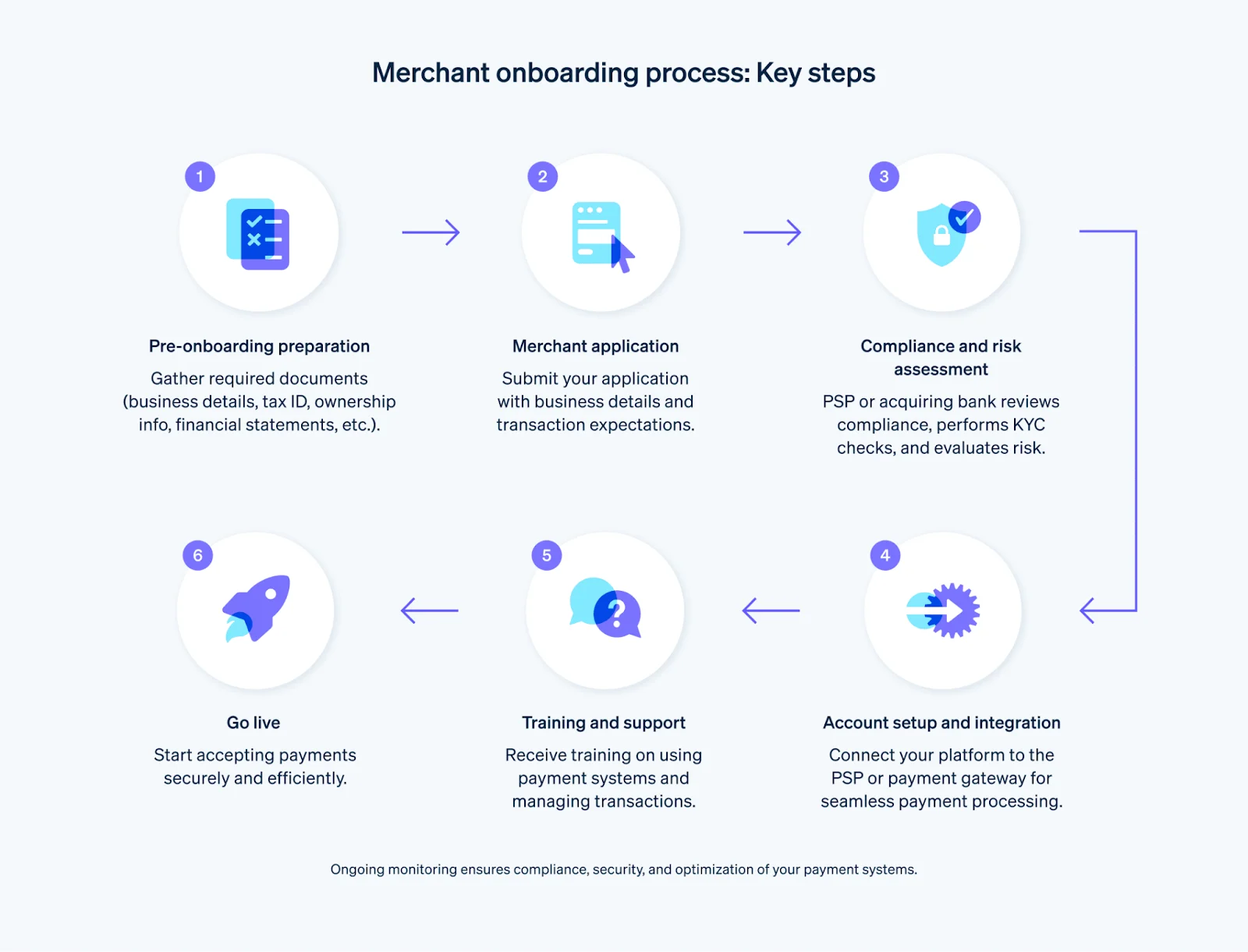

If you have an established or high-volume business (consistently processing over $20,000 per month), accepting credit cards through a traditional merchant account could be the least expensive option for your business. A merchant account is a type of bank account, so it’s a more formal setup than something like Square or PayPal because it usually requires an application and approval process. Learn more in my application guide below.

However, higher-volume businesses could receive more competitive rates from a merchant account provider than an all-in-one ecommerce platform that has set flat fees. Existing brick-and-mortar businesses could negotiate competitive online processing fees with their current payment processor.

You may also need a payment gateway to connect your merchant account with your online store. There’s no one-size-fits-all instruction for this option. Some merchant account providers, like Stax and Payment Depot, come with built-in gateways at no extra cost, while others, like Authorize.net, require you to pay an additional monthly fee or to use a separate gateway.

The most affordable merchant services for online payments include the following:

- Helcim: Best option for low-cost interchange-plus processing with no monthly fee. It also has automated volume discounts that make it competitively priced for established online, in-person, and multichannel payments of all sizes.

- Square: Best for new businesses and individuals

- Payment Depot: Affordable option for growing businesses

Traditional merchant accounts compared

| Monthly Fees | Online Transaction Fees | Card-present Transaction Fees | Chargeback Fee | |

|---|---|---|---|---|

| Helcim | $0 | Interchange plus 0.15% + 15 cents to 0.5% + 25 cents | Interchange plus 0.15% + 6 cents to Interchange plus 0.4% + 8 cents | $15 reversible |

| Square | $0 | 2.9%-3.3% + 30 cents | 2.4%-2.6% + 15 cents | Waived up to $250/month |

| Payment Depot | $0 | Custom interchange plus rate | Custom interchange plus rate | $25 |

Accept recurring payments

Businesses that offer memberships, subscriptions, and professional services require the ability to collect the same fees from customers on a regular basis. Recurring payment processors typically have tools for quotes, billing, and invoicing to help you bill, track, and accept payments from customers.

With a recurring payments option, customers will only need to enter their card information once instead of repeatedly being asked to do so every time you send them an invoice. Some payment processors also charge a smaller card-on-file transaction fee than keyed-in rates.

There are various reliable all-in-one payment processors that support recurring payments:

- Helcim: For high-volume merchants that will benefit from automatic volume discounts

- Square: Free online and in-person POS system ideal for small businesses and startups.

- PayPal: For seasonal businesses that accept PayPal payments

- Stax: Cheapest wholesale rates for large-volume businesses

- Stripe: Best for B2B businesses accepting international sales

Recurring payment processors compared

| Monthly Fee | Invoice Fee | Card-on-File Rate | |

|---|---|---|---|

| Helcim | $0 | $0 | 0.2% + 10 cents to 0.5% + 25 cents |

| Square | $0 | $0 | 3.5% + 15 cents |

| PayPal | $0 | $10-$40 | 3.49% + 49 cents |

| Stax | $99-$199 | $0 | Interchange plus 18 cents |

| Stripe | $0 | 0.5%-0.7% | 2.9% + 30 cents |

Learn more about accepting recurring payments and find more payment processing providers.

What are the costs of accepting payments online?

As already mentioned, there is no way to accept credit card payments online for free because card issuers, card networks, and payment processors charge fees on each card transaction. These fees include interchange fees, which are paid to the card-issuing bank, plus processor markups and, in some cases, monthly software or merchant account fees.

The exact cost depends on your processor, payment method, plan type, transaction volume, and whether the customer pays online, in person, by invoice, or through a manually keyed transaction. Online credit card payments usually cost more than in-person payments because card-not-present transactions carry more risk.

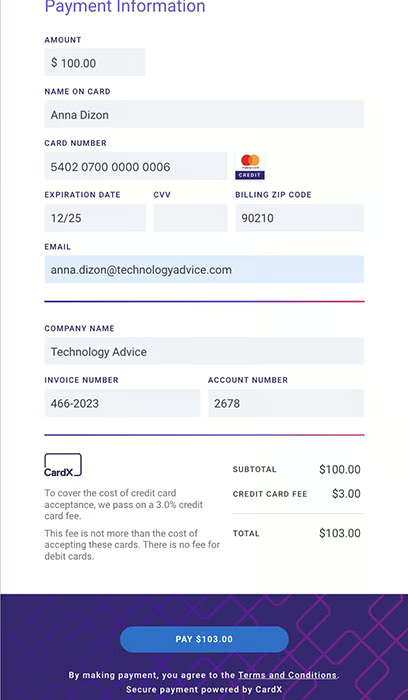

For example, Square Free has no monthly subscription cost, but online and invoice card payments cost 3.3% + 30 cents per transaction. Here is how that fee affects common online transaction amounts:

| Sale amount | Square online card fee (3.3% + 30 cents) | You receive |

|---|---|---|

| $25 | $1.13 | $23.87 |

| $100 | $3.60 | $96.40 |

| $500 | $16.80 | $483.20 |

| $1,000 | $33.30 | $966.70 |

Percentage-based fees have a larger impact on high-ticket sales, while fixed fees matter more for small-ticket transactions. For example, the 30-cent fixed fee is a small part of a $1,000 sale, but it makes up a much bigger share of the processing cost on a $25 sale.

Below are typical costs for accepting payments online:

| Fee type | Typical cost |

|---|---|

| Monthly merchant account or software fee | $0 to $200 |

| Online card transaction fee for low-volume businesses | Around 3% per transaction |

| Online card transaction fee for businesses processing above $20,000 per month | Around 2% per transaction |

| High-risk transaction fee | Around 4% per transaction |

| ACH payment fee | Often around 1% per transaction, sometimes with a minimum or cap |

Merchants that use a free credit card processing or surcharge program may pass eligible credit card processing fees to customers. However, surcharging rules vary by state, card brand, payment method, and processor. Debit card transactions and ACH payments generally cannot be surcharged the same way credit card payments can, so businesses may still be responsible for those transaction costs.

Learn more: Credit Card Transaction Fees

How do I choose the right payment processor?

Consider the following when choosing a payment processing solution for your business:

1. Compare transaction fees: For new and small businesses, solutions like Square and PayPal with flat fees and no monthly minimums are usually the most affordable. As your business grows, solutions with interchange-plus or membership pricing, such as Payment Depot and Stax, can offer the lowest rates. If you are looking for the cheapest credit card processing fees, avoid tiered pricing at all costs.

2. Find competitive monthly fees: Some solutions offer low transaction rates but have high monthly fees.

3. Watch out for startup fees and applications: Traditional merchant services accounts typically have longer setup processes than third-party credit card processing solutions because there is an approval process.

4. Review contracts and requirements: Some solutions require you to sign up for a year or more; others require your business to meet monthly transaction minimums.

5. Evaluate for compatibility with your website: Make sure the service you choose integrates well with your website hosting service.

6. Check for fast setup and ease of use: Small businesses should look for free and remote setups. The ideal payment processor should also have an easy-to-navigate interface, accessible knowledge base, and fast deposit times.

7. Evaluate payment security features: The best payment processors are Payment Card Industry (PCI)-compliant and come with fraud protection tools, such as tokenization, address, and IP verification.

How can I cut down on my credit card processing fees?

While there are many ways to accept payments online, free credit card processing may still not exist for businesses in the foreseeable future. However, there are many ways you can reduce the fees you pay. Here are just a few:

1. Set a minimum: You can require a minimum purchase amount for credit card payments. This can also help increase average order value (AOV).

2. Negotiate new rates: It doesn’t hurt to ask your processor if it can accommodate more affordable rates. If you have a longstanding history with its platform, then remind your provider of that — the bigger and more established your business, the more leverage you have in negotiating. You can also choose a processor that automatically discounts your rates as your business grows, such as Helcim.

3. Eliminate extra services: If your payment processor includes additional services, features, or tools, make sure you’re not paying for them—especially if you don’t use them.

4. Minimize chargebacks: Merchants facing credit card fraud lose a lot of time and money to fraudsters and in managing these instances. Use chargeback prevention tools and take other steps to reduce chargebacks and fraud in your business. Check out our guide to preventing chargebacks and our top recommendations for chargeback protection services.

5. Offer alternative payment methods: In general, card-present transaction fees are cheaper than when accepting card payments online because there is less risk of fraud. Peer-to-peer payments are also an affordable alternative. Zelle for example, does not charge any transaction fees and comes with fast access to funds. Learn how to use Zelle for business.

Looking to increase online sales? Consider adding a buy now, pay later (BNPL) option at checkout. BNPL transaction fees are typically higher than regular credit card processing fees. The tradeoff is that average order values are also typically higher for BNPL purchases. Check out our small business guide to BNPL.

Frequently asked questions (FAQs)

These are some of the most common questions I encounter about accepting payments online for free.

Can I accept credit card payments for free?

All credit card payments come with an interchange fee charged by card networks (Visa, Mastercard, etc.), so there is no way to process credit card payments for free. However, you can opt to pass on most of the cost to your customers via adding a surcharge or offering a cash discount program. Alternatively, you can limit the cost of your transactions with the right payment services provider.

Is there an app that allows me to accept credit card payments?

All mobile payment apps are equipped with credit card processing tools by default. With a linked mobile credit card reader, you can choose from swipe, EMV chip, and contactless payment options. Even if you don’t have a card reader, you can still accept credit card payments via manual entry or digital wallet transactions.

What is the cheapest way to take credit card payments?

In-person or card-present credit card payments impose the cheapest transaction rates. This is because physical cards presented at the point of sale offer the least risk of fraud and chargeback claims. Meanwhile, ACH payments is the cheapest way to accept payments online.

Can I pass credit card fees to customers?

Sometimes, but only if you follow state laws, card-brand rules, and processor requirements.

Can I accept credit card payments without a website?

Yes. Use payment links, online invoices, QR codes, or hosted checkout pages.

What is the best free credit card processor for online payments?

There is no free processor, but Square, Stripe, PayPal, and Helcim are strong no-monthly-fee options depending on setup and sales volume.

Bottom line

Although there’s no way to accept credit card payments online for free, it’s possible to find an affordable solution. Minimize costs and streamline the entire process by choosing an all-in-one payment processor that will host your website and offer competitive payment processing.

Square is one of the most affordable and easiest-to-use solutions that offers everything you need to accept payments online, including a free payment processing account and a free website. Plus, you can add extra features as you grow and use its marketing solutions to help scale your business. Visit Square to create your free account.