- What is a virtual terminal?

- Choosing the best virtual terminal

- Best virtual terminals compared

- Square Payments: Best overall virtual terminal for small business

- Helcim: Best for B2B transactions

- Shopify Payments: Best virtual terminal for ecommerce

- Payment Depot: Best for low custom rates

- PayPal: Best for accepting international card payments

- Chase Payment Solutions: Best for free same-day funding

- Clover: Best virtual terminal for restaurants

- PaymentCloud: Best for high-risk businesses

- Virtual terminal fee calculator

- How to choose a virtual terminal in 5 steps

- Frequently asked questions (FAQs)

- Bottom line

What is a virtual terminal?

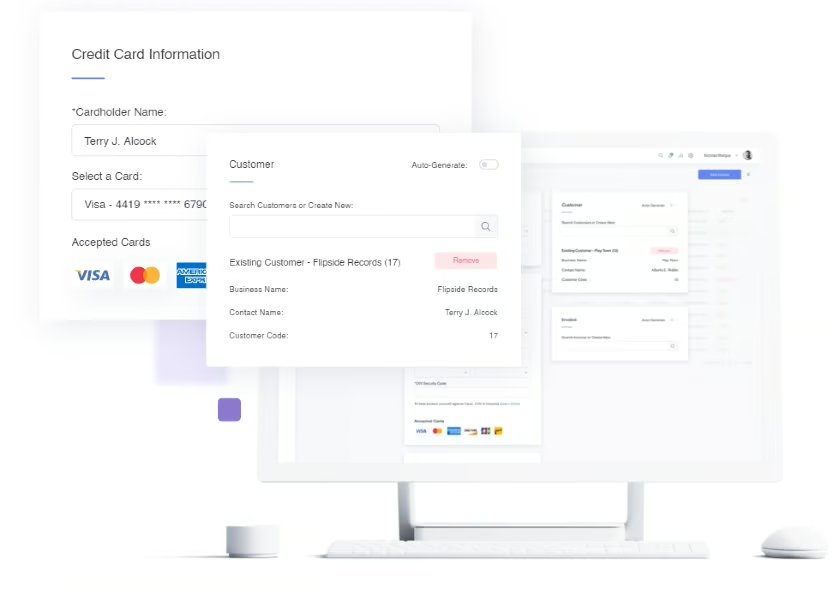

A virtual terminal is a secure, browser-based payment tool that lets businesses manually enter customer payment details, such as credit or debit card numbers, for processing. Unlike a physical card reader, it runs entirely online and requires no special equipment. This makes it especially useful for phone orders, email invoices, or remote billing scenarios.

According to a recent report, the global virtual terminal market is projected to grow by over 30% this year, from $17.85 billion to $23.48 billion, highlighting the rapid shift toward remote and digital-first payment workflows.

So, if you’re running a service-based business, boutique shop, restaurant, contracting company, or field service team, having the right virtual terminal platform means you can win over customers with a convenient checkout flow, get paid faster, and cut down on billing headaches.

Choosing the best virtual terminal

If you’re in the market for a virtual terminal solution, look for options that support payment methods your business needs, offer strong security, send professional invoices, and allow for easy recurring billing.

This guide compares popular virtual terminal providers for a wide range use cases to help you get started. My top picks combine ease of use, robust payment capabilities, and reliable customer support to keep your transactions seamless and secure, and your cash flow steady.

The best virtual terminals for 2025 are:

- Square: Best overall

- Helcim: Best for B2Bs

- Shopify Payments: Best for ecommerce

- Payment Depot: Best for low custom rates

- PayPal: Best for accepting international card payments

- Chase Payment Solutions: Best for free same-day funding

- Clover: Best for restaurants

- PaymentCloud: Best for high-risk businesses

Best virtual terminals compared

| Our Score(out of 5) | Minimum Monthly Fee | Keyed-in Transaction Fee | Supported Payment Methods | Payment Tools | |

|---|---|---|---|---|---|

| 4.28 | $0 | 3.5% + 15 cents |

|

|

| Visit Square | |||||

| 4.24 | $0 | Interchange plus 0.15% + 15 cents to 0.5% + 25 cents |

|

|

| Visit Helcim | |||||

| 4.16 | $5 | 2.5% + 30 cents to 2.9% + 30 cents |

|

|

| Visit Shopify Payments | |||||

| 4.05 | $0 | Interchange plus 0.2% to 1.95% |

|

|

| Visit Payment Depot | |||||

| 3.98 | $30 | 3.39% + 29 cents |

|

|

| Visit PayPal | |||||

| 3.94 | $0 | 3.5% + 10 cents |

|

|

| Visit Chase Payment Solutions | |||||

| 3.88 | $14.95 | 3.5% + 10 cents |

|

|

| Visit Clover | |||||

| 3.83 | $25 | 2.3% to 4.3% |

|

|

| Visit PaymentCloud | |||||

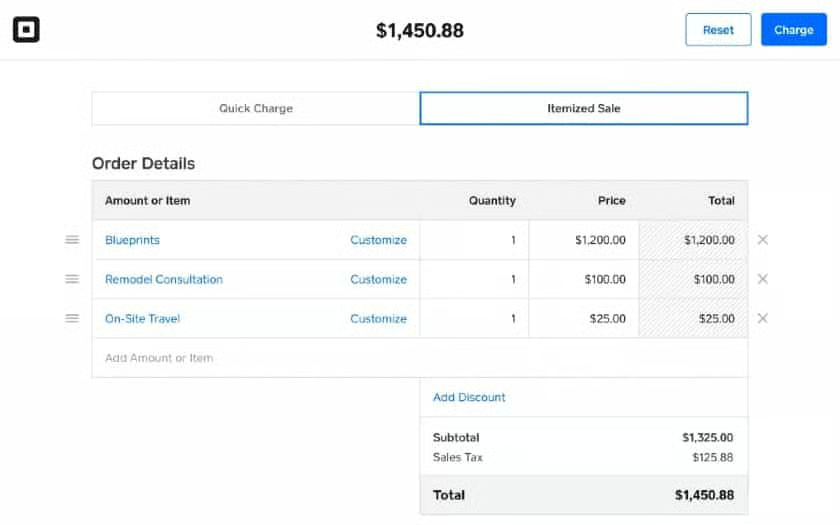

Square Payments: Best overall virtual terminal for small business

Who should use it:

Square Payments is ideal for small businesses that want an all-in-one solution that includes a free, built-in virtual terminal with their POS.

Why I like Square Payments:

Square Payments is Square’s built-in processor and powers the broader Square POS ecosystem. The virtual terminal is included with every Square account and supports nearly all common payment methods. It also checks the core boxes I expect: one-time and recurring billing, customer management, invoicing, and smooth web/mobile usage.

What I like most is how easy Square makes setup and day-to-day use. You can activate the virtual terminal right from your dashboard, send invoices, set up recurring payments, and manage customers without extra add-ons or complex configurations. You can even connect a card reader to lower your transaction fee. For small teams, that simplicity reduces admin time and gets you taking payments fast.

However, note that customer support hours are limited, Level 2/Level 3 data support is minimal (so B2B-optimized processing may require third-party integrations), and ACH is restricted to invoice payments (you can’t key bank details directly in the terminal). If you run high-volume keyed transactions, I recommend price-checking against Helcim or Payment Depot, which can be more cost-efficient at scale.

Also read: Top 9 Square Competitors

- Monthly subscription fee: $0

- Virtual terminal monthly fee: $0

- Keyed-in (virtual terminal) transaction fees: 3.5% + 15 cents

- In-person (swipe, dip, tap) transaction fees: 2.6% + 15 cents

- Invoice transaction fees: 3.3% + 30 cents

- Ecommerce transaction fees: 2.9% + 10 cents

- ACH/bank transfer fees: 1% with $1 minimum

- Free virtual terminal

- Feature-rich payment tools

- Native POS integration

- Built-in payment processing

- Free POS and Invoicing

- Next-day access to funds (same-day with fee)

- Waived chargeback fees

- Add-on services like appointments or payroll

- CBD program for businesses selling CBD products

Helcim: Best for B2B transactions

Who should use it:

Helcim is my pick for small to mid-sized B2B firms and SaaS platforms — think wholesale, automotive, healthcare, education, and other invoice-heavy operations — that want built-in fee optimization.

Why I like Helcim:

Helcim is a Canada-based processor with a strong reputation among SMB B2B merchants. Its virtual terminal covers the essentials, card and ACH acceptance, phone sales, invoices, and recurring billing, and you also get a mobile app plus a free POS that runs on your existing smartphone, iPad, or tablet.

What I like most is how Helcim automates cost optimization behind the scenes. Beyond clear interchange-plus pricing, it automatically applies volume-based discounts as businesses grow and supports Level 2 and Level 3 data processing to help US merchants qualify for lower interchange. In practice, that means better rates on many B2B transactions, without manual setup or constant oversight, making Helcim especially valuable if you process large or line-item-rich invoices.

That said, payouts can be slower than average, and Helcim primarily serves US and Canadian merchants. If you need faster deposits or plan to accept payments globally, Square and PayPal are better alternatives with quicker funding options.

- Monthly subscription fee: $0

- Virtual terminal monthly fee: $0

- Keyed-in (virtual terminal) transaction fees: From Interchange plus 0.15% + 15 cents to 0.5% + 25 cents

- In-person (swipe, dip, tap) transaction fees: From Interchange plus 0.15% + 6 cents to 0.4% + 8 cents

- Invoice transaction fees: From Interchange plus 0.15% + 15 cents to 0.5% + 25 cents

- Ecommerce transaction fees: From Interchange plus 0.15% + 15 cents to 0.5% + 25 cents

- ACH/bank transfer fees: 0.5% + 25 cents

- American Express cards: Additional 0.10% + 10 cents

- Free virtual terminal

- Free POS

- Excellent rates

- ACH transactions

- Tokenized card information

- Stored-card payments

- Recurring payment processing

- Mobile app with the virtual terminal

- Surcharging program

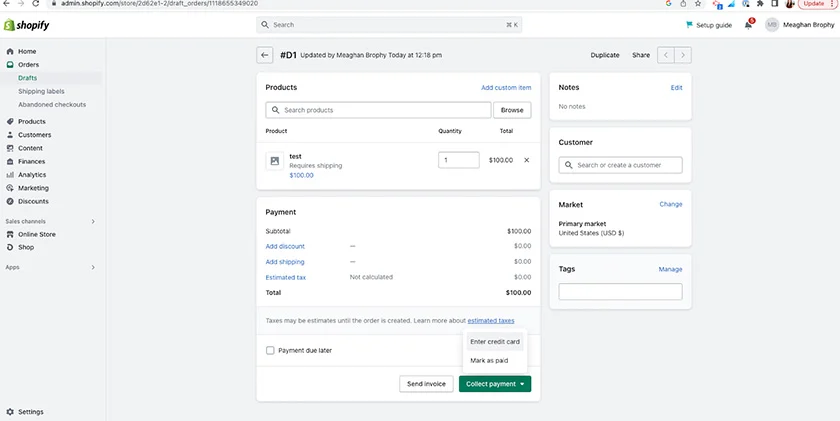

Shopify Payments: Best virtual terminal for ecommerce

Who should use it:

Shopify Payments is a strong fit for ecommerce-first and multichannel small businesses, online stores, social sellers, and storefronts that also take orders by phone or email.

Why I like Shopify Payments:

Shopify Payments is Shopify’s native processor, tightly integrated with the entire Shopify stack, your online store, checkout, admin, POS, and social sales channels. It includes a free virtual terminal for keying in card payments, plus robust order management for invoices, draft orders, and payment links. Shopify also supports multi-currency, so international sellers can be paid in their primary currency.

What I like most about Shopify is how seamlessly the back office and checkout work together for merchants who live in Shopify. Phone orders, email invoices, and keyed card payments all feed the same order, inventory, and customer records, so you’re not stitching together tools.

Add Shopify’s built-in social sales tools and access to B2B workflows with draft orders and invoicing, and you’ve got a clean end-to-end system for online and remote sales.

However, the virtual terminal is limited to credit cards (no keyed-in ACH directly in the terminal), and advanced features like B2B tools require a Shopify Plus subscription. If you need B2B fee optimization with Level 2/3 data or keyed-in ACH, Helcim is the better fit.

Also read: How to Accept Credit Card Payments Online

- Monthly fees:

- Starter: $5 (sell only through social media messaging)

- Basic: $39 billed monthly

- Shopify (Grow): $105 billed monthly

- Advanced: $399 billed monthly

- Transaction fees:

- Starter: 5% per transaction

- Basic: 2.9% + 30 cents online; 2.6% + 10cents in person

- Shopify (Grow): 2.7% + 30 cents online; 2.5% + 10 cents in person

- Advanced: 2.5% + 30 cents online; 2.4% + 10 cents in person

- Shopify Plus: Custom (high volume)

- Online/Keyed-in: 2.5% + 30 cents to 2.9% + 30 cents

- Native shipping and delivery management tools

- Multiple payment methods available for virtual terminal

- Itemized invoicing with customization tools

- Refundable chargeback fee

- $0 per transaction markup

- Integrates with Stripe

- Purchase orders payment processing

- Manual payment methods

- Multicurrency payment processing

- Social media payment processing

- B2B payments

Payment Depot: Best for low custom rates

Who should use it:

Payment Depot is a strong fit for established small businesses with steady volume that want custom interchange-plus pricing and the freedom to choose a virtual terminal that matches their workflow.

Why I like Payment Depot:

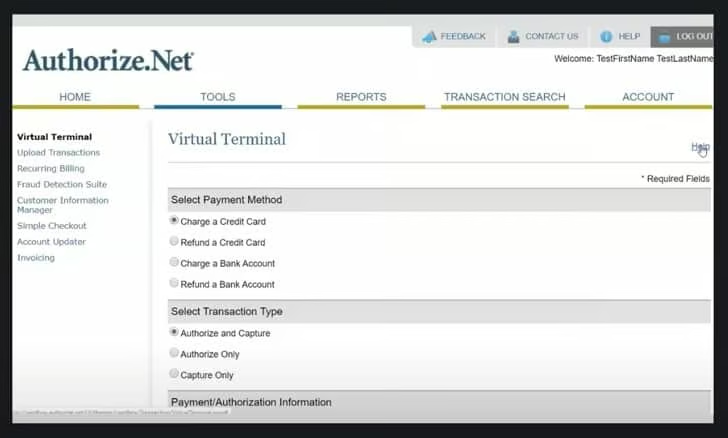

Acquired by Stax in 2021, Payment Depot is a more small-business-friendly alternative that offers custom interchange-plus rates with no monthly, setup, or cancellation fees. It seamlessly integrates QuickBooks and connects to a wide range of POS and business tools, including Clover.

What I like most is the blend of low custom pricing and platform flexibility. Unlike most providers in my list, I chose Payment Depot for its compatibility to integrate with a range of virtual terminal platforms, such as Authorize.net, SwipeSimple, PayTrace, and NMI, instead of locking you into a single terminal. This means you keep Payment Depot’s processing economics while picking the virtual terminal that fits your team, which is rare.

That said, because Payment Depot relies on third-party virtual terminals, setup can involve more moving parts than an all-in-one provider — for instance, Level 2 and 3 data processing benefits for B2Bs are tied to PayTrace rather than every terminal option. Custom pricing also tends to favor consistent or higher volumes. So, if you’re newer or your volume is low/variable, Square may be more cost-predictable. For built-in Level 2/Level 3 data handling, consider Helcim.

- Monthly subscription fee: $0

- Virtual terminal monthly fee: $0

- Transaction fees: Interchange plus 0.2% to 1.95%

- Interchange-plus pricing

- Choice of virtual terminals through Authorize.net, SwipeSimple, NMI, and more

- Sales staff helps you find the best terminals and POS systems for your business

- Multiple integrations

- Free equipment reprogramming

- B2B payments processing

- Business management integrations

- Responsive customer support

PayPal: Best for accepting international card payments

Who should use it:

PayPal is a strong fit for solopreneurs, freelancers, and small businesses with international customers, such as retailers in tourist areas, tour and experience operators, hospitality, pop-ups, and more.

Why I like PayPal:

PayPal is the world’s most recognized payment processor and plugs into almost anything — website builders, invoicing tools, and marketplaces. Its virtual terminal lets you key in most major cards and supports cross-border transactions. You also get PayPal’s free POS software, plus a mobile app for on-the-go sales.

I often recommend PayPal for low to moderate volumes where simplicity and global reach matter more than the absolute lowest processing rate. As a virtual terminal platform, PayPal allows you to accept payments in n 200+ currencies (with conversion), add quick payment buttons, and even offer installment options to customers. This makes it easy to handle phone orders while continuing to accept payments online, in-store, and via social channels.

The biggest downside to using PayPal’s virtual terminal is the monthly fee which essentially takes away the convenience of PayPal as a free payment processor. Also, flat-rate pricing can be costlier at scale, and currency conversion/cross-border fees apply. If you want lower effective rates for high-volume keyed transactions, look at Helcim or Payment Depot.

- Monthly fee: $0-$30

- Standard card-present fee: 2.99% + 49 cents

- Virtual terminal fee: $30 per month plus

- Standard: 3.39% + 29 cents

- Charity: 2.39% + 49 cents

- Payment gateway (Payflow): $0-$25/month

- Recurring billing: $10 per month

- Invoicing: 3.49% + 49 cents

- Chargeback fee: $20

- Chargeback protection: 0.4%-0.6% per transaction

- International payment processing

- Instant fund access through your PayPal account

- Peer-to-peer payments

- Low flat-rate in-person transaction fee with PayPal Point of Sale

- Integrates with hundreds of POS and third-party payment systems

- Easy-to-use platform

- Free POS and third-party integrations

Chase Payment Solutions: Best for free same-day funding

Who should use it:

Small businesses that prioritize fast access to funds and want an enterprise-grade virtual terminal backed by a major US bank. It’s especially appealing if you already have, or are open to opening, a Chase business bank account.

Why I like Chase Payment Solutions:

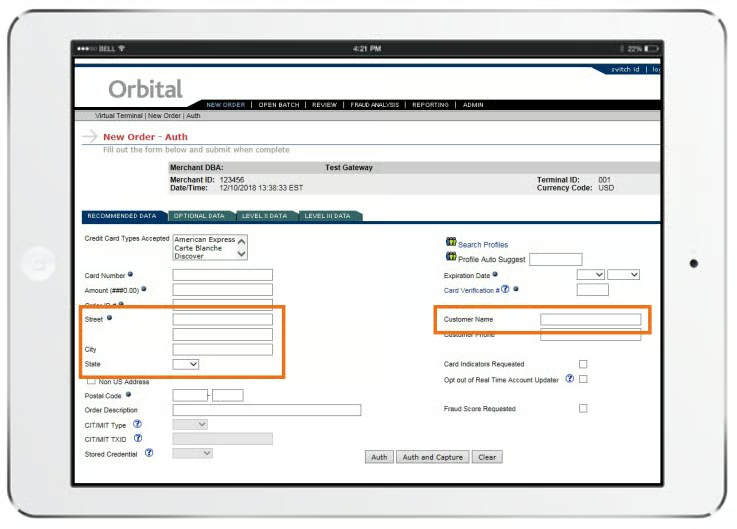

Chase Payment Solutions is the merchant services arm of JPMorgan Chase, offering end-to-end payment processing across in-store, online, and mobile channels. Its lineup includes the Orbital® Virtual Terminal (Chase’s proprietary, browser-based terminal) and support for Authorize.net, giving you multiple ways to handle keyed and remote payments under one umbrella.

What makes Chase unique is the funding speed — and that it can be free. If you direct card payments to a Chase business checking account and use QuickAccept®, you can receive same-day funding at no additional cost. I also like how Chase gives you a choice to run Orbital for deep gateway features and reporting, or plug in Authorize.net if that’s your team’s comfort zone.

Orbital also supports advanced workflows (refunds, detailed reporting; and documentation references shipment-level controls), which helps if your orders aren’t one-and-done. That said, note that opening a Chase business checking account comes with a $15 monthly service fee unless you meet a $2,000 minimum daily ending balance or other qualifying activities. Consider PayPal for free, instant access to your funds.

Also read: 10 Best Merchant Services

- Monthly fee: $0

- Virtual terminal fee: Not disclosed

- Online fee: 2.9% + 25 cents

- In-person fee: 2.6% + 10 cents

- Keyed-in fee: 3.5% + 10 cents

- ACH processing:

- Real-time deposits: 1% (capped at $25), nonreversible

- Same-day deposits: 1% (capped at $25), reversible

- Standard deposits (1-2 business days): $2.50 for the first 10 transactions, 15 cents for additional, reversible

- Chargeback fee: $25-$100

- Backed by trusted payment processor

- Offers advanced analytics tools

- Processes e-checks

- Split payments, refunds, account histories

- Choose between Chase’s native virtual terminals, Orbital and Authorize.net

- Also works with non-Chase business bank account holders

- B2B payment processing

- Free same-day funding

Clover: Best virtual terminal for restaurants

Who should use it:

Restaurants, cafés, bars, food trucks, and caterers that need a POS-first system with a built-in virtual terminal for phone orders, deposits, private events, and remote payments from the same dashboard.

Why I like Clover:

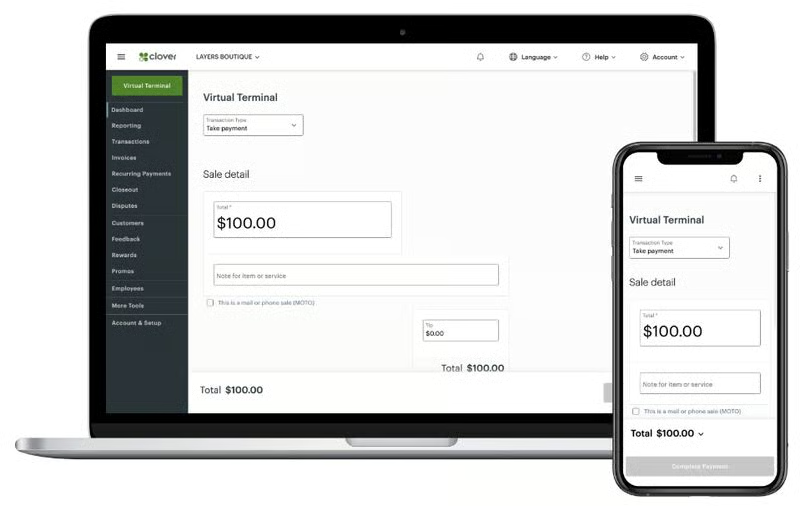

Clover is popular as a restaurant payment solutions provider, making it highly suitable as a virtual terminal for restaurants to accept payments over the phone, via invoice, and through remote transactions. It offers a flexible and convenient solution for managing takeout and delivery orders.

Clover’s virtual terminal integrates seamlessly with its broader POS system, providing comprehensive features such as menu management, kitchen displays, customer relationship management (CRM), and employee management. These features provide a complete solution for front-of-house and back-of-house operations.

It is also available through various payment processors, which means rates and contracts may vary across different providers.

“There’s rarely an instance where a restaurant would use a virtual terminal if they don’t already have a point-of-sale (POS) system. With a POS, you just manually key the card information into the POS payment screen if you need to process invoices, deposits, or private-party transactions. Whether you simply want a virtual terminal to invoice catering clients or you need a full-blown restaurant POS that supports in-person and virtual transactions, Clover is a solid choice.”

Mary King

Restaurant Expert

Also read: Best Clover Alternatives & Competitors

- Monthly fee: $14.95 (virtual terminal only)

- Virtual terminal fee: $0

- Transaction fee: 3.5% + 10 cents

- Payment requests/simple invoicing

- Card-on-file support

- Optional tipping

- Recurring payments

- Online customer payments page

- Reporting tools

- Fraud prevention tools

- 1- to 3-day standard payout speed with 1.5% fee for instant payout

PaymentCloud: Best for high-risk businesses

Who should use it:

High-risk and hard-to-place merchants, including MOTO (mail/phone order), subscription services, ticketing/travel, nutraceuticals, and other categories with higher chargeback exposure, who need a virtual terminal.

Why I like PaymentCloud:

PaymentCloud is a US-based merchant services provider known for placing high-risk businesses through a network of acquiring banks and gateways. Unlike one-size-fits-all processors, it can support interchange-plus, flat-rate, or tiered pricing, and matches you to a banking partner that fits your model and volume.

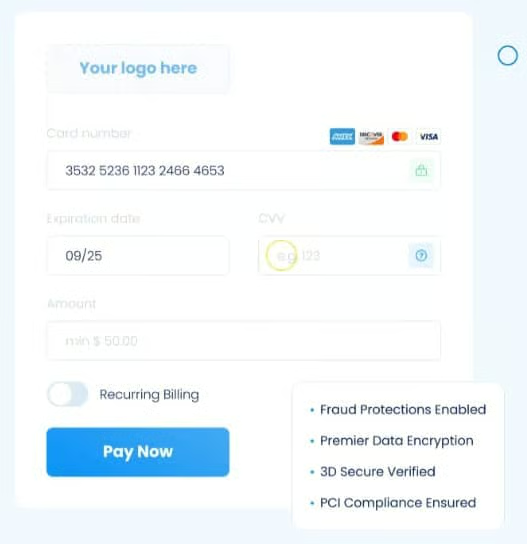

What I like most is how it packages the virtual terminal with risk-minded controls. You get PCI compliance, fraud tools, data encryption, and 3-D Secure (Visa/Mastercard), plus AVS/CVV checks and other verifications that are crucial for card-not-present sales. The virtual terminal supports simple invoicing, recurring payments, and digital receipts (note: no itemized sales in the virtual terminal), and it plays well with CRMs like Salesforce to keep customer and payment data aligned.

Designed to connect with CRM software like Salesforce, PaymentCloud offers a seamless integration process for enhanced CRM. On the other hand, underwriting can take longer than with plug-and-play options (e.g., Square, PayPal), and final rates/terms vary based on your risk profile. If you’re not truly high-risk and primarily want transparent, automated fee optimization (e.g., Level 2/3 for B2B), Helcim is a better fit.

Also read: 6 Best High-Risk Merchant Account Providers

Note that PaymentCloud offers custom pricing. The fees listed below is based from quote provided by PaymentCloud.

- Monthly fee: $10-$45

- Virtual terminal: $15-$45 per month

- Medium-risk transaction fee: 2.3%-3.4%

- High-risk transaction fee: 2.7%-4.3%

- Payment gateway fee: $15 per month (average)

- Chargeback fee: $25

- Early termination fee: Waived

- Advanced payment security tools

- Multiple virtual terminal options supported

- Integration with popular POS

- Invoices and recurring sales supported

- Flexible pricing structure

- Gateway agnostic

- Custom fraud protection

- Waived early termination fees

- CRM integrations

Virtual terminal fee calculator

Compare your estimated monthly fees for each of my top picks:

Virtual Terminal Payment Processing Calculator

How to choose a virtual terminal in 5 steps

Choosing the right virtual terminal depends on your business’ payment needs and your sales volume. Here is a quick guide to choosing a virtual terminal for your business:

Step 1: Identify your virtual payment needs

Like most payment methods, it’s important to find virtual terminals that complement your business model and give you the most value for your money. The best virtual terminal credit card processing provider should be able to process different payment methods and transaction types.

Some key features to consider include the following:

- Payment methods: Credit and debit cards, ACH, e-checks, wire transfers, gift cards, digital wallet payments, buy now, pay later (BNPL)

- Payment types: Invoicing, stored card, recurring billing, payment links, level 2 and level 3 data processing, multicurrency

- Payment security: PCI security, tokenization and encryption, fraud protection tools

Make a list of potential payment processors that offer the payment tools you identified above.

Step 2: Consider your sales volume

Payment processors typically structure their fees based on merchant sales volume, so knowing your business’s monthly or annual average will allow you to get customized quotes and rates from the virtual terminals you are considering.

Having these rates will help estimate the cost of doing business with each option.

Step 3: Look for essential virtual terminal features

Use the following non-negotiable features as your shortlist filter:

- Payments & billing essentials

- Multiple payment methods: Major cards, ACH/bank transfer, and digital wallets if available.

- Invoicing + payment links: Send branded invoices, itemize charges, add tax/shipping, and include secure pay-now links.

- Recurring billing & subscriptions: Flexible schedules, proration, trial periods, and easy pause/cancel controls.

- Partial authorizations, voids, and refunds: Handle deposits, adjustments, and quick error fixes without support tickets.

- Security & risk controls

- PCI compliance plus tokenization & encryption: Protect card data end-to-end.

- Fraud tools: AVS/CVV checks, velocity limits, block/allow lists, IP/geolocation rules, and optional 3-D Secure.

- Role-based permissions & audit logs: Limit who can key cards, issue refunds, or view reports.

Step 4: Compare virtual terminal fees

Virtual terminal processing rates are often higher because they usually apply the keyed-in rate, which is 3.5% plus 10 cents to 15 cents per transaction. You will also need to consider any monthly fees, such as for account maintenance and (sometimes) for accessing the virtual terminal platform. To help you get started, use the calculator below for an estimate of your monthly merchant payment processing fees with our recommended providers.

Looking for other ways to accept payments remotely? Check out our list of best payment gateways and leading mobile point-of-sale applications.

Step 5: Choose a provider and sign up for a merchant account

Once you find your chosen virtual terminal, it’s time to apply for a merchant account to access this service. The ease or complexity of this process depends on the service provider and the merchant account type it offers. Note that most of the providers on our list are ideal for small businesses and do not require an application process—you just need to sign up for a merchant account.

Download our complete guide to signing up for a merchant account.

How I evaluated the best virtual terminals

Frequently asked questions (FAQs)

Here are some questions I often encounter about virtual terminals.

Which virtual terminal is best for small businesses?

It depends on your mix of sales: third-party roundups often name Square as the best all-around pick for small businesses, while Helcim stands out for B2B cost optimization and Shopify Payments for ecommerce-first brands.

Is there a free virtual terminal (included with my account)?

Yes, several providers include a virtual terminal with no extra monthly software fee. For example, Square’s virtual terminal has no monthly fee (you just pay processing). Many guides note that some processors include the virtual terminal for free, while others charge a subscription.

Which virtual terminals support ACH/eCheck and recurring billing?

Helcim supports ACH in the virtual terminal, invoices, and subscriptions; Square supports ACH via invoices (not by keying bank info directly in the virtual terminal) and offers recurring billing via Card on File/Invoices. Check your provider’s docs for specifics.

What’s the difference between a virtual terminal, a payment gateway, and a POS?

A virtual terminal is a staff-facing browser screen for manually keying payments; a payment gateway moves payment data from a customer-facing checkout to the processor; a POS handles card-present sales and in-store workflows. Many businesses use both a gateway and a virtual terminal.

Bottom line

Virtual credit card terminals are a great addition to any business, allowing you to take orders over the phone or by email. Most payment processors offer these for free or with a small monthly fee. The best ones handle multiple payment types, including cryptocurrency and ACH transfers, and have some form of fraud or chargeback protection beyond PCI compliance.

For small businesses, I find Square offers the overall best virtual terminal credit card processing service in the industry. It provides reasonable rates, has a free POS system, and is super easy to use. Its wide range of products also makes it a solid choice for growing businesses, and it’s free. You only pay a by-transaction rate. Sign up for Square today.