Merchant services, also referred to as payment processors, are a necessary but frustrating part of running a business. We list 10 providers that offer fair and transparent pricing

10 Best Merchant Services for 2025

Download our Merchant Account Application Guide

This article is part of a larger series on Payments.

Merchant services The main role of a merchant services provider is to set up merchant accounts that businesses need to start accepting credit cards and other types of payments. This is why merchant services providers are also often called payment processors even though there are some differences in the type of merchant account they provide. Learn more about merchant accounts. allow businesses to accept credit and debit card payments. Many also offer additional tools, such as payment gateways, virtual terminals, and point-of-sale (POS) systems. The best solutions offer competitive rates, month-to-month contracts with no cancellation fees, and flexible solutions for processing in-person and online transactions.

If you’re in the market for a new merchant services solution, I evaluated 34 providers based on 23 data points to provide you with my best recommendations.

The best merchant services for 2025 are:

- Square: Best overall

- Helcim: Cheapest merchant services provider

- Payment Depot: Best for growing businesses

- Chase Payment Solutions: Best direct processor

- Stax: Best for large-volume businesses

- QuickBooks: Best for QuickBooks users

- U.S. Bank Merchant Services: Best for same-day funding

New customers who open a payment solutions account with U.S. Bank can get merchant account fees of up to $1,000 refunded over three months. Member FDIC.

To qualify, the new U.S. Bank Payment Solutions Merchant Account (MID) must be (1) opened and approved by June 30, 2025, and (2) kept open and actively accepting and settling card payments at the time monthly statement credits are applied.

- PaymentCloud: Best for high-risk merchants

- PayPal: Best for flexible checkouts

- Stripe: Best for online payments

Note that there are several pricing structures for merchant account providers. To truly compare pricing side-by-side, you should request a quote or use a tool like our calculator below

Best merchant services compared

Our Score (out of 5) | Monthly Fee | Swipe/Chip Transaction | Chargeback Fees | |

|---|---|---|---|---|

4.49 | $0-$165 (with POS) | 2.6% + 15 cents | Waived up to $250/month | |

4.44 | $0 | From interchange + 0.15% + 6 cents | $15 refundable | |

4.43 | $0 | Custom quote (Interchange + 0.2%-1.95%) | $25 | |

| 4.10 | $0 | 2.6% + 10 cents | $25 |

4.04 | $99-$199 | Interchange + 8 cents | $25 | |

3.96 | $0-$35 | 2.5% | $25 | |

3.93 | $0-$99 | 2.6% + 10 cents | $35 | |

3.92 | $10-$45 | 2%-3.5% | $25-$45 | |

3.86 | $0-$30 | 2.29% + 9 cents | $20 | |

3.84 | $0 | 2.7% + 5 cents | $15 refundable | |

Enter your typical monthly sales volume and average order value or ticket size to see how much you would pay each month with each processor, along with your effective rate:

I have over seven years of experience testing and reviewing payment processing technology, merchant services, and POS systems. To evaluate the best merchant services, I fact-checked each provider to ensure that pricing and features were accurate. I then scored each one on 23 data points prioritizing value for money and ease of use. See my full methodology below.

Retail Staff Writer at Fit Small Business

Square: Best overall merchant services provider

Overall Score:

4.49 / 5

Pros

- Transparent, predictable pricing

- Free, user-friendly software & card reader

- No application, contract, monthly fees, or minimum requirements

Cons

- Can only be used with Square POS

- Limited or inconsistent support

- Interchange-plus rates only for large enterprise clients

Overview

Who should use it:

Small businesses that want low fees and a free subscription, a flexible set of features, compatibility with many industries, and easy setup and use will find Square a great fit.

Why we like it:

Square is an all-in-one merchant services provider, meaning it can process payments in-store and online as well as via mobile, virtual terminal, invoice, and even quick response (QR) code. The simplest merchant account provider to get started with, Square is free to use except for pay-as-you-go transaction fees.

Easy, low-cost, and flexible merchant services, combined with the best free POS software, make Square the best value for new and small businesses that want lots of payment options, easy setup, and low fees. It is also our leading free merchant account and our top choice among retail credit card processors.

As soon as you create your free Square account, you can accept credit card payments, record cash and check sales, process invoices, set up an online checkout or ordering system, and accept contactless payments.

- Monthly fee: $0 to $165

- Card-present transaction fee: 2.6% + 15 cents

- Ecommerce and invoice transaction fee: 2.9% + 30 cents

- Card-not-present transaction fee: 3.5% + 15 cents

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: Waived up to $250 per month for chargeback protection

- Card reader: $59

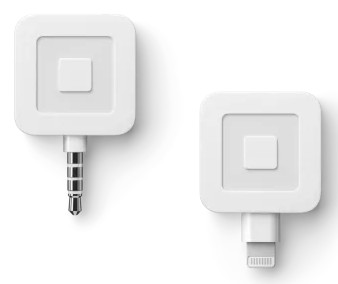

Magstripe Reader | Contactless and Chip Reader | Square Terminal |

|---|---|---|

|  |  |

First free, additional $10 | $59 | $299 or $27 per month for 12 months |

Accepts payments via magstripe (swiped), available in jack or lightning connector. | Bluetooth reader that accepts EMV (chip), and near-field communications (NFC), such as Apple Pay and Google Pay payments. Optional countertop dock and phone case mount. | Stand-alone mobile POS that can take orders, accept card payments, and issue receipts with built-in printer. |

- Free plan and affordable upgrades: Square has a forever-free plan that contains lots of tools for point of sale, ecommerce, and payments. If you decide to upgrade, higher plans are within reach even for small and new businesses.

- Multiple payment methods and services: Square gives you great flexibility in accepting various payment methods. Customers can buy and pay via credit card (in-person and via manually-keyed payments), through online stores and social media, ACH bank transfers, buy now, pay later (BNPL), recurring payments, and more. Square also has an online CBD program that lets you sell hemp and hemp-derived products — something unique among the providers in this guide.

- Chargeback policy: Square waives up to $250 per month for chargeback disputes — a generous policy compared to other merchant services.

- Affordable hardware: Square hardware covers a wide range of prices and devices, so you’re sure to find what you need. You get one free card reader upon signing up, and financing is available for most hardware purchases.

Related reading:

Helcim: Cheapest merchant service provider

Overall Score:

4.44 / 5

Pros

- Interchange-plus pricing with no monthly fee

- Free POS, customer relationship management (CRM), invoicing, and online store software

- Options to pass processing fees onto customers

Cons

- Limited third-party integrations

- Charges extra for Amex transactions

- Strict approval process

Overview

Who should use it:

Helcim is for seasoned business owners of all sizes, familiar with transaction rates and looking to minimize credit card processing costs. It offers dedicated tools for B2Bs, wholesalers, and professionals in the healthcare, education, and automotive industries.

Why we like it:

Helcim is a traditional merchant account service provider that provides businesses with a wide range of payment processing features. The system is popular among merchants for its built-in automated volume discounts and free business tools. In addition to its primary functions, Helcim also comes with a POS app, subscription management tools, and an online payment gateway.

But what makes Helcim stand out the most is its fee-optimization features. Helcim does not charge a monthly fee, and access to its invoicing, subscription management, and payment gateway tools are free. What’s more, every Helcim merchant is pre-approved to use its online and in-person surcharging features. Helcim can also recognize B2B transactions and will automatically collect the necessary information so your business can qualify for B2B discounted fees.

That said, it’s important to know that as a traditional merchant account provider, Helcim’s merchant account requirements are stringent. Unlike with Square, businesses will go through an application process that first-time merchants may find challenging to navigate.

Read our guide to merchant accounts to learn more about dedicated or traditional merchant accounts (like Helcim) vs payment facilitators (like Square).

- Monthly fee: $0

- Card-present transaction fee: From interchange plus 0.15% + 6 cents

- Card-not-present transaction fee: From interchange plus 0.15% + 15 cents

- American Express transaction fee: 0.10% + 10 cents

- Tap-to-pay on iPhone: + 10 cents per transaction

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $15 per lost dispute

- Card readers: $99

- POS terminal: $329

Helcim also has a free credit card processing program called Helcim Fee Saver, which allows merchants to pass processing fees over to customers via a surcharge or convenience fee.

Card Reader | Smart Terminal |

|---|---|

|  |

$99 | $329 ($30/month x12) + $50 (optional stand) |

Tap, Chip & PIN transactions | Standalone device with built-in POS app, tap, chip, and PIN-enabled transactions |

- Automated volume discounts: If your business processes high volumes and you need discounted rates, Helcim is a great choice. Helcim reduces your fees as your processing volume goes up; what’s more, the provider does this automatically, without you needing to call and negotiate for lower rates.

- Great pricing terms: Helcim gives you zero monthly fees, interchange-plus pricing, volume discounts, and refundable chargeback fees. In terms of sheer financial savings, few other providers have such attractive offerings.

- Free credit card processing: Helcim’s Fee Saver feature lets you accept credit card payments while paying no processing fees on your end. You can opt to pass these fees onto customers if they pay via credit cards, rather than other methods, such as ACH payments or cash. The Fee Saver feature applies for both in-person and online payments, and customers are informed of this extra fee on their invoices and receipts.

Related reading:

Payment Depot: Best for growing businesses

Overall Score:

4.43 / 5

Pros

- Custom interchange-plus rates

- No contract or cancellation fee

- 24/7 customer support

Cons

- Next-day funding available with fee

- ACH payment is an add-on service

- US merchants only

Overview

Who should use it:

Payment Depot is suitable for growing businesses, looking for a customized, all-in-one payment processing service.

Why I like Payment Depot:

Like Helcim, Payment Depot offers zero monthly fees and interchange-plus transaction rates. But, while Helcim excels in fee optimization, Payment Depot stands out for its customization. It supports both in-person and online transactions, as well as virtual terminal, invoicing, payment gateway, and subscription management. Payment Depot is a better option than Helcim if you need better integration capabilities, especially with popular POS software.

Payment Depot also benefits from its parent company, Stax. Payment Depot merchants looking to scale with surcharging, subscription management tools, and developer-based upgrades can be seamlessly transitioned. There are no long-term contracts and you get 24/7 support.

Note, however, like Helcim, Payment Depot is a traditional merchant account service provider, which means an application process and stricter terms for new and micro businesses. Deposit time is also much slower, with next-day funding available for a fee.

- Monthly fee: $0

- Transaction fees: Custom-quoted (variable rates from around 0.2% to 1.95%)

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: From $49

- Other fees: Payment Depot will charge a $19.99 monthly fee for Payment Card Industry (PCI) non-compliance if you do not keep your business compliant

Payment Depot has a wide selection of card readers available, including mobile and countertop solutions from popular brands like Clover, Poynt, and SwipeSimple. Those hardware items have quote-based pricing.

Mobile Card Reader | Smart Terminals | POS Hardware |

|---|---|---|

|  |  |

Swipe Simple B250 | Clover and Dejavoo | Clover |

- Interchange-plus pricing: Interchange-plus pricing, as opposed to flat-rate processing fees, can often result in long-term savings for your business. Call Payment Depot to get a custom processing rate quote; this allows you to negotiate good rates for your business.

- High-quality virtual terminal: This virtual terminal can handle high-volume businesses and accept both in-person and online card payments (plus card-not-present transactions and digital wallets). You can use the virtual terminal as long as you have a subscription with Payment Depot, and you’ll get access to your funds within 24 to 48 hours when using it.

- Business funding: Users can apply for business funding via Payment Depot. Certain requirements, such as minimum FICO scores and monthly revenues, will need to be met.

Related reading:

Chase Payment Solutions: Best direct processor

Overall Score:

4.10 / 5

Pros

- Same-day funding for Chase Business Checking customers

- Negotiable rates

- Leverages all Chase network data to offer business insights

Cons

- Some plans require long-term contracts

- Not all pricing disclosed on website

- Best value for Chase banking customers

Overview

Who should use it:

Chase Payment Solutions is suitable for businesses that have existing accounts with Chase, prefer some negotiating power with rates, or want strong business analytics tools to go along with their merchant services.

Why I like Chase:

Chase Payment Solutions (formerly Chase Merchant Services) offers merchant services for any business looking to work with a traditional bank, especially if your business accounts are with Chase. It is one of the few direct processors that offer flat-rate fees for small businesses. Larger businesses can also negotiate competitive interchange-plus pricing like you’d find with Helcim.

What I like about having Chase as both the processor and receiving bank is the speed and security of funding transactions by removing the intermediary. With a checking account, you can access Chase QuickAccept, a free mobile payments app that includes same-day deposits and dispute management. In addition, Chase provides its own payment gateway and virtual terminal solution but can still integrate with a number of popular payment gateway platforms.

For new merchants still looking for a business checking account, particularly those looking to sell internationally and online, Chase is an ideal solution. However, its card transaction rates may be better suited for low-volume businesses so unless your business relies heavily on crossborder sales and ACH payments, you will likely be better off with Helcim or Payment Depot.

- Monthly fee: $0

- Card-present transaction fee: 2.6% + 10 cents

- Card-not-present transaction fee: 3.5% +10 cents

- ACH processing fee:

- Real-time deposits: 1% (capped at $25), non reversible

- Same-day deposits: 1% (capped at $25), reversible

- Standard deposits (1 business day): $2.50 for the first 10 transactions, 15 cents for additional, reversible

- Contract length: Most plans are month-to-month

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: From $49

Chase Smart Terminal* | Countertop Terminal | Mobile Terminal | Chase QuickAccept Mobile Card Reader* |

|---|---|---|---|

|  |  |  |

$499 | $299 | $399 | $49 |

Wireless, Wi-Fi-enabled credit card terminal with digital and email receipts, transaction search, and more. | Ethernet or Wi-Fi connection with 24/7 support. Color screens with tipping functions and built-in receipt printers. | Same as the countertop terminal, but with a mobile battery that can power 450 transactions between charges. | Use the Chase Mobile app and optional card reader to accept swipe, chip, and contactless payments on the go. |

- Same-day deposits: Chase offers same-day deposits depending on the type of service you use—with no additional costs. Few other merchant services provide this turnaround speed.

- Customer insights: Chase software includes business analytics tools that monitor sales data, trends, customer information, and competition analysis. These insights provide actionable data you can use to zero in on high-potential business opportunities.

- Comprehensive support: You’ll get 24/7 live support, plus online guides and resources.

Related reading:

Stax: Best for large-volume businesses

Overall Score:

4.04 / 5

Pros

- Membership model interchange-plus pricing

- User-friendly software

- Unique add-on tools

Cons

- Pricey software packages

- Lacks same-day funding options

- ACH payments and next-day funding with fee

Overview

Who should use it:

Businesses with regular large transaction volume to benefit from Stax’ wholesale pricing as well as those that primarily collect payments through invoicing; businesses with recurring billing.

Why I like Stax:

Stax (formerly Fattmerchant) is a traditional merchant account services provider with dedicated solutions for all types of businesses, as well as SaaS platforms. It supports a complete range of payment processing solutions including advanced features for B2B transactions, credit card surcharging, and subscription management.

Some businesses may balk at Stax’s high membership pricing, but the wholesale rates and all-in-one access make up for the monthly cost. This pricing model allows large-volume businesses to lower their effective rate and keep more of their earnings. Stax also offers custom pricing options to its enterprise-level clients. It even offers short message service (SMS) text-to-pay solutions and robust reporting, which are also not common offerings.

Compared to Helcim, Stax is more versatile because it integrates readily with popular ecommerce, POS software and hardware, and other business solutions. However, Stax also requires a merchant application process that’s best for established businesses.

- Monthly fee: $99-$199 (depends on processing volume and software packages)

- Card-present transaction fee: Interchange plus 8 cents

- Card-not-present transaction fee: Interchange plus 15 cents

- Contract length: Month-to-month, 30 days’ notice to cancel

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: Custom quote

Stax hardware is custom-quoted. A selection of BBPOS mobile readers, Z terminals, and PAX terminals are available. We have previously been quoted $100 for mobile readers, $175 to $300 for Z terminals, and $500 to $650 for PAX models. These are available for purchase for a one-time fee, or through monthly fees with protection plans.

Mobile Card Reader | Smart Terminals | POS Hardware |

|---|---|---|

|  |  |

Swipe Simple B250 | Clover and Dejavoo | Clover |

- Stax Pay: Stax Pay is an all-in-one business management platform with which you can accept multiple payment types and access other business tools, all on a single dashboard. With Stax Pay, you can take in-person card payments, digital wallet payments, mobile device payments, and online payments via several gateways. You can also create payment links and buttons for your websites.

- Surcharging: CardX by Stax is a surcharging solution that lets you keep 100% of every credit card sale — no more losing out on profits due to fees. Your customer can choose whether to pay via credit (in which case they pay the fee themselves) or debit card (meaning you will pay the fee yourself). In either case, legal compliance via the CardX system is automatic.

- Recurring billing: Stax Bill is an automated payments and subscription service with Stax. You can set up an automated recurring billing schedule for your customers, which saves your business lots of time and headaches. The self-service portal allows customers to register and then monitor their own subscriptions so that you don’t have to. The system can also accept payments — including different currencies — via multiple gateways. This is different from the Stax Pay recurring invoice feature, which sends customers automatic invoices (which may involve varying rather than predictable payment amounts) on a schedule.

Tip: There is more than one way to decide which is the cheapest credit card processor. Check out our guide to 9 of the cheapest credit card processing companies in 2025.

QuickBooks: Best for QuickBooks Users

Overall Score:

3.96 / 5

Pros

- Option for free plan without the accounting software

- Invoicing and recurring billing tools, including ACH payment processing

- Seamless integration with QuickBooks accounting

Cons

- Requires paid plan to accept card-present payments

- Only scalable if you sign up for a QuickBooks online account

- Not ideal for high-volume of card-present transactions or ecommerce payments

Overview

Who should use it:

Businesses that are already using QuickBooks online and those looking for a free business bank account.

Why I like QuickBooks Payments:

QuickBooks is primarily an accounting software, with a payment processor that also offers both a merchant account and a free business bank account. One of QuickBook’s best updates is that merchants no longer need to sign up for a paid software plan to use its payment processing service. And because the system is highly compatible with most POS solutions, this opens up QuickBooks payments to a wider range of target users.

An independent QuickBooks payments account is best for online sellers and professionals. There are no monthly fees, and it comes with an online credit card payment processing feature, as well as an ACH payment method and invoicing tools. However, the free plan does not support card-present transactions, which means you’ll need a paid QuickBooks payment and QuickBooks accounting plan to accept in-person transactions.

QuickBooks’ rates are similar to that of Square, but the former gives you more POS software options to work with. That said, both providers’ flat fees are only ideal for low-volume businesses; if you need better rates for growing transactions, consider Helcim, Payment Depot, or Stax instead.

- Monthly fee:

- QuickBooks Money: $0 (QuickBooks Payments without an account software plan)

- QuickBooks Solopreneur: $20/month (+QuickBooks online plan $35-$235/month)

- QuickBooks Simple Start: $35/month (+QuickBooks online plan $35-$235/month)

- Card-present transaction fee: 2.5%

- Invoice transaction fee: 2.99%

- Keyed-in transaction fee: 3.5%

- ACH transaction fee: 1%, $1 min

- Instant funding: 1.75%

- Contract length: None

- Early termination fee: $0

- Chargeback fee: $25

- Card readers: From $49

QuickBooks Card Reader |

|---|

|

$49; $79 with Power Stand |

Accept EMV chip, debit, credit, Apple Pay, and Google Pay payments. Connects wirelessly to phone or tablet via Bluetooth for the QuickBooks GoPayment app. Stays charged for up to a week. |

QuickBooks offers a single mobile card reader option that is compatible with QuickBooks’ GoPayment mobile app. Countertop pin pads were previously available through QuickBooks POS, but the QuickBooks POS product has been discontinued.

You can also accept payments directly through the QuickBooks Online accounting software by sending an invoice or manually keying in the payment. Learn more in our tutorial on how to enter credit card transactions in QuickBooks Online.

- Mobile app/virtual terminal: QuickBooks’ mobile app lets you accept payments in person, by keying in card details. You can also use a mobile card reader with your smartphone, so you can accept tap payments as well.

- Accounting software: QuickBooks is known for its robust accounting software and tools. The software includes features such as income and expense tracking based on classes and locations, industry-specific customization, data sharing for tax professionals and accountants, and an advisor network.

- Integrations: You’ll have access to lots of third-party integrations that increase functionality, such as Amazon, PayPal, Square, and Shopify. If you need integrations specifically for credit card processing, these are available for you as well.

Related reading:

U.S. Bank Merchant Services: Best for same-day funding

Overall Score:

3.93 / 5

Pros

- Same-day funding

- Hardware rentals

- Surcharging and debit card optimization programs

Cons

- Limited user reviews

- Need to call for consultation on full feature set

Overview

Who should use it:

U.S. Bank Merchant Services is ideal for most business types, including retail, restaurants, services, and mobile businesses that want same-day funding.

Why I like U.S. Bank Merchant Services:

U.S. Bank is a large banking institution with a variety of business products including its own merchant services arm. It provides a traditional merchant account with the ability to accept credit cards and ACH payments, plus invoicing and website building tools. Every merchant also gets a dedicated account manager, fraud protection, comprehensive sales reporting tools, and 24/7 support.

Like Chase, U.S. Bank Merchant Services provides same-day funding for merchants with a U.S. Bank business account. However, with U.S. Bank’s Everyday Funding feature, you can receive your funds seven days a week. Additionally, U.S. Bank Merchant Services supports paper check processing (via remote deposit capture), and even surcharging, which you won’t find in Chase.

While its primary advertised fees are flat-rate, U.S. Bank Merchant Services can provide custom processing. So, it’s possible to compare potential costs against providers like Helcim, Payment Depot, and Stax.

- Mobile: $0

- Unlimited users

- Up to 100 products

- Starter: $29+ per month

- Unlimited users

- Up to 500 products

- Standard: $69+ per month

- One-time set-up fee of $99

- Unlimited users and products

- Good for retail shops and small restaurants

- Premium: $99+ per month

- One-time set-up fee of $99

- Unlimited users and products

- Good for large restaurants and multi-location businesses

- Processing fees:

- In-person transactions: 2.6% + 10 cents

- Keyed-in transactions: 3.5% + 15 cents

- Online transactions: 2.9% + 30 cents

Mobile card reader | Handheld POS terminal | POS Register |

|---|---|---|

|  |  |

Pair with a smartphone to accept contactless payments | Accept card payments with high sales mobility | Full register system for restaurants and retail shops |

- Same-day funding: With the Everyday Funding service, you can get funds deposited into your account on the same day as the transaction. Few other merchant service providers offer this kind of quick funding. What’s more, this benefit is free for users with a U.S. Bank checking account.

- Surcharging and debit card optimization: Pay lower (or no) fees and keep more of your earnings with U.S. Bank’s surcharging features. Have your customers pay transaction fees instead of bearing the burden yourself, ultimately improving your bottom line. This is especially useful for small businesses that are still trying to find their footing in their industry.

- Fraud protection: Features and programs like Real Time Payments, Singlepoint, and IBM Trusteer Rapport offer you layers of protection against payment fraud—whether that’s check, cash, or online payments.

New customers who open a payment solutions account with U.S. Bank can get merchant account fees of up to $1,000 refunded over three months. Member FDIC.

To qualify, the new U.S. Bank Payment Solutions Merchant Account (MID) must be (1) opened and approved by June 30, 2025, and (2) kept open and actively accepting and settling card payments at the time monthly statement credits are applied.

PaymentCloud: Best for high-risk merchants

Overall Score:

3.92 / 5

Pros

- Excellent customer support

- Customized high-risk payment gateway

- Crypto and zero-cost processing available for low-risk businesses

Cons

- Pricing not disclosed

- Longer application and approval process

- Charges extra for virtual terminal and payment gateway

Overview

Who should use it:

High-risk businesses (tobacco, vape shops, liquor, firearms) that need the best possible odds for payment processing approval will find PaymentCloud a suitable solution.

Why I like PaymentCloud:

PaymentCloud is a popular merchant service provider that specializes in mid-to-high-risk businesses. It offers a full range of payment processing features including invoicing, subscription management, payment gateway, payment terminal, and more. The company has relationships with more than 10 banks and a step-by-step application process to help you submit all the documents needed to get approved by one of their partner banks.

I like how PaymentCloud is highly integrable. It allows high-risk businesses to accept in-person, online, and manual payment methods as well as connect with POS systems, payment gateways, and virtual terminals. PaymentCloud is also highly flexible in its pricing, so merchants not only get customized rates but can also choose the best way to manager their costs.

That said, expect higher fees with a PaymentCloud merchant account, as this is usually the case with high-risk businesses.

PaymentCloud’s fees are always custom-quoted based on specific business factors. Flat-rate and interchange rates are available depending on your business needs and discounts are available for high-volume businesses. The pricing below are estimates we obtained from PaymentCloud.

- Monthly fee: $10 to $45

- Typical low-risk transaction fees: 2% to 3.1%

- Typical mid-risk transaction fees: 2.25% to 3.4%

- Typical high-risk transaction fees: 2.7% to 4.3%

- Payment gateway monthly fee: $15

- One-time virtual terminal fee: $15 to $45

- Contract length: None, month-to-month options available

- Early termination fees: Waived

- Chargeback fees: $25 to $45

- Cross-border fees: 1% to 2%

- 1000+ integrations available, no API required

PaymentCloud has many options for card readers and POS systems. However, PaymentCloud does not disclose specific models or pricing on its site. You’ll need to contact the provider for a specific quote.

If you’re migrating over to PaymentCloud from a different processor, PaymentCloud will reprogram your existing equipment if possible.

- Medium- and high-risk business support: PaymentCloud will support business types that other services won’t come near. This software will work with businesses selling firearms, tobacco products, bail bonds, and more.

- Chargeback protection: In line with its high-risk business support, PaymentCloud gives you strong chargeback protection. You’ll get alerts and tracking functions for disputes, as well as prevention analysis tools.

Related reading: Best high-risk merchant account providers

PayPal: Best for flexible checkout methods

Overall Score:

3.86 / 5

Pros

- Easy to use

- Trusted by customers

- Accept international and PayPal payments

Cons

- Account stability issues

- Monthly fee for virtual terminal

- Complex pricing

Overview

Who should use it:

PayPal is a recommended option for solopreneurs or hobbyists with low-volume and occasional sales or an additional payment option for online stores.

Why I like PayPal:

As a pioneer in mobile payments, PayPal has an advantage of more than 400 million users, both consumers and merchants, using the service. Adding PayPal as a payment option can increase online store conversions and reduce cart abandonment because shoppers don’t need to type in payment or shipping information. PayPal alone makes this distinction and is often used with other merchant accounts like those on our list.

This makes PayPal a household name, with customers preferring to pay with their PayPal account every chance they get, both for security and convenience. And with PayPal’s checkout feature available as a standalone or in addition to other payment processors, businesses won’t go wrong by adding PayPal to their payment options.

Like Square, PayPal is a payment facilitator, so while it’s easy to sign up and use, the aggregate merchant account is less reliable. This means business accounts can be flagged and frozen if the company deems anything suspicious, which is problematic for businesses relying on daily deposits. Read our Square vs PayPal comparison to learn more.

- Monthly fee: $0 to $30

- In-person transaction fee: 2.29% plus 9 cents

- Online transaction fee: 2.59% to 2.99% plus 49 cents

- Keyed-in processing fee: 3.49% + 9 cents

- Invoice payment processing fee: 3.49% + 9 cents

- QR code payment fee: 2.29% + 9 cents

- PayPal Checkout transaction fee: 3.49% plus 49 cents

- Contract length: Month-to-month

- Early termination fee: $0

- Chargeback fee: $20

- Card readers: $29 to $199

PayPal Card Reader | PayPal Terminal |

|---|---|

|  |

$79 (first one $29) | $199 (model with built-in barcode scanner available for $239) |

Accept chip, PIN, and contactless payments. Connect to Zettle POS app via Bluetooth. Battery lasts eight hours or 100 transactions. Optional charging dock available. | Portable touch-screen POS pre-programmed with PayPal Zettle. Accept chip, PIN, contactless, and QR payments. Battery lasts 12 hours (four to six hours with intensive use).

|

- Instant PayPal payouts: If you’re using a PayPal account, you’ll be credited your received funds instantly. You can also opt to pay a 1.5% fee for the same instant payout when using a linked bank account.

- Social selling: You can connect PayPal Business to social media sites like Facebook and Instagram for multichannel selling.

- International payments: PayPal lets you accept international payments, for an additional 1.5% processing fee.

- Fastlane Guest Checkout: Merchants can add a guest checkout option to their ecommerce sites. This allows online buyers to quickly make purchases without needing to create an account. PayPal customers need only submit a confirmation code in order for Fastlane to recognize them.

- Smart Receipts: PayPal digital receipts can now include personalized product offers and discounts to entice customers to make additional purchases. These additions are powered by artificial intelligence and are based on the buyer’s purchase history.

Related reading:

- Best mobile credit card processors

- Best credit card payment apps

- Best nonprofit credit card processing solutions

Stripe: Best for online payments

Overall Score:

3.84 / 5

Pros

- Powerful, user-friendly developer tools, and application programming interfaces (APIs)

- Robust security, reporting, and account management tools

- Supports more than 35 countries and 135 currencies

Cons

- Lacks out-of-the-box mobile functionality

- Best for those with software development skills or resources

- Add-on fees for invoicing and recurring billing

Overview

Who should use it:

Businesses looking for a scalable and highly customizable online payment solution. Businesses that process international sales will also appreciate Stripe’s payment versatility and online sales functionality.

Why I like Stripe:

Stripe is a payment processor with sophisticated software and APIs ideal for online businesses. Its pre-built integrations make it easy to connect a Stripe checkout to almost any website or software. Besides PayPal, Stripe supports some of the widest range of payment types. I particularly like how it can accept a long list of local payment methods in 47 countries around the world including different buy now, pay later (BNPL) solutions.

Like Square and Helcim, Stripe offers no-code checkout customizations. However, what sets it apart is Stripe’s advanced developer-based customization tools. Businesses can use Stripe’s library of well-documented APIs and SDKs to create custom online checkouts, subscription management, and more.

On the other hand, Stripe lacks a pre-built mobile payment and POS app. Consider Square or PayPal if you need a more user-friendly setup.

- Monthly fee: $0

- Card-present transaction fee: 2.7% + 5 cents

- Card-not-present transaction fee: 2.9% + 30 cents

- Keyed-in transaction fee: 3.4% plus 30 cents

- ACH: 0.8%, $5 cap

- Invoicing: + 0.4% to 0.5%

- Recurring Billing: + 0.5% to 0.8%

- 1% additional fee for international cards and currency conversion

- Contract length: None, pay-as-you-go billing

- Early termination fee: $0

- Chargeback fee: $15 per lost dispute

- Chargeback protection and coverage available for 0.4% transaction fee

- Card readers: $59 to $349

You will need to sign up for a Stripe merchant account to access the purchase hardware options within the merchant account dashboard.

Stripe Reader M2 | BBPOS WisePOS E | Stripe Reader S700 |

|---|---|---|

|  |  |

$59 | $249 | $349 |

Accept EMV chip, contactless, and mobile wallet payments. This battery-powered reader connects to your POS app via Bluetooth. | Android-based POS with a 5-inch display including PIN functionality. Connects to a third-party POS app via Wi-Fi. | Android-based smart reader for mobile and countertop use. Customize or use pre-built elements. Connects via WiFi or Ethernet. |

- Multicurrency processing: Customers can pay you in over 135 currencies, making Stripe a great platform for online and international sales.

- Stripe invoicing: Create custom invoices with elements like brand logos and colors. You can also have the system generate numbers for each invoice for easier tracking and reconciliation, plus add Stripe-hosted payment links to invoices.

- Fraud prevention tools: To detect payment fraud, Stripe uses both machine learning and an existing and perpetually growing network of data points and models. This information helps Stripe’s machine learning infrastructure and algorithms detect emerging fraud patterns and see which payments are high-risk. You can also set the system to automatically block these payments while keeping legitimate customers on a whitelist.

Related reading:

Quiz: Which merchant account service is right for you?

Which Payments Provider is Right for You?

How to choose the best merchant services

Some merchant services are more compatible with certain business types than others. So, when choosing the best payment processor, it’s crucial that you are already familiar with the types of services that your business needs. Once you have that down, follow these guidelines:

Step 1: Look for your preferred payment methods

Merchant services offer a wide range of payment methods for both card-present and card-not-present transactions. You will likely be looking for a combination of both so narrow down your options with providers that can offer the cheapest rates based on your processing volume.

- Card-present methods are generally done through swiped, EMV chip, contactless, and digital/mobile wallet payments. Debit cards and prepaid cards such as gift cards, EBT, and FSA are also card-present payments.

- Card-not-present payment methods are primarily remote transactions that not only refer to credit card payments, but other forms of payments as well such as ACH, e-checks, and bank transfers.

Are you a freelancer looking for the best payment options for your line of work? Review our picks for the best payment methods for freelancers.

Step 2: Compare essential payment processing tools

Payment processing tools refer to a merchant service provider’s set of features used to process card-present and card-not-present payment methods.

- Invoicing and recurring billing

- Virtual terminal

- Online payment gateway (website checkouts, shareable payment links)

- Stored card payments

- Level 2 and 3 data processing for B2Bs

- Cross border payments

- Nonprofit payment processing

Ideally, you will find a provider that offers most of these features for free, otherwise, you should look for one that matches your business needs without charging additional monthly costs.

Check out our recommendations for:

Step 3: Match your required business management integrations

Some merchant services come with business management integrations. You will find providers with built-in integrations that will allow you to use these features for free, while others come with an additional monthly cost.

Examples:

- QuickBooks and Wave are primarily paid accounting and bookkeeping platforms with built-in payment processing.

- Square offers free and paid POS software with built-in payment processing features. It also provides add-on business management tools such as loyalty and rewards management, marketing tools, and employee management.

- iATS is a nonprofit management platform with its own credit card processing service.

- Clover is a POS software and hardware provider with a range of business management features that can be programmed to work with a number of merchant service providers.

Note that all of the merchant services providers in our list have direct integrations with third-party business management software.

Step 4: Check for essential card reader features

Card readers can be mobile paired with a mobile payment app, wireless standalone with an integrated POS app, or built-in to your countertop POS hardware. Depending on your business model, you may need one or all of these card readers.

Whatever card reader type you need, check for the following features before deciding on an option:

- At least a one-year warranty on the hardware

- Your preferred card-present payment methods (swipe, EMV chip, contactless, digital payments)

- Compatibility with mobile device operating systems for mobile credit card readers with mobile apps.

- Payment/POS app that’s integrated into your main POS system for mobile and wireless card readers.

- Ability to process credit card payments without an internet connection.

- Great user reviews to ensure reliability (minimal failed transactions) and long battery life for processing payments on the go.

- Security features (tokenization, encryption) to protect your transactions

Read our selection of the best credit card readers.

Step 5: Identify your ideal merchant account features

In general, merchant services differ in pricing structure, setup and application, contract terms, security measures, funding speed, and customer service. For this category, choosing the right merchant account features will depend on your business size.

- Small businesses and startups benefit more from merchant services that do not require an application process, simple setup, pay-as-you-go terms, zero monthly account fees, and flat payment processing rates.

- Small, established businesses as well as mid-sized, and fast-growing businesses will get better rates with their higher sales volume. Instead of flat payment processing fees, they can look for merchant services that offer interchange plus transaction rates. Pay-as-you-go contract terms are still ideal, but these types of merchants can easily qualify for a more secure traditional merchant account that requires an application process.

- Mid-sized to large businesses that process higher transaction volumes can get even better rates with merchant service providers that offer monthly fees plus wholesale transaction rates (with no percentage markups).

- High-risk payment processing requires a special category of merchant services that can help businesses that fall under the category of “high risk” get approved for a merchant account.

- Funding speed is ideally business day with the option for same-day deposits for a fee. Merchant services for small businesses usually charge for batch fees while some that cater to large-volume businesses do not charge extra.

- Payment security, such as various tokenization and encryption technology, should be one of your non-negotiable requirements for a merchant account service. Fraud detection tools can be simple (best for small businesses and startups) or customizable (ideal for large-volume businesses). PCI security is also essential but look for a provider that will assist you with compliance.

- Customer support should include the availability of live assistance (phone, email, chat) and offline resources such as a knowledge base and video guides. Additionally, you should also know how much assistance you would need and get during the merchant application process, migration, and setting up of your merchant account.

How to apply for a merchant account

Choosing the merchant services you want for your business is just the beginning. Depending on the solution you choose, you’ll need to submit an application.

Our guide walks you through the application process, the documents you’ll need, red flags to watch out for, and tips for negotiating lower rates.

Thank you for downloading!

Methodology: How I evaluated the best free merchant services

In evaluating the best merchant services, I focused on finding providers with the widest range of payment processing features and the most reasonable pricing. I narrowed down my list to 34 traditional merchant service account providers and payment facilitators and scored each one against 23 data points divided into 4 categories of pricing and contract, payment types, account features, and expert score.

Click through the categories below for our full criteria:

30%

Pricing & Contract

30%

Payment Types

20%

Account Features

20%

Expert Score

30% of Overall Score

Transaction fees weighed heavily here. We also awarded points for month-to-month or pay-as-you-go billing and no monthly, cancellation, or chargeback fees. and only included providers that offer competitive and predictable flat-rate or interchange-plus pricing. We also awarded points to processors that offer volume discounts.

30% of Overall Score

The best merchant accounts can accept various payment types, including POS and card-present transactions, mobile payments, contactless payments, ecommerce transactions, and ACH and e-check payments, and offer free virtual terminal and invoicing solutions for phone orders, recurring billing, and card-on-file payments.

20% of Overall Score

20% of Overall Score

*Percentages of overall score

Please note that my scores are based on the currently available features and information. This list will be regularly updated based on the latest technology and user demands to ensure that I provide you with the best information.

Best merchant services frequently asked questions (FAQs)

Square is the best option for many businesses. Helcim offers low pricing, and PaymentCloud is excellent if you’re having trouble getting approved.

Anything under 2.5% is good and under 3% is average.

Small businesses typically pay between 1.9% to 3.75% per transaction, with online and card-not-present transactions being more expensive.

550 is the minimum credit score you’ll likely need for a dedicated merchant account. Aggregate payment processors (like Square or PayPal) don’t require a credit check. However, aggregate processors aren’t compatible with all businesses. It’s possible to get a merchant account with bad credit, you just may need to work with a dedicated high-risk processor.

No. In some cases, you can pass along the fees to your customers through surcharging, cash discounting, or convenience fees, but there is no way to accept credit or debit payments without a fee.

Bottom line

Choosing the right merchant account provider can save your business lots of money in fees each month. The best payment processors are also easy to use, offer good value with business solutions, and integrate with popular software. Plus, merchant accounts should be transparent and reliable.

Visit Square, our top pick, to see if it’s a good fit for your business.